Does Uber Cover Accidents?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Uber covers accidents in Texas, but the policy that applies depends on the driver's app status.

- Periods 2 and 3 trigger Uber's $1 million primary liability policy for injured passengers and others.

- Period 1 offers only contingent coverage of $50,000 per person after the personal insurer denies the claim.

You were riding home from a late dinner near The Pearl in San Antonio when your Uber driver ran a stop sign and clipped another car. Your shoulder slammed into the door. Now you’re staring at an emergency room bill and wondering whether the rideshare company will pay your medical expenses or whether you’re on your own.

Does Uber cover accidents? The short answer is yes: Uber carries insurance that can cover its passengers. The longer answer depends on what the driver was doing at the exact moment of the crash.

How Uber Covers Accidents in Texas

Uber maintains accident insurance required under Texas law. This coverage is not optional and not discretionary. The amount available and the policy that applies depend on the driver’s status when the crash occurred. Per state law, three time periods govern which policy applies. Passengers, pedestrians, and other drivers may all have a covered claim, depending on which period was active.

The Texas Department of Insurance explains the basics in its rideshare insurance guide for consumers. The document exists because most personal auto policies exclude commercial driving, which would otherwise leave injured people without a payer.

Knowing which time period applied to your crash is the first real question in any rideshare accident claim. Get that wrong and you may chase the wrong insurer for months.

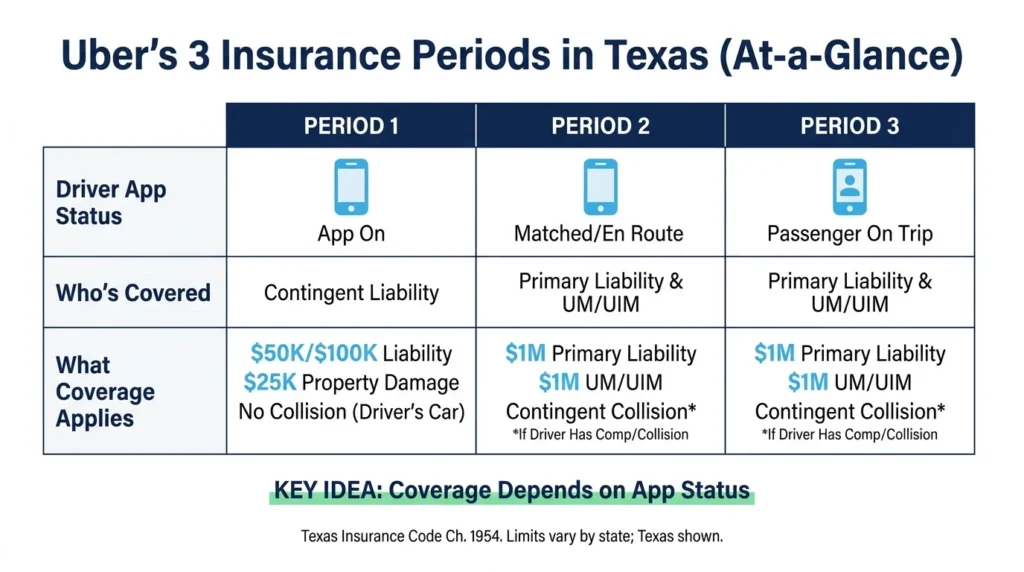

Uber’s Three Coverage Periods

For transportation network company coverage, each period has a different coverage level, based on the driver’s status on the rideshare app at the time of the accident. Texas Insurance Code Chapter 1954 is the controlling statute. Period 1 is the most commonly misunderstood and the source of most coverage disputes.

Period 1: App On, No Rider Matched

The driver is logged in to the Uber app but has not yet accepted a ride. During this window, Uber provides contingent liability coverage: $50,000 per person for bodily injury, $100,000 per accident, and $25,000 for property damage.

Uber’s Period 1 policy is described as contingent liability coverage, meaning it goes into effect when the driver’s personal policy does not cover the loss. Under Texas Insurance Code § 1954.055, Uber’s coverage is not contingent on the personal insurer first denying the claim, but in practice, most personal policies exclude commercial use, which means Uber’s coverage is often the only policy that responds during this time period. Uber does not provide collision coverage for the driver’s own vehicle at this point.

