Does Insurance Cover Road Rage Accidents in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas auto insurers may deny road rage claims under an "intentional act exclusion," but your own UM/UIM, PIP, and collision coverages may still apply.

- Evidence collected immediately after a road rage crash often determines how insurers classify the incident and whether coverage is available.

- If the at-fault driver's insurance denies your claim, request the denial in writing and promptly file claims under your own policy while preserving evidence for potential legal action.

You were driving home on I-10 near the Galleria area when another driver cut you off, then slammed on their brakes. Before you could react, they reversed into the front end of your car. Now you’re dealing with injuries, a damaged car, and an insurance adjuster who says the crash was “intentional” and won’t be covered.

Road rage accidents create unique insurance problems. The label an insurer puts on the crash can determine whether anyone pays for your losses. Understanding how Texas auto insurance handles these situations helps you protect your claim and find coverage that may still apply.

Why Road Rage Crashes Create Insurance Coverage Problems

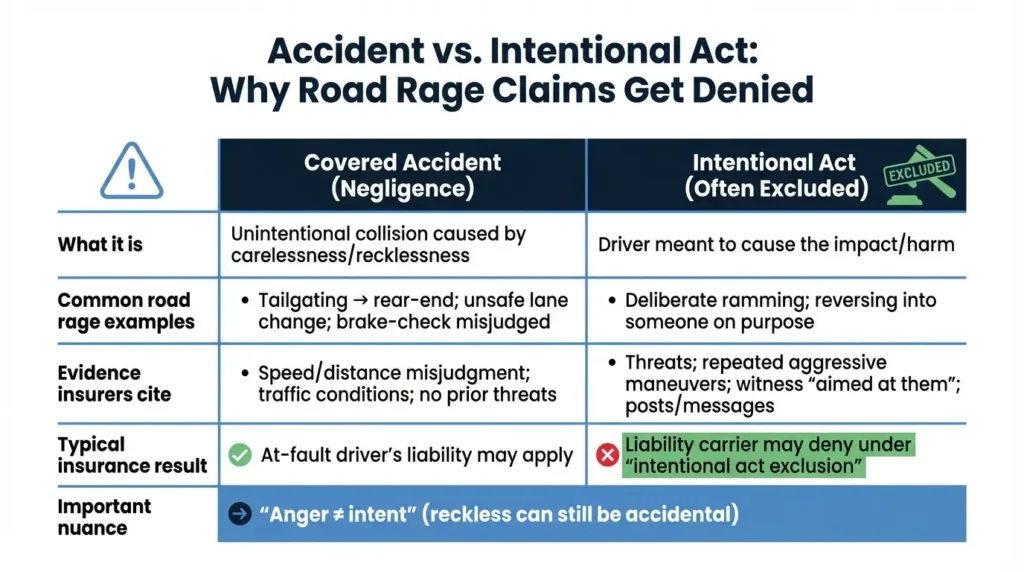

Insurance policies are designed to cover accidents (i.e., car accidents, truck accidents, rideshare accidents, etc.), meaning unintentional events caused by negligence. When a driver deliberately uses their vehicle as a weapon, insurers may argue that the collision falls outside what the policy covers.

Whether a crash was accidental or intentional matters for two reasons: First, it affects whether the at-fault driver’s liability insurance will pay your claim. Second, it determines what coverage you might be eligible for if their insurer denies responsibility.

Road rage accidents often involve a gray area. Did the other driver lose their temper and make a reckless mistake, or did they intentionally aim their vehicle at you? The answer isn’t always clear, and insurers may interpret the facts in ways that favor denial in order to avoid paying you.

When the At-Fault Driver’s Liability Insurance May Deny Your Claim

According to the Texas Department of Insurance, most insurance policies do not cover accidents that were caused intentionally. This provision allows insurers to deny claims when the policyholder deliberately caused harm.

In road rage cases, the other driver’s insurance company may investigate whether the collision was truly an accident. If they determine their insured meant to hit you, they can deny your claim entirely.

How Insurers Determine Whether a Crash Was an Accident or an Intentional Act

Insurers look for evidence suggesting the at-fault driver intended for the collision to happen.

Evidence may include:

- Threats made before the crash

- Repeated aggressive maneuvers

- Witness accounts of deliberate ramming

- Social media posts

Anger alone doesn’t automatically equal intent. A driver who loses their temper and makes a split-second, reckless decision may still have acted negligently rather than intentionally. However, insurers often interpret ambiguous facts in their favor.

The sequence of events also matters. If a collision happened first and violence followed afterward, different parts of the incident may receive different coverage treatment. A crash caused by aggressive tailgating might be covered, while injuries from a physical assault after both drivers exited their vehicles might not.

