How Pain & Suffering Is Calculated in Texas Car Accident Claims

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurers typically use multiplier or per diem methods to estimate pain and suffering, but the strength of your medical documentation and "human impact" evidence are more important than any formula.

- Texas has no general cap on pain and suffering in typical car accident cases, though your recovery can be reduced or barred entirely based on your percentage of fault under comparative negligence rules.

- Early settlement offers often undervalue non-economic damages because they're made before treatment is complete and full documentation exists.

You were rear-ended in rush hour traffic on I-35 near downtown Austin last month. Your neck still aches every morning, and you’ve missed two weeks of work. Now the insurance adjuster has called with a settlement offer that barely covers your medical bills. The number they assigned to your “pain and suffering” seems almost random.

You’re not wrong to question it. Insurers use specific methods to put a dollar figure on non-economic harm, and understanding those methods gives you leverage in negotiations. Texas law also shapes what you can recover in ways that differ from other states.

What Pain & Suffering Means in a Texas Car Accident Claim

When you file an injury claim after a crash, your damages fall into two categories.

Economic damages cover measurable losses: medical bills, lost wages, property repair costs.

Non-economic damages cover everything else: physical pain, mental anguish, loss of enjoyment of life, and the daily inconvenience of living with an injury.

Pain and suffering falls squarely in the non-economic category. There’s no receipt for it. No invoice. That’s why insurers rely on internal evaluation practices to assign a number. These practices can feel arbitrary because they involve judgment calls about how much your suffering is “worth.”

The methods insurers use are negotiation tools, not legal requirements. Understanding them helps you recognize when an offer undervalues your claim. If you’re wondering whether your situation warrants legal action for pain and suffering, knowing how these calculations work is the first step.

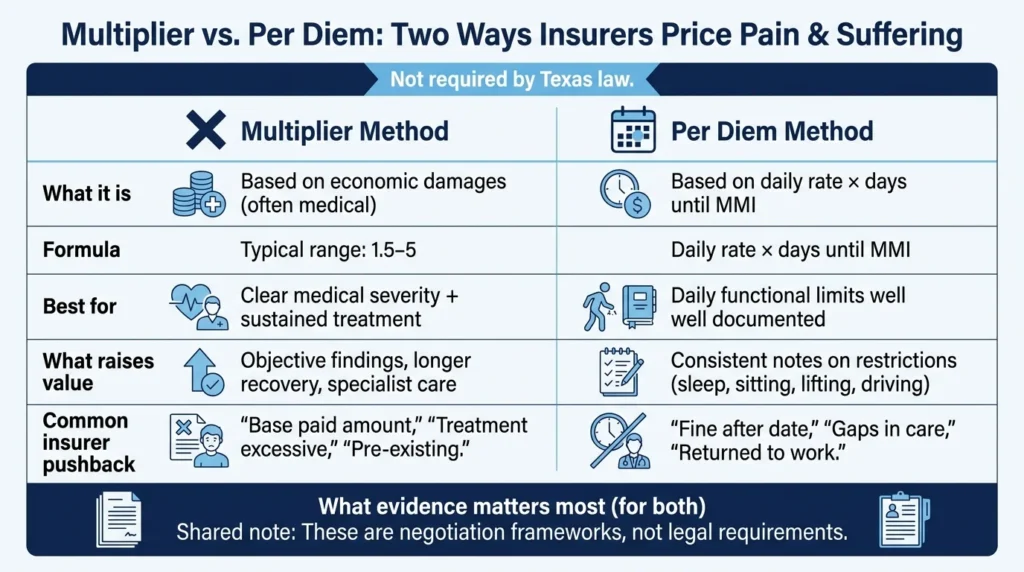

The Two Most Common Ways Insurers Estimate Pain & Suffering

Insurance adjusters typically start with one of two approaches: the multiplier method or the per diem method. Neither is required by law. Both serve as frameworks for negotiation.

The multiplier method takes your economic damages (usually medical expenses) and multiplies them by a number between 1.5 and 5, depending on injury severity. A minor soft-tissue injury might get a 1.5 multiplier. A serious injury requiring surgery and months of recovery might justify a 4 or 5.

