Car Insurance Requirements for Teen Drivers in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas requires 30/60/25 minimum liability coverage before your teen drives legally on any road.

- Adding a teen to your existing policy usually costs less than buying them a separate policy.

- Good student, driver education, and safe driving discounts can offset higher teen driver premiums.

Car Insurance Requirements for Teen Drivers in Texas

Your teenager just got their learner license, and your insurance questions are piling up faster than their driving hours. With their license test around the corner, it’s important to be prepared for them to have formal insurance.

Texas requires minimum liability coverage of 30/60/25 before your teen gets behind the wheel. That 30/60/25 rule applies whether your teen has a learner’s permit, a provisional license, or a full license. Getting this right matters for your family’s finances because a coverage gap could leave you personally responsible for damages if your teen is involved in an accident.

What Texas Law Requires for Teen Driver Insurance

Every vehicle driven on Texas roads must have liability insurance that meets the state minimum; your teen is no exception. Liability coverage pays for injuries and property damage your teen causes to others in a crash. It does not cover your teen’s own injuries or vehicle repairs.

The 30/60/25 minimum breaks down like this:

- $30,000 maximum payout for one person’s injuries

- $60,000 maximum payout for all injuries in a single accident

- $25,000 maximum payout for property damage

Those numbers sound substantial until you see how quickly bills can add up. A rear-end accident on I-35 can quickly surpass $30,000 after hospital treatment, ongoing rehabilitation, and more. For this reason, many families choose higher limits to protect their savings and home equity.

When Teen Insurance Coverage Must Start

Every driver, licensed or permitted, must have insurance. Most insurers automatically extend your own liability coverage to permit holders in your household, but confirm this with your insurer in writing before your teen starts building practice time behind the wheel.

Once your teen gets a provisional or full license, you must formally add them to your policy or obtain separate coverage. Failing to disclose a licensed teen driver can void your coverage.

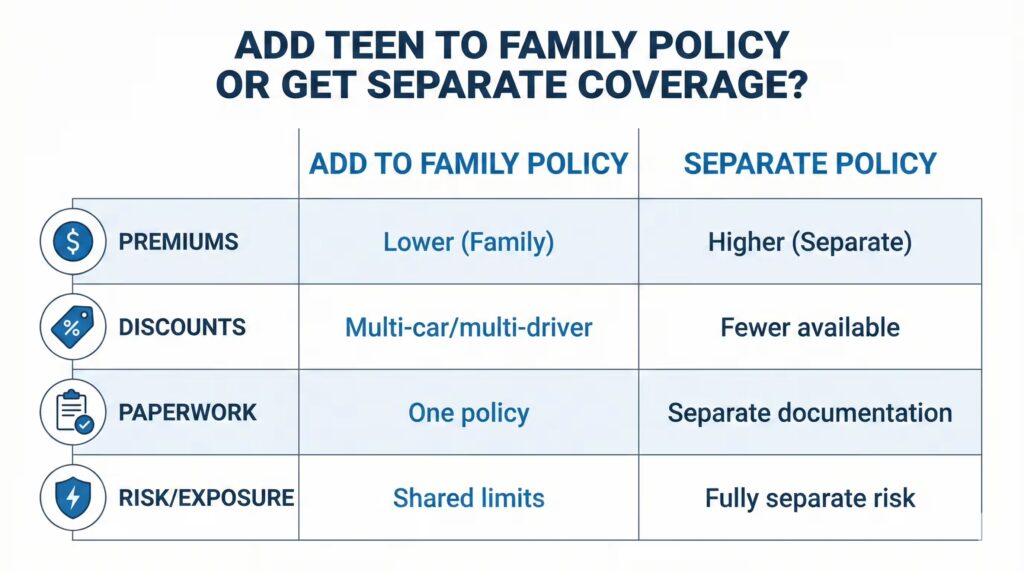

Adding a Teen to Your Policy vs. a Separate Policy

Most families add their teen to an existing policy because it costs less than buying a separate one.

