What Is the Average Settlement for a Car Accident in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- No single average applies; Texas settlement value depends entirely on your case facts.

- Rideshare and truck crashes carry higher coverage that can raise settlement value.

- 2-year deadline to file – contact attorney immediately for maximum compensation

You are sitting at your kitchen table in San Antonio with a stack of medical bills and a first offer from an insurance adjuster. The number feels low, but you have no way to know for sure. You don’t know anyone you can ask, and you can’t seem to find a consistent number or any reasonable advice on the internet about the average settlement for a car accident in Texas.

You want a benchmark—something to tell you whether to sign or push back. Unfortunately, there really isn’t one, and there are several reasons why that number does not exist.

Why There Is No Single Average

No fixed average applies to Texas car accident settlements because value depends entirely on the facts of your case. Any published “average” you find online is misleading. Law firms, industry writers, and other information resources can all influence their data with a few key decisions. For example, some blend minor fender-benders with catastrophic injury claims into a number that fits neither.

Actual settlement values in Texas are driven by variables, not a formula. Injury severity, medical costs, lost income, and who was at fault all pull the number in different directions. Understanding those variables gives you a real framework for judging an offer.

These variables also explain why two similar crashes can settle for very different amounts. A soft-tissue neck strain and a spinal injury are not the same claim, even if both were the result of a rear-end accident. Learning how each factor works helps you spot an offer that shortchanges you.

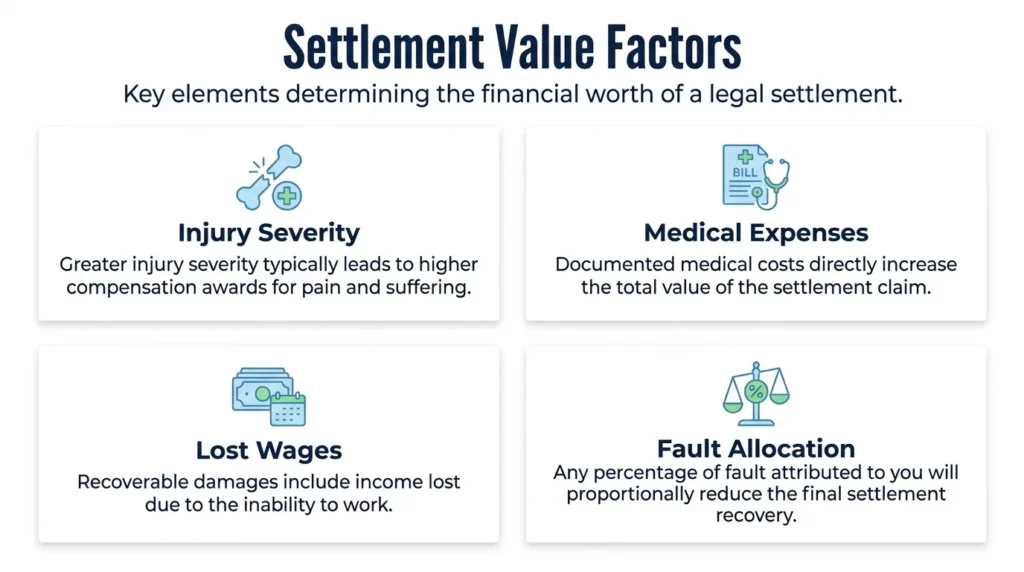

Factors That Affect Settlement Value

Four variables shape most Texas settlements:

- Injury severity

- Medical expenses

- Lost wages

- Fault allocation

Serious injuries with high medical bills and long recovery times carry more value. Minor injuries with quick recoveries settle for less.

The last factor is one that people’s perception of their case often overlooks. Fault matters for case value as much as the nature of injuries and losses.