The per diem method assigns a daily dollar value to your pain and then multiplies it by the number of days you suffered. If an adjuster values your daily pain at $150 and you experienced significant symptoms for 120 days, the calculation yields $18,000.

More important than the math is what goes into it. The “inputs” drive the outcome: your medical treatment, how long it lasted, what limitations you experienced, and whether your account is credible and consistent.

Multiplier Method: How the Number Is Typically Built

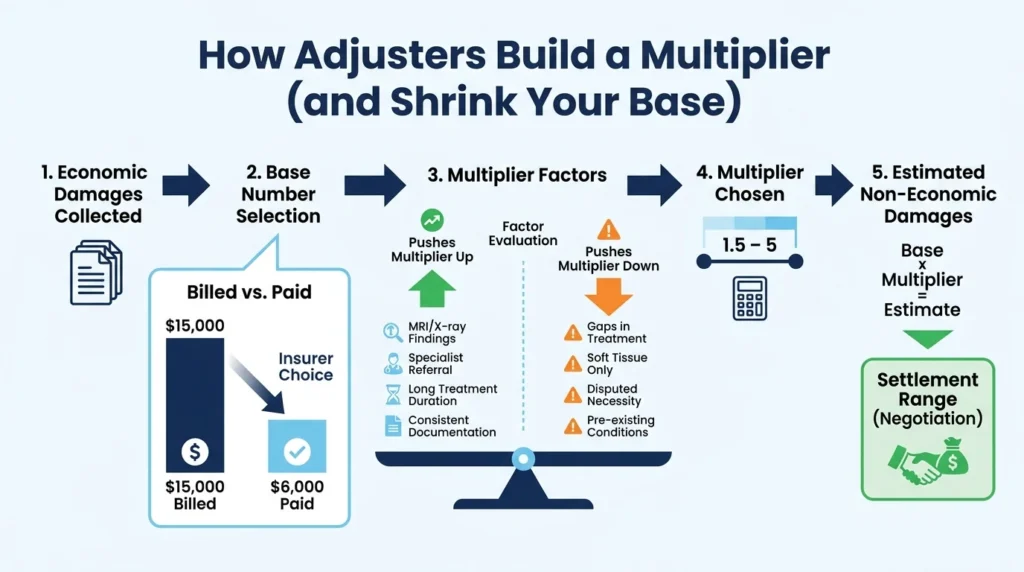

Adjusters using the multiplier approach first establish a “base” number. This is usually your medical expenses, though some adjusters include lost wages or limit the base to certain treatment types.

A critical detail to note is that insurers may use the amount actually paid by insurance rather than the full amount billed. If your hospital billed $15,000 but your health insurer paid $6,000, the adjuster might argue the base should be $6,000. This immediately shrinks your non-economic calculation.

Several factors push multipliers up or down:

- Objective medical findings (MRI results, X-rays showing damage) support higher multipliers.

- Longer treatment duration suggests more serious impact.

- Gaps in care give adjusters ammunition to argue you weren’t really hurt.

- Pre-existing conditions may be used to attribute some pain to prior problems.

Watch for this tactic. Adjusters who aggressively dispute your medical expenses aren’t just fighting over bills. They’re controlling the base number to suppress your entire car accident settlement.

Per Diem Method: Valuing Each Day of Pain & Disruption

The per diem approach requires defining two things: a reasonable daily rate and the time period that rate applies to.

The time period typically runs from the date of injury until you reach maximum medical improvement (MMI), the point where your condition has stabilized. For some injuries, this might be weeks. For others, it may be months or longer.

Adjusters attack per diem claims by arguing the period should be shorter. They’ll point to gaps between appointments and say, “You were fine after that date.” They’ll note that you returned to work and claim your pain ended then.

To make a per diem argument credible, tie your daily rate to documented functional limitations. If your medical records show you couldn’t sit for more than 20 minutes, couldn’t lift your children, or needed help with basic tasks, those details justify a meaningful daily value.

Human Impact Signals Insurers Look For

Beyond the formulas, adjusters evaluate what’s sometimes called “human impact.” This is the real-world disruption your injury caused. Strong human impact signals justify higher non-economic values.

Objective medical support is the most important part of your claim. Imaging studies, range-of-motion measurements, specialist referrals, and consistent symptom documentation in your records all strengthen your claim. When your doctor’s notes align with what you’re reporting, your account gains credibility.