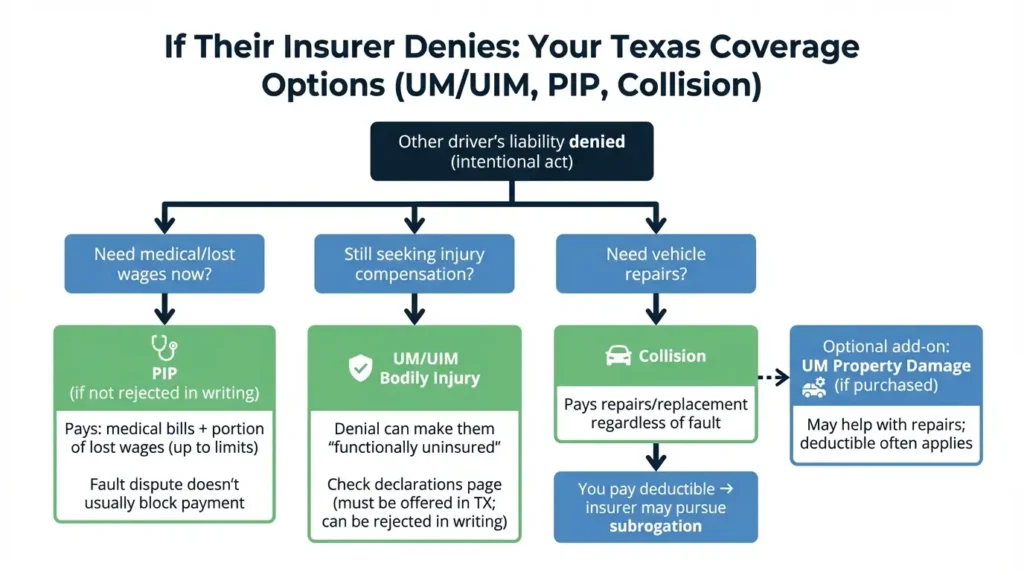

You May Still Be Eligible for Coverage Even When the Other Insurer Denies

According to the Texas Office of Public Insurance Counsel, even if the at-fault driver’s liability carrier refuses to pay, your own policy may provide coverage options.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

When the at-fault driver’s insurer denies coverage, that driver becomes functionally uninsured from your perspective. This is where UM/UIM coverage can become your primary recovery tool.

Under Texas Insurance Code Chapter 1952, insurers must offer UM/UIM coverage to Texas policyholders. You can reject it in writing, but if you didn’t, you likely have it. Check your declarations page to confirm.

UM coverage pays when the at-fault driver has no insurance. UIM coverage pays when their insurance exists, but doesn’t fully cover your losses. Both can apply to bodily injury claims. If you purchased UM/UIM property damage coverage, it may help with vehicle repairs, too, though a deductible typically applies.

Personal Injury Protection (PIP)

PIP coverage pays certain injury-related expenses quickly, without waiting for fault determinations. This can be critical while liability disputes play out.

PIP typically covers medical bills and a portion of lost wages up to your policy limits. It pays regardless of who caused the crash, which means intentional-act disputes don’t block it the same way they block liability claims.

Texas insurers must offer PIP coverage, but you can reject it in writing. If you’re unsure whether you have PIP, review your policy or call your insurance company.

Collision Coverage

Collision coverage pays to repair or replace your vehicle after an impact, regardless of fault. If the other driver’s insurer denies your property damage claim, your collision coverage can keep repairs moving.

You’ll pay your deductible upfront. However, your insurer may pursue the at-fault driver through subrogation (an insurer’s legal right to recover the costs they paid for your claim from the party who actually caused the accident). If they recover money, you may get your deductible back.