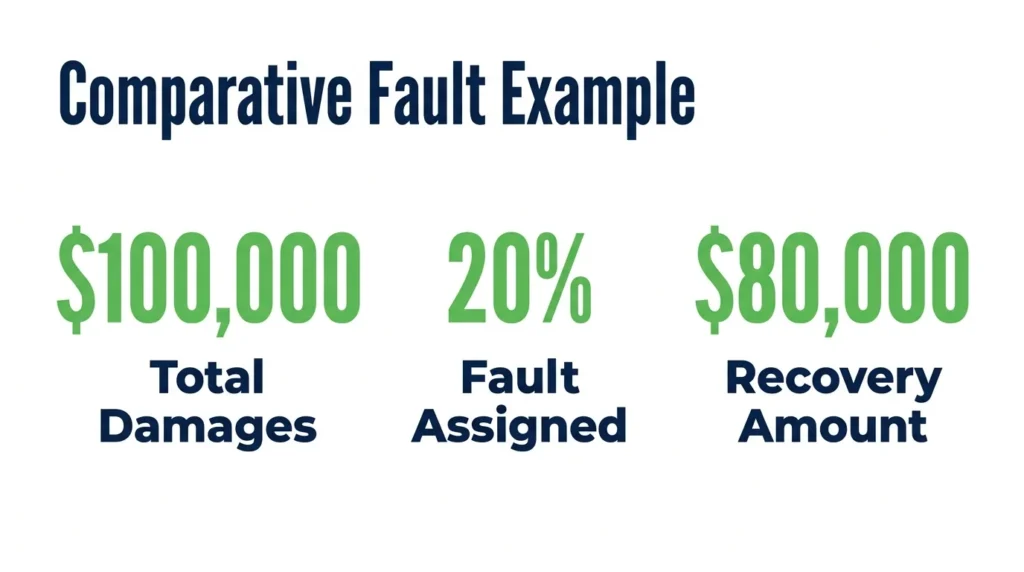

Texas uses modified comparative fault under Texas Civil Practice and Remedies Code Chapter 33. To put it simply: if you are 50 percent or less at fault, your recovery drops by your fault percentage. If you are more than 50 percent at fault, you recover nothing.

Here is how that works in practice. Say your damages total $100,000 and you are found 20 percent at fault. Under this law, your recovery falls to $80,000. Fault allocation is often where insurers fight hardest because shifting blame onto you directly cuts what they have to pay.

Insurance limits also set a practical ceiling on recovery. The at-fault driver’s insurance caps what they will pay at the limit of their policy, no matter how large your damages. Texas Transportation Code Section 601.072 sets minimum liability coverage, and many drivers carry only that minimum. When damages exceed the policy, recovery can require other sources.

A first offer from an adjuster rarely reflects full value. Adjusters open low and rely on you to accept quickly. Strong documentation of your injuries and losses supports a higher number.

Economic Damages

Economic damages are your tangible, documentable losses. These include medical bills, lost wages, future medical care, and property damage. Each one can be backed by a receipt, a pay stub, or a treatment estimate.

Documentation drives the recoverable amount. The more clearly you can prove a dollar figure, the harder it is for an insurer to dispute it. Keep every bill and record.

Non-Economic Damages

Non-economic damages cover intangible losses. These include pain and suffering, mental anguish, and loss of enjoyment of life. They are real harms, but no receipt exists for them.

Because they are subjective, these damages are harder to quantify and vary widely by case. A permanent injury that changes daily life supports far more than a short-term bruise. This is often where experienced negotiation makes the biggest difference.

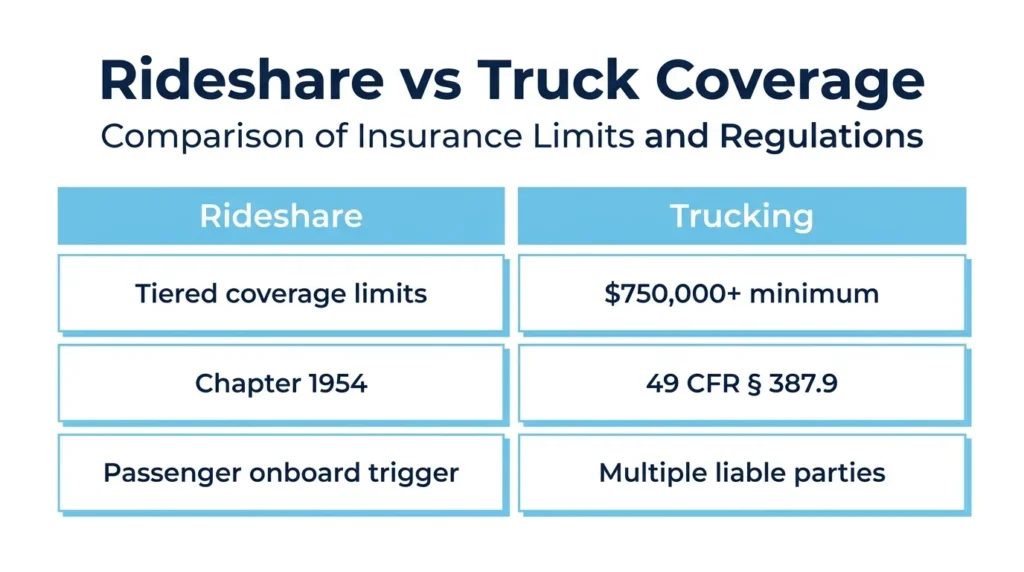

Rideshare & Truck Accident Settlements

Some accident types carry much higher available insurance coverage, which can raise the settlement ceiling. Rideshare and commercial trucking crashes are the clearest examples. Both involve coverage structures far larger than a standard driver’s minimum policy.