Functional disruption translates pain into terms adjusters understand. Work restrictions from your doctor. Activities you can no longer do. Driving limitations. Sleep problems documented in treatment notes. The inability to care for your children the way you did before.

Credibility factors can make or break a claim. Consistent treatment without unexplained gaps. A clear mechanism of injury that matches your symptoms. No contradictory social media posts showing you doing activities you claimed you couldn’t do.

High-Value Impact Categories to Document

Daily living limitations include difficulty bending, lifting restrictions, reduced sitting or standing tolerance, and inability to perform household tasks. If you needed help getting dressed or couldn’t cook meals for your family, document it.

Emotional and mental impact covers anxiety while driving, sleep disruption, irritability, and loss of independence. These carry more weight when they appear in your treatment notes, not just your own account.

Relationship and lifestyle impact includes missed family events, hobbies you’ve had to abandon, and exercise routines you can no longer maintain. A parent who couldn’t attend their child’s soccer games for three months has a concrete, relatable loss.

Texas Law That Directly Affects Pain & Suffering Negotiations

Texas has specific rules that shape what you can recover. Understanding them prevents surprises during negotiations.

Comparative Fault Changes the Final Number

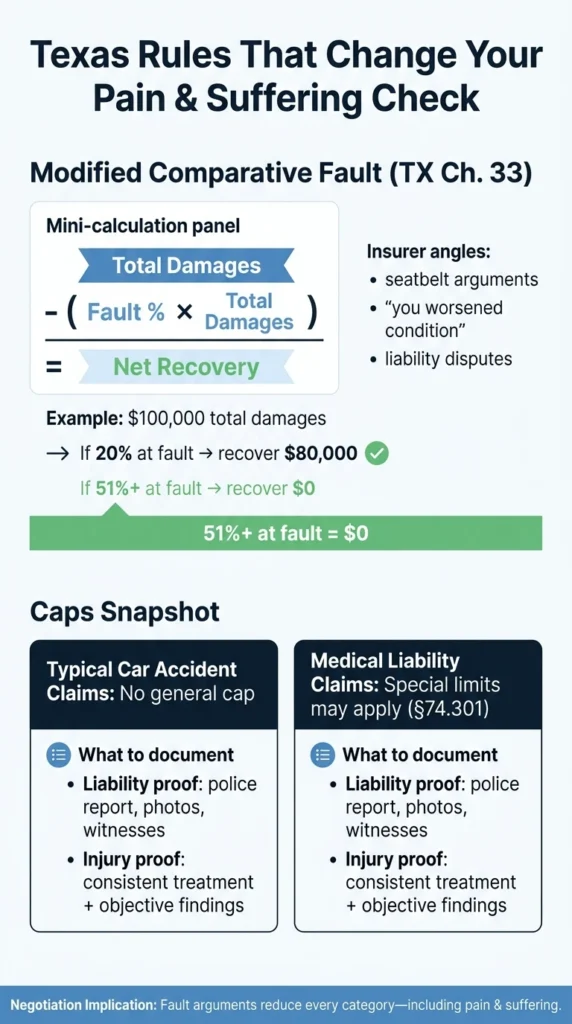

Texas follows a “modified comparative fault” system under Texas Civil Practice and Remedies Code Chapter 33. If you’re found partially at fault for the crash, your recovery is reduced by your percentage of responsibility.

Here’s how it works: If your total damages (including pain and suffering) are valued at $100,000 but you’re found 20% at fault, you recover $80,000. If you’re found more than 50% responsible, you recover nothing.

This means fault disputes directly affect your pain and suffering payout. Adjusters may argue you were partially responsible for your injuries, perhaps by claiming you weren’t wearing a seatbelt or that you made treatment choices that worsened your condition.

Protect your final number by documenting liability as thoroughly as you document injuries. Crash scene photos, the police report, and witness contact information are all essential for truck accidents and car crashes alike.

No General Cap, But Special Rules for Medical Liability

In typical Texas car accident cases, there is no blanket statutory cap on pain and suffering damages. This is important. Many states limit non-economic recovery, but Texas generally does not for standard auto injury claims.

