How Texas Insurers Value T-Bone Accident Claims

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

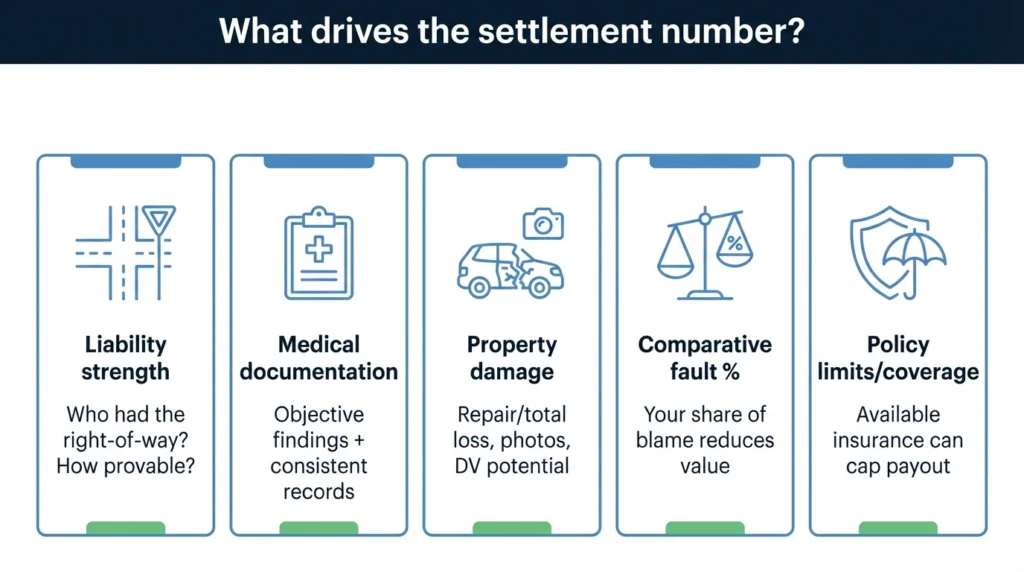

- Texas insurers value T-bone claims using five core inputs: liability strength, medical documentation, property damage, comparative fault percentage, and available policy limits.

- Under Texas's modified comparative negligence rule, being more than 50% at fault bars recovery entirely, while any fault percentage up to 50% reduces your net recovery proportionally.

- Early settlement offers are typically lower because adjusters discount for uncertainty about liability, causation, and future care needs that haven't been fully documented.

You were driving through an intersection near Lower Greenville when another car ran the light and slammed into your driver’s side door. Now you’re dealing with injuries, a damaged vehicle, and an insurance adjuster who just made an offer that seems far too low. Understanding how insurers actually calculate claim value can help you recognize whether that number reflects your real losses.

Determining Settlement Value in a Texas T-Bone Claim

The number an insurance company offers in a settlement negotiation isn’t pulled from thin air. Adjusters consider specific factors – such as liability strength, medical documentation, property damage, and Texas fault rules – when determining their offer.

Side-impact crashes can be difficult to value. Your car might not look totaled, but door intrusion injuries to your ribs, hip, or shoulder can be severe. Insurers sometimes use this argument to claim that your injuries couldn’t have come from “such a minor collision.” Causation disputes such as this often directly affect what insurers are willing to pay.

How Adjusters Evaluate Liability in Side-Impact Crashes

Before calculating damages, insurers determine who caused the car accident and how clearly it can be proven. For a T-bone accident, right-of-way evidence drives everything.

Common situations that can prove fault include:

- Red-light or stop-sign violations

- Left turns across oncoming traffic

- Unsafe lane changes

- Failure to yield at uncontrolled intersections

Adjusters rank evidence by reliability. Video footage from nearby businesses or dashcams carries the most weight. Independent witness statements matter, especially when documented properly. Police reports help but aren’t conclusive. Vehicle damage patterns can show point of impact and direction of travel.

Even before fully valuing your damages, the adjuster assigns a fault percentage. If they believe you share some responsibility, they’ll discount any offer accordingly.

The Adjuster’s Liability Checklist

For side-impact cases, adjusters look for specific proof of fault.

Fault may be proven through:

- Right-of-way evidence: This includes signal phase timing, point of impact location, and lane positions at the moment of collision.

- Contributory conduct arguments: Were you speeding or distracted? Did you brake late? Were your headlights off at dusk? These scenarios can shift fault toward you.