Rideshare Accident Settlements

Rideshare coverage in Texas depends on what the driver was doing at the moment of the crash. Texas Insurance Code Chapter 1954 sets tiered requirements for transportation network companies like Uber and Lyft. The tier depends on whether the driver was offline, waiting for a request, or carrying a passenger.

When the driver is actively transporting a passenger, the highest coverage tier applies. That coverage can far exceed a standard auto policy. Higher available limits can materially increase your compensation.

Commercial Truck Accident Settlements

Commercial carriers must carry far higher minimum liability coverage than everyday drivers. Under 49 CFR § 387.9, many trucking companies must carry at least $750,000 in coverage, and often much more.

Those larger policies change the math. Trucking cases also often involve multiple liable parties, such as the driver, the carrier, and a maintenance contractor. More policies and higher limits can raise settlement value well beyond a typical car crash.

Case Results & Estimating Your Claim

If you’re still not sure where to even begin with analyzing your case, Angel Reyes & Associates has an answer for you. We have put together an intuitive, easy-to-use case calculator using compiled data from real-world cases. Simply work through the short questionnaire to the best of your ability and the calculator will give you a broad range for what your case might be worth.

However, keep in mind that this is not a complete picture, so any value ranges it provides are purely figurative and for your own educational purposes. A case value estimate can serve as a starting framework. It can help you form rough expectations before you talk to anyone. Just treat any estimate as a starting point, not a substitute for a full case evaluation by an attorney.

Documented outcomes show how much settlement value depends on the specific facts. Reading through real outcomes of some of the accident cases we have handled can provide a more honest picture than any average.

Reading real client experiences adds useful context about the process as well. Keep in mind that past results never predict a specific outcome. Every case turns on its own facts, and no prior recovery guarantees yours.

Review Your Options with an Attorney

No matter the facts of your case, one constraint applies: you have a deadline to file. Under Texas Civil Practice & Remedies Code § 16.003, you generally have two years from the crash date to file a lawsuit. Miss that window and your claim can be barred entirely. Insurers know this, and they’re hoping you don’t.

If you’ve been hurt in an accident and you want to learn more about what your case might be worth, Angel Reyes & Associates offers that evaluation at no cost. Our experienced attorneys have handled accidents across Texas for more than 30 years. Consultations are completely free, and you pay no fee unless we win.

Our team has recovered more than $1 billion recovered for clients across Texas. We handle the adjusters and the paperwork so you can focus on healing. If an offer is on the table or your bills are piling up, do not sign any offers before you know your options.

Reach out to our team through our contact page or give us a call today. We can review your case and evaluate what it may realistically be worth.

Average Settlement FAQs

Can I still recover compensation if the at-fault driver in Texas had no insurance?

Texas law requires drivers to carry minimum liability coverage, but uninsured drivers are common on Texas roads. If you carry uninsured or underinsured motorist coverage on your own policy, that coverage can step in to compensate you when the at-fault driver has no insurance or not enough.

Does Texas allow me to recover damages for a loved one's death in a car accident?

Yes. Texas law allows certain family members to bring a wrongful death claim under Texas Civil Practice and Remedies Code Chapter 71 when a crash causes a fatality. Recoverable damages can include loss of financial support, loss of companionship, and mental anguish suffered by surviving family members.

How does a pre-existing injury affect my Texas car accident claim?

A pre-existing condition does not automatically bar your recovery in Texas. Under the “eggshell plaintiff” rule, a defendant takes the victim as they find them, meaning they can be held responsible for aggravating a prior injury even if a healthy person would have suffered less harm.

Will my medical bills get paid while my Texas car accident claim is still open?

Texas does not require at-fault drivers’ insurers to pay your medical bills as they come in during an open claim. You may need to use your own health insurance, MedPay coverage, a medical lien arrangement, or a Letter of Protection with your provider while the case resolves.

Does Texas require me to report a car accident to the state?

Texas law requires an investigating law enforcement officer to file a written crash report with TxDOT if the accident caused injury, death, or property damage over $1,000. If no officer investigates, drivers are no longer required to self-file a report with the state as of 2017. However, you should still document the crash and report it to local police if possible, since the lack of an official report can create complications for your claim.

About the Authors

Spencer Browne

Writer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials across Texas. He focuses on car, truck, and wrongful death cases, with notable verdicts including a landmark win in the Choctaw Casino bus crash case. A recognized speaker and legal educator, Spencer is a member of the American Board of Trial Advocates and has been honored as a Texas Super Lawyer and one of D Magazine’s Best Lawyers in Dallas. He brings deep trial experience and relentless advocacy to every client he represents.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...