The exception involves medical liability claims. Under Texas Civil Practice and Remedies Code § 74.301, non-economic damages in health care liability cases are subject to statutory limits. If your car accident claim somehow involves medical malpractice (for example, negligent treatment of your crash injuries), different rules may apply.

For the vast majority of Texas car accident victims, the absence of a general cap means your pain and suffering recovery depends on the strength of your evidence and your negotiation, not an arbitrary legal ceiling.

Why Early Settlement Offers Can Be Low

Insurance companies are businesses. Their goal is to resolve claims for the lowest reasonable payout. Early offers often reflect this priority.

Timing plays a role. Adjusters frequently make offers before your injury story is complete. You may not have finished treatment. Your doctor may not have determined your prognosis. You haven’t reached maximum medical improvement. The adjuster is betting you’ll accept a quick payment rather than wait for full documentation.

Common arguments adjusters use to shrink non-economic value include:

- “Minor impact” claims suggesting the crash wasn’t severe enough to cause real injury.

- Characterizing your injury as “just soft tissue.”

- Attributing your symptoms to pre-existing conditions.

- Calling your treatment excessive or unnecessary.

Texas regulates insurer conduct. The Texas Department of Insurance enforces unfair claim settlement practice rules that require insurers to handle claims in good faith. This doesn’t guarantee a fair offer, but it provides regulatory context for how claims should be processed.

If you’ve received an offer that seems low, consider what’s missing. Have you finished treatment? Is your documentation complete? Does the adjuster have everything needed to evaluate your claim fairly?

Understanding average settlement factors can help you assess whether an offer is reasonable.

When to Talk to a Texas Car Accident Attorney About Pain & Suffering

Some situations benefit significantly from legal guidance. Consider speaking with an attorney if:

- Your injuries are serious, required surgery, or caused lasting impairment.

- Treatment lasted several months or is ongoing.

- The adjuster disputes fault or claims you’re significantly responsible.

- You’ve already given a recorded statement.

- The offer feels substantially lower than your actual losses.

An attorney can help build the demand narrative, organize medical records, rebut adjuster arguments, and calculate how comparative fault might affect your recovery. At Angel Reyes & Associates, we’ve spent over 30 years helping Texas car accident victims recover fair compensation. We’ve recovered more than $1 billion for our clients, and we offer free consultations with no fee unless we win.

You can review our case results and client testimonials to see how we’ve helped others in similar situations. If your pain and suffering claim has been undervalued, contact us to discuss your options.

Past results do not guarantee future outcomes.

Pain & Suffering Valuation FAQs

Can I recover pain and suffering if my car accident made a pre-existing condition worse?

Yes, potentially. In Texas, you may still seek damages for the aggravation of a prior condition, but insurers often look closely at your earlier records and whether your doctors clearly tied the worsening symptoms to the crash.

Do pain and suffering damages get taxed in Texas car accident settlements?

Usually, compensation for physical injuries is not taxable under federal law, but amounts tied only to interest or certain non-physical claims can be treated differently. Tax treatment depends on how the settlement is structured, so the details are crucial.

What if the at-fault driver only has minimum insurance coverage?

Your claim’s value does not create more coverage by itself, so a strong pain-and-suffering case can still be limited by the other driver’s policy limits. In some situations, your own uninsured/underinsured motorist coverage may become important if you carry it.

Should I accept a pain and suffering offer before I finish medical treatment?

It can be risky because once you settle, you usually cannot reopen the claim if your symptoms last longer or treatment becomes more expensive. Many people wait until their condition is more stable so the full impact is easier to measure.

Can social media affect a Texas pain and suffering claim?

Yes. Photos, videos, comments, and location tags can be used to argue your injuries were less serious than claimed, especially if they seem inconsistent with your medical records or stated limitations.

About the Authors

Spencer Browne

Writer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials across Texas. He focuses on car, truck, and wrongful death cases, with notable verdicts including a landmark win in the Choctaw Casino bus crash case. A recognized speaker and legal educator, Spencer is a member of the American Board of Trial Advocates and has been honored as a Texas Super Lawyer and one of D Magazine’s Best Lawyers in Dallas. He brings deep trial experience and relentless advocacy to every client he represents.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...