- Documentation that shuts down disputes: Intersection camera footage or photographs that clearly display lane markings, signal positions, and all vehicle damage angles can all prove fault.

How Insurers Categorize Damages

In Texas, insurance companies organize car accident damages into two buckets, and each type has different proof requirements.

Economic damages are documented dollar losses, which includes medical bills, lost wages, property repair costs, and rental car expenses.

Non-economic damages cover human losses that don’t come with receipts, including physical pain, emotional distress, loss of enjoyment of life, and disfigurement.

Texas Civil Practice and Remedies Code § 41 provides the framework for these types of damage.

Damages play a crucial role in determining offers. If your medical bills total $15,000, that number becomes the starting point for calculating everything else. Adjusters want proof for each type of damage, including itemized bills, medical records, pay stubs showing missed work, photos documenting injuries and vehicle damage.

Medical Bills & Treatment: Converting Care Into a Number

During the process of calculating your care needs, adjusters try to figure out whether your treatment was “reasonable and necessary” and whether the crash actually caused your injuries.

To determine this, they review:

- Emergency room and ambulance charges

- Diagnostic imaging (X-rays, MRIs, and CT scans)

- Physical therapy and chiropractic visits

- Specialist consultations

- Surgical recommendations

- Prescription costs

Insurance companies often argue that the cost of your care is inaccurate through the “low property damage” argument (claiming minor vehicle damage means minor injuries).

They may also use gaps in treatment, pre-existing conditions, and inconsistent symptom reporting across medical records to argue against your claim.

If an insurer says your treatment was excessive or unrelated to the crash, ask for their explanation in writing. Then, gather records that connect the crash to your symptoms and treatment, such as referral letters, imaging impressions noting acute findings, and work restriction documentation from your physician.

Future Medical Care: Valuing What Hasn’t Happened Yet

Insurers discount future damages unless they’re supported by medical documentation.

Types of future care that you may be entitled to compensation for include:

- Recommended surgeries not yet performed

- Ongoing physical therapy

- Long-term medications

- Follow-up imaging

- Counseling for accident-related anxiety

You will need to prove that you need future care. Adjusters want physician recommendations, documented prognoses, and treatment plans. A surgeon’s letter stating you’ll likely need a spinal fusion within two years carries weight.

Calculation Methods for Pain & Suffering in Texas

Texas law doesn’t mandate a specific formula for non-economic damages, but insurers use structured approaches during negotiation.

The multiplier method takes your economic damages and multiplies them by a factor (typically 1.5 to 5) based on injury severity. Factors that push the multiplier higher include visible injuries on imaging, surgical intervention, permanent impairment, and extended recovery periods.

The per-diem method assigns a daily dollar value to your pain and multiplies it by the number of days you’ve been affected. This approach works better for injuries with clear start and end dates.

Side-impact injuries often justify higher non-economic values because door intrusion can create direct trauma to the torso, hip, and head. Rib fractures, shoulder injuries, and concussions are also common with these types of accidents.

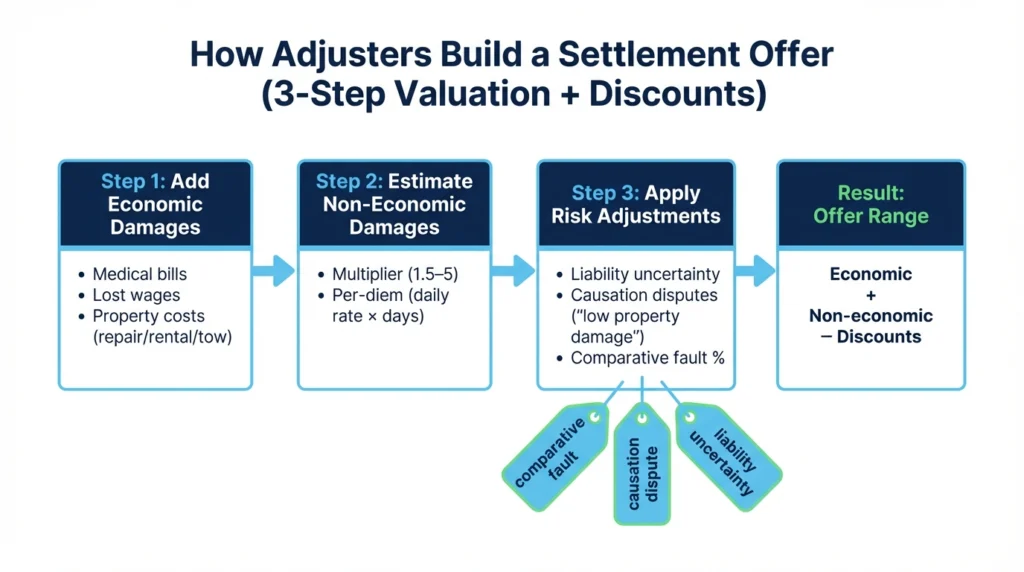

Three Steps Adjusters Take to Build Negotiation

While building a case and preparing for negotiation, insurance companies consider different factors to determine a settlement offer.