Adding to a Family Policy

When you add your teen as a listed driver to your already purchased policy, they share your policy limits and deductibles. There are several benefits to this, including:

- Lower premiums than a standalone teen driver policy

- Multi-car and multi-driver discounts may apply

- Simpler paperwork and one bill

Adding a teen driver will increase your premiums. Young drivers are statistically more likely to be in crashes, so insurers charge more (in some cases, a fair bit more).

A Separate Policy for Your Teen

Alternatively, you could purchase an entirely separate insurance policy for your teen. A separate policy might make sense if adding your teen to your policy would spike your rates dramatically, or if your insurer requires it. This arrangement is not as common.

Drawbacks can include:

- Higher premiums as an inexperienced, “high-risk” driver

- No multi-policy discounts

- Your teen must qualify on their own driving record, which may lead to coverage denial as a new driver

However, this arrangement comes with one big advantage: because your teen would have their own policy limits and liability, your important assets like your home and other vehicles are not at risk should they exceed their liability limitation.

Talk to your insurer about both options. Get quotes in writing before deciding.

When Your Teen Owns Their Own Vehicle

Some teens purchase a vehicle with their own money or receive one as a gift titled in their name. This changes the insurance picture.

If the vehicle is titled in your teen’s name, they may need their own policy rather than being added to yours. Some insurers won’t cover a vehicle owned by someone not named on the policy.

Before your teen takes formal ownership of a vehicle, consider:

- Insurance cost: A policy in a teen’s name with no driving history will be significantly more expensive than adding them to an established family policy.

- Title alternatives: Keeping the vehicle titled in a parent’s name while the teen drives it may allow you to add both the vehicle and them as a driver to your existing policy at lower rates.

- Liability exposure: If your teen owns the vehicle and causes a crash, their personal assets (and potentially yours) could be at risk if coverage is insufficient.

Talk to your insurer before finalizing any title transfer for a more accurate quote.

Discounts That Can Lower Your Teen’s Insurance Costs

Adding a teen to your policy will raise your rates, but insurance companies typically offer several discounts that can help mitigate some of the increased cost of a young driver.

Good Student Discount

Teens who maintain a GPA average at or above a certain threshold often qualify for reduced rates. Your insurer may ask for a report card or transcript.

Driver Education Discount

Completing an approved driver education course can lower premiums. Texas requires teens under 18 to complete a driver education course anyway, so this might be an easy discount to obtain.

Telematics or Safe Driver Programs

Some insurers offer apps or devices that track driving habits. Teens who avoid hard braking, speeding, and late-night driving can earn discounts.

Vehicle Selection

Insuring a used sedan costs less than insuring a new sports car. Vehicles with high safety ratings and low theft rates typically have lower premiums.

Ask your insurer which discounts apply and what documentation you need.