Periods 2 & 3: Rider Matched or On Board

Period 2 starts when the driver accepts a ride and is heading to the pickup point. Period 3 begins when the passenger gets into the car and ends when the ride is over. Both periods share the same policy.

Uber’s $1 million primary liability policy kicks in the moment the driver is matched with a rider and stays active for the entire trip. Primary means that the policy responds first. The driver’s personal insurance carrier does not have to deny anything for it to apply.

Uber also carries $1 million in uninsured and underinsured motorist coverage during periods 2 and 3. This protects passengers and the driver when the person at fault either doesn’t have insurance or not enough coverage. Contingent collision coverage for the driver’s own vehicle may apply during these periods if the driver carries comprehensive and collision on a personal policy, subject to a deductible.

If you are weighing a settlement, looking at average settlement values for Uber accidents in Texas can give you a sense of what claims similar to yours have produced.

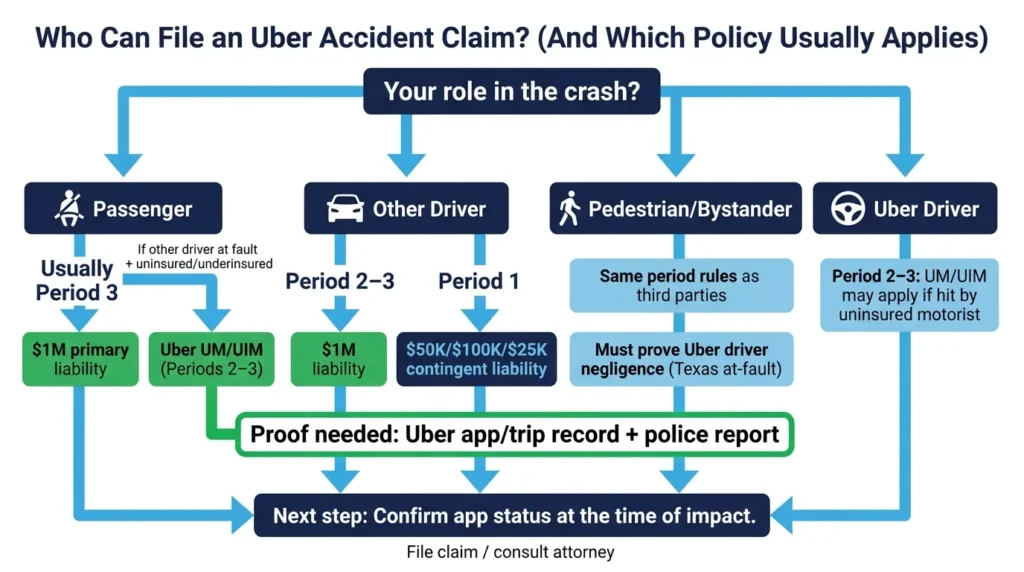

Who Can File a Claim After an Uber Accident?

Three positions cover most situations: passenger, driver of another vehicle, or pedestrian. Each follows the same period-dependent analysis, but the path looks different.

Passengers in an active Uber ride are in the strongest position. Period 3 means that the $1 million primary policy applies to your injuries. If the at-fault driver is someone other than your Uber driver and they carry no insurance, Uber’s $1 million uninsured or underinsured motorist (UM/UIM) coverage can also respond. These coverage requirements are set by Texas Insurance Code Chapter 1954.

Drivers of other vehicles hit by an Uber driver follow the period rules, too. If the Uber driver was matched with a rider or had a passenger aboard, the $1 million liability policy applies. If the driver was in Period 1, the contingent coverage and lower limits apply.

Pedestrians and bystanders use the same period-based path as other third-party claimants. Texas is an at-fault state, which means you must show that the Uber driver’s negligence caused the crash before any policy pays.

Uber drivers themselves are not left out. A driver injured by an uninsured motorist during Period 2 or 3 can access the UM/UIM policy.