Insurance companies complete the following tasks to help them determine settlement value:

- Calculate economic damages: Add up medical bills, lost wages, and property-related costs.

- Estimate non-economic damages: Apply a multiplier or per-diem calculation based on injury severity.

- Apply risk adjustments: Discount for liability uncertainty, causation disputes, and any comparative fault percentage.

A claim with $20,000 in economic damages might support $40,000 to $60,000 in non-economic damages for moderate injuries. But if the adjuster believes you’re 20% at fault and causation is disputed, they might offer $50,000 instead of $70,000.

Property Damage: Repair vs. Total Loss

T-bone collisions can potentially cause irreversible damage to your car. If your vehicle is totaled, the insurer uses valuation reports to determine actual cash value.

Review their report carefully. Check that the comparable vehicles match your car’s mileage, condition, and features. Challenge adjustments that seem arbitrary.

Whether your car totaled or not, you may be entitled to compensation for the damage and costs associated with those damages.

Recoverable property damage includes:

- Repair costs or actual cash value if totaled

- Towing and storage fees

- Rental car or loss-of-use compensation

- Personal property damaged inside the vehicle

Diminished Value After Repairs

Even after quality repairs, your vehicle now has an accident history that reduces its resale value. This is known as diminished value, and Texas allows you to claim it against the at-fault driver’s liability coverage.

Stronger diminished value claims involve newer vehicles, documented structural repairs, and evidence showing how accident history affects market value. Supporting documentation includes pre-loss condition records, detailed repair invoices, and comparable sales data.

The at-fault driver’s property damage liability coverage typically pays diminished value claims. Your own collision coverage generally doesn’t cover this loss.

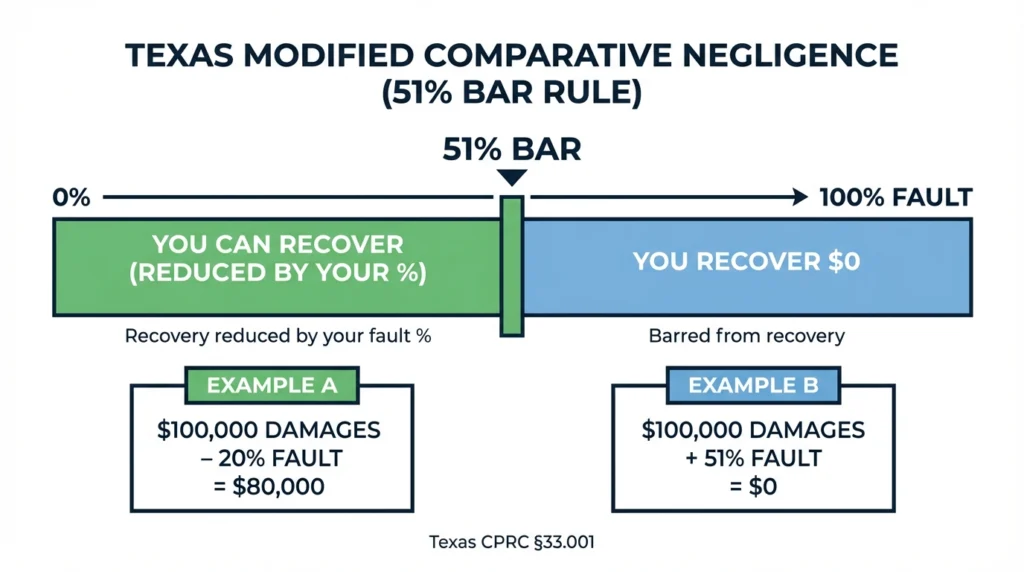

Texas Modified Comparative Negligence: The 51% Rule

Your recovery depends on your percentage of fault.

Under Texas Civil Practice and Remedies Code § 33.001, if you’re more than 50% responsible, you recover nothing. If you’re 50% or less responsible, your recovery is reduced by your fault percentage.