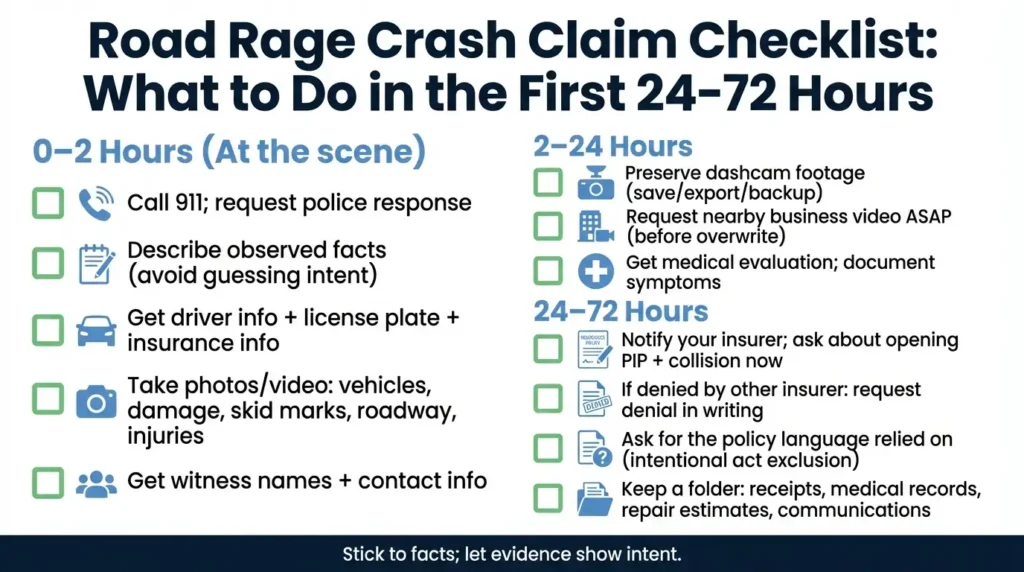

What to Do Immediately After a Road Rage Crash to Strengthen Your Claim

The steps you take in the first hours and days after your crash can shape how the insurance company classifies the crash and whether your claim succeeds.

Call 911 and request a police response. When speaking with officers, describe what you observed without speculating about the other driver’s mental state. Let the evidence speak for itself. A police report creates an official record that’s harder for insurers to dismiss.

Preserve every piece of evidence you can. Dashcam footage, phone videos, photos of damage, the other driver’s license plate, and witness contact information all matter. If nearby businesses have security camera footage, request it quickly before it’s overwritten.

Document your injuries thoroughly. Seek medical attention promptly and keep records of every appointment, diagnosis, and symptom. This documentation supports both PIP claims and any UM/UIM injury claim you may need to file.

Reporting & Claim Notice

Notify your insurance company promptly. Ask about opening PIP and collision claims while liability questions are investigated. You don’t have to wait for the other driver’s insurer to make a decision before using your own coverage.

If the other driver’s insurer denies your claim, request the denial in writing. Ask for the specific policy language they’re relying on. Understanding their stated basis helps you evaluate your options and build a response.

When giving statements to any insurance company, stick to observed facts. Avoid speculation about what the other driver intended. Let your evidence tell the story.

What to Do When Insurance Coverage Falls Short

Some road rage incidents involve criminal conduct that opens additional resources for victims.

The Texas Crime Victims’ Compensation Program may help cover certain expenses when you’re the victim of a violent crime. Eligibility requirements apply, and the program has limits, but it’s worth exploring if your injuries are serious and insurance coverage is inadequate.

If criminal charges are filed against the other driver, restitution may be ordered as part of their sentence. This is separate from civil recovery and depends on the criminal case outcome.

Keep all receipts and medical records organized. Whether you’re pursuing insurance claims, crime victim compensation, or a lawsuit, thorough documentation strengthens every path to recovery.

When to Talk to a Texas Car Accident Lawyer

Road rage coverage disputes can involve multiple insurers, competing exclusions, and complex injury documentation.

Consider speaking with an attorney if you’re facing severe injuries, a disputed intent classification, UM/UIM delays, or a denial letter citing exclusions.

An experienced lawyer can organize evidence, communicate with carriers, coordinate claims across PIP, UM/UIM, and collision coverages, and evaluate whether a lawsuit against the other driver makes sense.

At Angel Reyes & Associates, we’ve spent over 30 years helping Texas crash victims recover compensation. We offer free consultations and work on contingency, meaning no fees unless we win. Our attorneys have recovered more than $1 billion for clients across the state.

If a road rage crash has left you dealing with injuries, vehicle damage, and insurance denials, contact us today to discuss your options.

Road Rage FAQs

Does MedPay help after a road rage crash in Texas?

Maybe. Medical Payments coverage, if you bought it, can help pay medical bills regardless of fault, but unlike PIP, it usually does not cover lost wages.

Do I have to pay a deductible to use UM property damage coverage in Texas?

Often yes. In Texas, UM property damage claims commonly involve a deductible, though the amount depends on the policy.

Can a passenger make an insurance claim after a road rage crash?

Usually yes. An injured passenger may have rights under the at-fault driver’s liability coverage if it applies, and may also be covered under PIP or UM/UIM, depending on the policies involved.

Will a criminal case automatically force the insurance company to pay?

No. A criminal charge or conviction can support your evidence, but insurance coverage still depends on the policy language and the specific facts of the incident.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...