Five Things You Can Do to Maximize Your Injury Settlement in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Early medical evaluation and consistent follow-up create the timeline insurers rely on when valuing injuries.

- Preserved evidence and organized weekly documentation reduces disputes and supports higher negotiations.

- Careful communication and the right timing, guided by a lawyer, help prevent low offers and irreversible paperwork mistakes.

Maximizing the Value of Your Car Accident Case

If you have been injured in a car accident in Texas and are seeking compensation, either through an insurance claim or potentially via a lawsuit, it’s important to handle your case properly. A case is not something that is simply passed off to a lawyer and left alone—you are an active participant and should be involved every step along the way.

Whether you were rear-ended on Congress Avenue in Austin or side-swiped on I-35 in Lewisville, if you want to maximize your injury settlement, there are some things you can do to help build and strengthen your case.

1. Get Medically Examined Early & Track Treatment Through Recovery

Get evaluated by a medical professional as soon as you reasonably can, even if you think you will feel better in a few days. Early records create a clean starting point that ties your symptoms to the incident date. If you wait, the insurer may argue your injury was minor, unrelated, or caused by something else.

Be direct with your provider. Describe every symptom and when it started. Mention headaches, dizziness, sleep problems, tingling, weakness, and pain that comes and goes. If you’re struggling to remember symptoms, keep a journal and write them down. Those details often drive referrals, imaging, and the care plan that later supports settlement value.

Consistency is what turns treatment into proof. Gaps and missed appointments are common negotiation targets. If you miss a visit for a real reason, reschedule quickly and keep a short note about what happened.

Use this simple routine after every appointment so your file stays complete and easy for your lawyer to use:

- Save the after-visit summary, work status note, and any imaging results.

- Keep prescriptions, referrals, and physical therapy instructions.

- Record new symptoms and flare-ups within 24 hours.

- Track restrictions like “no lifting” or “reduced hours” in your calendar.

If you don’t think you can afford to see a medical professional, don’t worry! Call their office and tell them you were involved in an accident and are pursuing an injury claim. Some providers are more than willing to treat you now and collect payment later once your settlement is finalized. In fact, these providers are usually accustomed to providing extensive documentation detailing services rendered and their associated costs, so you can build it into your case file.

2. Preserve Evidence Early & Lock in Proof of Fault

When evidence supporting claims of fault is strong, the insurer has fewer excuses to delay or discount the claim. Evidence fades quickly. Scenes change, vehicles get repaired, and surveillance video can be overwritten. Even in a “simple” crash, the other side may try to shift fault, minimize impact, or dispute how your injury happened.

Focus on proof that explains the mechanics of the incident and the identities of everyone involved. If you can do it safely, collect what you can that day and back it up in two places.

These are the most useful items to gather and save:

- Photos of the scene, vehicle damage, visible injuries, roadway conditions, and any hazards

- Names, numbers, and emails for witnesses

- Dashcam, doorbell, or nearby business video saved as a file, not only a link

- The report number and the agency that responded

- Damaged items kept in their post-incident condition until your lawyer says repairs or disposal are safe

If the injury happened on a property or in a business, ask in writing that any surveillance video be preserved. Keep a copy of that request. It can prevent a later claim that the footage no longer exists.

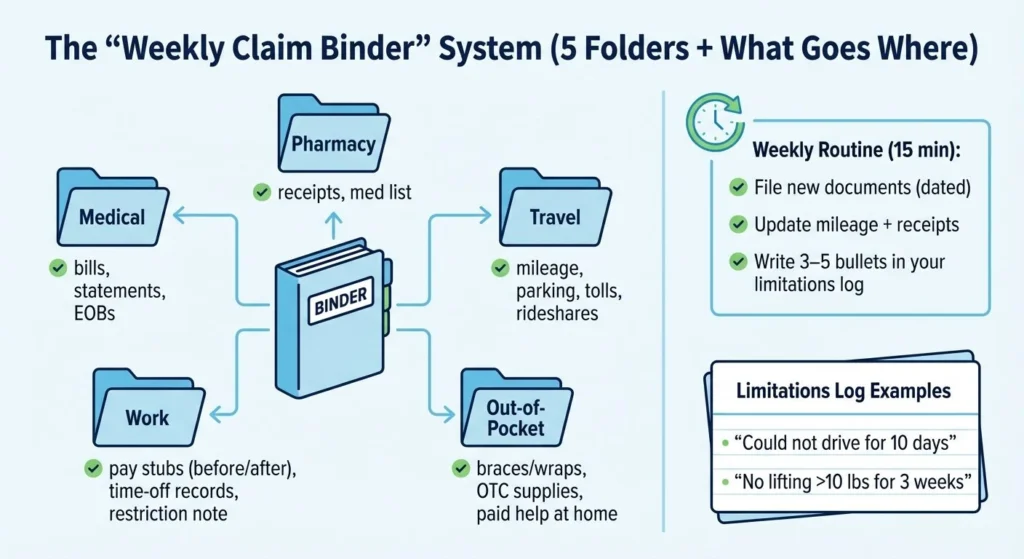

3. Document Costs, Lost Income, & Daily Limitations Every Week

Settlement offers track what you can prove. A clear file of bills, payment records, and life impact often moves negotiations more than a long explanation on a phone call.