The math is straightforward. If your damages total $100,000 and you’re found 20% at fault, your net recovery is $80,000. If you’re found 51% at fault, you recover nothing.

Insurers push fault arguments early because shifting even 10% of the blame onto you saves them money. Common arguments that insurance companies use in T-bone cases include claiming you were speeding, that you could have avoided the collision, or that you were distracted.

Strong liability evidence shuts down these arguments. Dashcam footage showing the other driver running a red light makes it hard to blame you for the crash.

Policy Limits & Coverage Paths

Even a well-documented claim can be limited by available insurance coverage.

Texas requires minimum liability coverage of $30,000 per person, $60,000 per accident for bodily injury, and $25,000 for property damage. If the at-fault driver carries only minimum coverage and your damages exceed $30,000, you may not recover your full losses from their policy.

When the at-fault driver’s coverage is insufficient, look to your own policy. Uninsured/underinsured motorist (UM/UIM) coverage, governed by Texas Insurance Code §1952.101, can fill the gap. Medical payment coverage may help with immediate bills regardless of fault.

Exemplary Damages in Extreme Cases

Punitive damages (compensation awarded in lawsuits to punish a defendant for especially harmful actions) aren’t routine in car crashes. They require proof of extreme conduct, such as gross negligence, fraud, malice, or willful acts.

Texas Civil Practice and Remedies Code § 41.008 caps exemplary damages at the greater of $200,000 or two times economic damages plus an amount equal to non-economic damages (up to $750,000). Cases involving intoxicated drivers or intentional conduct may qualify, but most T-bone crashes don’t meet this threshold.

Why Early Offers Are Often Low

That first offer reflects the adjuster’s current risk assessment. When liability is disputed, treatment is ongoing, or future care needs are unclear, they price in uncertainty by offering less.

Here are things that can increase an early offer:

- Clear liability evidence (video, independent witnesses)

- Consistent medical documentation with objective findings

- Finalized prognosis and future care recommendations

- Credible wage-loss documentation

Settling before your injury stabilizes can underprice future care. But waiting too long creates other problems. For example, witnesses become harder to locate, and evidence degrades. The safest time to evaluate an offer is after your diagnostic workup is complete, your treatment plan is established, and your limitations are documented.

When to Talk to a Lawyer

An attorney can help preserve evidence, present your claim effectively, document future damages, negotiate from a stronger position, and navigate UM/UIM coverage when needed.

Certain situations signal that your claim’s value is being unfairly discounted and that you should speak with an attorney.

These include:

- The insurer is pushing fault toward 51% or higher.

- They’re using “low property damage” to dispute injury causation.

- Surgery or long-term care is on the horizon.

- The at-fault driver has low policy limits.

Our attorneys at Angel Reyes & Associates have recovered more than $1 billion for clients across Texas, and we’ve spent over 30 years handling cases exactly like yours. We have extensive experience handling car accident, truck accident, rideshare accident, and wrongful death claims.

We offer free consultations and work on contingency, meaning you pay nothing unless we win. If you’re dealing with a T-bone crash in Texas, contact us to discuss your situation. We’re available 24/7.

T-Bone Wreck FAQs

What if the police report blames the wrong driver in a T-bone crash?

A police report can influence negotiations, but it is not the final word on fault. Video, witness statements, vehicle damage, and other evidence can still change how the insurer evaluates the claim.

Can a pre-existing injury still be part of a Texas car accident claim?

Yes, if the crash made an existing condition worse, that added harm may still be eligible for compensation. Insurance companies will verify any pre-existing conditions and require clear medical records showing what changed after the collision.

Who pays if the other driver was working at the time of the crash?

If the driver was acting within the scope of their job, their employer’s commercial insurance may also be involved. That can affect both the investigation and the amount of coverage available.

Do I have to use the insurance company’s repair shop after a side-impact crash in Texas?

No. In Texas, you generally have the right to choose your own repair shop, even if the insurer suggests a preferred one.

About the Authors

Spencer Browne

Writer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials across Texas. He focuses on car, truck, and wrongful death cases, with notable verdicts including a landmark win in the Choctaw Casino bus crash case. A recognized speaker and legal educator, Spencer is a member of the American Board of Trial Advocates and has been honored as a Texas Super Lawyer and one of D Magazine’s Best Lawyers in Dallas. He brings deep trial experience and relentless advocacy to every client he represents.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...