Steps to Take After an Uber Accident in Texas

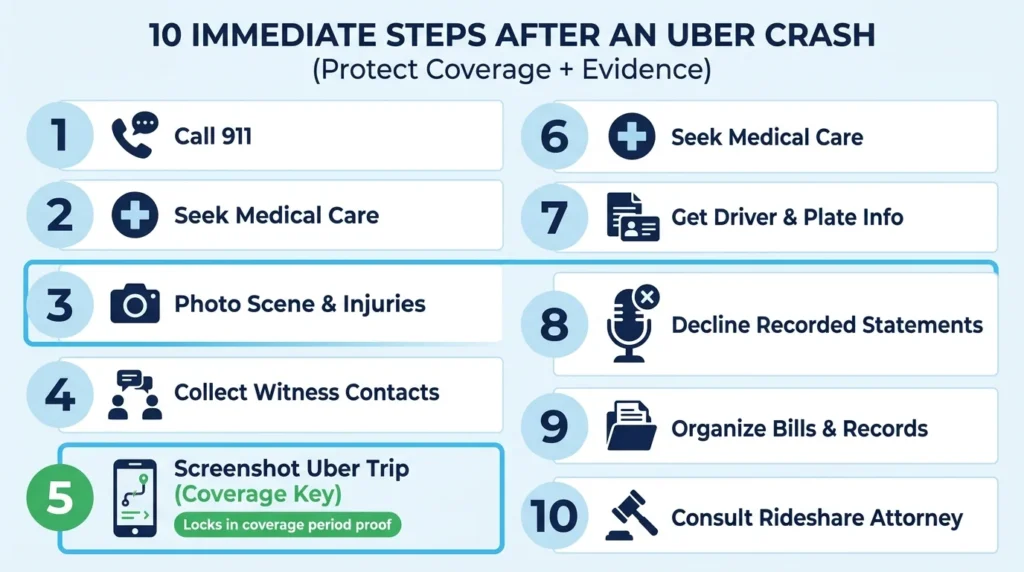

What you do in the first hours after the crash shapes your claim. What period the Uber driver was in determines coverage, and the proof of which period was active can fade fast.

Call 911 and get medical attention. A medical record creates a treatment timeline that supports your claim later. Take photos of the scene, all vehicles, the Uber driver’s identification, and any visible injuries.

Take a screenshot of the trip in your Uber app right away. The trip receipt or trip history confirms the ride was active and which period applied. If you were a passenger, this single screenshot can settle the period question before it becomes a dispute.

Do not give recorded statements to any insurer before talking with an attorney. Insurers may use early statements to limit what they pay. Uber’s insurance carrier and the driver’s personal insurer may both contact you, and the period rules determine who is actually responsible.

Reviewing how Uber accident settlements work in Texas can help you understand the rideshare claim process generally, since the period structure is similar for companies.

Work with a Texas Rideshare Accident Attorney

Uber accident claims involve multiple insurers, period-dependent coverage rules, and Texas at-fault analysis. That combination is hard to handle alone, especially while you are recovering from injuries and watching bills add up.

Angel Reyes & Associates has represented Texans injured in Uber and Lyft crashes for decades. We have recovered significant verdicts and settlements for clients across our practice. We work on contingency, which means we receive no fee unless we win. And consultations are always free.

Contact us today to talk through what happened and figure out which Uber policy should be paying your claim.

Past results do not guarantee future outcomes.

Uber Coverage FAQs

Can Uber's insurance company deny a valid injury claim, and what options do I have if it does?

Uber’s insurer can dispute or deny claims, just like any other insurer. In Texas, you can file a complaint with the Texas Department of Insurance or pursue the claim through litigation if a denial is wrongful or made in bad faith.

Does Uber carry coverage for accidents that happen in parking lots or on private property?

Uber’s period-based coverage follows the driver’s app status, not the type of roadway. If the driver was in Period 1, 2, or 3 at the time of the crash, the applicable Uber policy can respond regardless of whether the accident happened on a public street or on private property.

How long do I have to file a personal injury claim after an Uber accident in Texas?

Texas has a two-year statute of limitations for personal injury claims, meaning you generally must file suit within two years of the accident date. Missing that deadline typically bars you from recovering anything, no matter how strong the evidence is.

What if the Uber driver was logged in to both Uber and Lyft at the same time when the crash happened?

When a driver is logged in to multiple apps, known as simultaneous or dual-app driving, coverage disputes between the platforms can arise over which company’s policy applies. Each company’s insurer may argue that the other bears primary responsibility, which can slow the claims process significantly.

Does Uber cover accidents that happen outside Texas if I am a Texas resident?

Uber’s coverage applies based on where the trip takes place, not where the rider lives. The insurance laws and period requirements of the state where the crash occurred govern which policy responds and at what limits.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...