Set up a binder and make time to update it once a week. Use five subfolders: medical, pharmacy, travel, work, and out-of-pocket. Keep everything dated.

Store each of these in their appropriate folder:

- Medical bills, statements, and insurance EOBs (medical)

- Pharmacy receipts and a current medication list (pharmacy)

- Mileage and travel costs for treatment, including parking, tolls, and rideshares (travel)

- Pay stubs from before and after, time-off records, and a short employer note confirming missed time or restrictions (work)

- Receipts for braces, wraps, over-the-counter supplies, and paid help at home (out-of-pocket)

Keep some paper in this binder to serve as a weekly limitations log. Write what you could not do, what triggered pain, and what you had to stop or reduce. Specifics like “could not drive for 10 days” or “could not lift more than 10 pounds for 3 weeks” are easier to evaluate than general statements. Keep what you write here factual and honest. Don’t exaggerate.

4. Limit Insurance Conversations & Control What You Sign

Adjusters often call early and ask friendly questions that create leverage for a low offer. Your goal is to avoid providing statements that downplay injuries, add uncertainty about fault, or open the door to unrelated medical history.

If you are not represented yet, keep communication narrow and written when possible. Confirm the claim number and basic facts. Do not guess about speed, distances, timing, or what someone “probably” did. If you do not know, say you do not know.

Be especially cautious with these common requests:

- Recorded statements

- Broad medical authorizations that give unlimited access to records

- Quick settlement paperwork that includes a full release

- Requests to “just sign” a form so they can “finish the file”

Ask for any request in writing and save it. If you feel pressured, it is usually a sign to slow down and get legal advice.

Also, treat your social media as part of the claim file. Posts about activities, travel, workouts, home projects, or “feeling fine” can be taken out of context. Privacy settings do not guarantee the content stays private.

5. Talk to an Injury Lawyer Early & Avoid Settling Before the Case Is Ready

Many people settle before they understand the full picture of their medical outlook, future care needs, or how their missed work and restrictions affect the value of their claim. In fact, insurance companies are hoping you’ll do the same. Once you sign a release, you usually cannot go back for more money if symptoms worsen or your doctor recommends new treatment.

Early legal help also matters for coverage. Some claims involve more than one source of recovery, including coverage you did not realize you had. Identifying all policies and deadlines early can raise the ceiling of the case and prevent avoidable mistakes.

Bring these items to your first meeting with an attorney to help them more accurately evaluate your position and available options:

- Photos, videos, and witness contact information

- Report details and the responding agency

- A list of providers and appointment dates

- Bills, EOBs, prescriptions, and work restriction notes

- All insurance information for everyone involved, including your own policy

- Any letters, emails, or texts from adjusters

Tell your lawyer about prior injuries to the same body parts and any gaps in treatment. Surprises weaken leverage. Clear disclosure lets your attorney handle the issues before the insurer uses them against you.

Evaluate Your Options Today

You cannot control whether an insurer plays hardball, but you can control how you approach your case. Your medical records, the proof of fault, the documentation of losses, and the mistakes you avoid in early calls and paperwork all make a difference in your final outcome.

If you want help building a demand that supports full value and pushing back on low offers, talk with a lawyer before you sign anything or give a recorded statement. Angel Reyes & Associates has over 30 years of experience helping Texans like you. We proudly serve clients across the state, and we don’t charge any fees unless we win. Contact us today to learn more about your options.

Settlement Maximization FAQs

Can my settlement drop if I am partly at fault?

Yes. In Texas, your recovery may be reduced based on your share of fault, and some situations may prevent recovery if your share of fault is too high.

What is an IME, and should I go if the insurer schedules one?

An insurer may request a medical exam by a doctor they choose. If they do, talk with your lawyer so you understand what is being requested and how to prepare.

Should I keep my injury claim separate from the property damage claim?

Often yes. Quick vehicle repairs can be handled while the injury claim develops, and mixing them can create pressure to sign paperwork before your medical situation is clear.

Where can I file a complaint in Texas if I think my own insurer is mishandling the claim?

The Texas Department of Insurance has a defined process for filing complaints against insurance carriers who act in bad faith. Check out their guidance on handling these situations here.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...