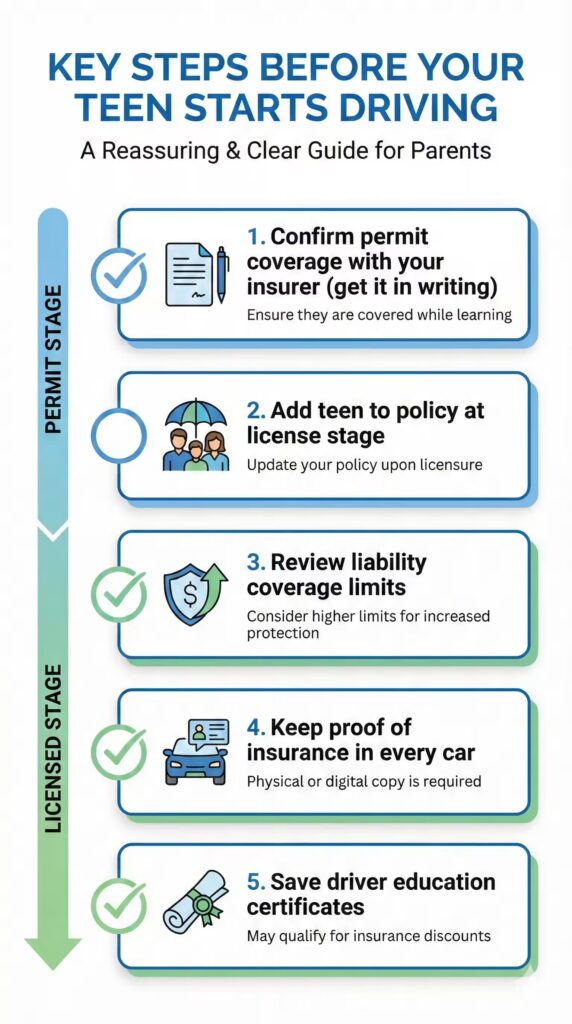

Steps to Take Before Your Teen Starts Driving

A few actions now can prevent coverage gaps and reduce your liability later.

- Confirm coverage when your teen gets a permit. Most policies extend automatically, but get written confirmation so there’s no gap.

- Add your teen formally once they receive a provisional or full license. Do not wait for the renewal period.

- Review your coverage limits. Consider whether the state minimum adequately protects your family’s assets.

- Keep proof of insurance in every vehicle your teen drives. Texas law requires drivers to show proof during traffic stops.

- Document your teen’s driving training. Save certificates from driver education courses for discount eligibility.

Parental Liability and Negligent Entrustment

Insurance handles most situations, but it has limits. If your teen causes a crash, you as a parent could face legal and financial consequences beyond what your policy covers.

Parental Liability in Texas

Texas law can hold parents responsible for a minor child’s negligent driving. This means an injured person could pursue a claim against you personally.

Your auto liability insurance covers claims arising from your teen’s driving, but if damages exceed your policy limits, your personal assets could be at risk. This includes things like savings or home equity. For more on how Texas handles parental responsibility, see A Parent’s Guide to Child Accident Liability in Texas.

Negligent Entrustment

Negligent entrustment occurs when you let someone drive your vehicle knowing they are unfit or unqualified. For example, if you let a teen drive who is unlicensed, intoxicated, or has a pattern of reckless driving take your car for a spin, you could be held liable for any resulting crash.

For more details, see Can You Get in Trouble for Letting an Unlicensed Driver Use Your Car in Texas?

Protect Your Family Before Your Teen Hits the Road

Getting your insurance right before your teen starts driving protects your family from unexpected costs after a crash. Confirm coverage in writing, add your teen to your policy once they’re licensed, and look into discounts that can reduce the financial impact.

If your teen is involved in a crash and you have questions about liability, coverage disputes, or your legal options, talk to our team at Angel Reyes & Associates today! We have guided Texas families through accidents for over 30 years. Reach out to request a free consultation for more information.

FAQs

Does my teen need their own insurance policy?

Not always. Most teens can be added to your family policy. But, if they own a vehicle titled in their name, they may need to purchase their own insurance for that vehicle.

What happens if I do not tell my insurer about my teen driver?

If you do not disclose a licensed teen driver, your insurer could void your coverage or deny a claim after a crash, making you liable for all damages.

Are learner permit holders covered automatically?

Yes, learner permit holders are usually covered automatically under your existing policy, but we recommend confirming this in writing with your insurer before your teen starts practicing.

How much will adding a teen driver increase my premium?

The amount varies by insurer, vehicle, and driving record. Ask your insurer about discounts for good grades and driver education to help offset the cost!

What should I do if my teen is in a crash?

If your teen is in a crash, make sure everyone is safe, call 911 if needed, exchange insurance information, and document the scene with photos. Then contact your insurer. For guidance, see Texas Teen Driver Accident Claims: A Complete Guide for Victims and Parents.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...