A Texas Car Insurance Buyer’s Guide: Coverages, Premiums & More

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas drivers pay around $2,500 per year on average for auto insurance, making it one of the most expensive states in the country for coverage.

- The state's 30/60/25 liability minimums are a legal requirement, not a safety net — serious accidents frequently produce costs that far exceed those limits.

- Discounts for bundling, defensive driving, and telematics programs can significantly reduce your premium, but comparing quotes across carriers every one to two years remains the most reliable way to avoid overpaying.

Sure enough, it’s happened again. You might be wondering if it’s time to take your business elsewhere.

If this sounds like an all-too-familiar situation, you aren’t alone. Texas drivers fork over billions of dollars per year for coverage, so it’s only natural to want to keep your costs as low as possible. If you’re looking to switch providers or make some significant changes to your policy, then this guide has a wealth of information to help you make informed decisions regarding your auto insurance protection.

How Much Is Car Insurance in Texas?

According to Insurify, a website for shopping around and comparing auto insurance quotes, Texas drivers pay around $2,500 per year for auto insurance, or just a little over $200 per month. This is one of the highest rates in the nation, exceeding national averages by 15 to 20 percent.

However, your exact cost can vary from this number wildly. According to Insurance.com, Texas auto policies can start as low as around $50 per month, but the type of protection you get for this value is dramatically lower than the average policy purchased in the state.

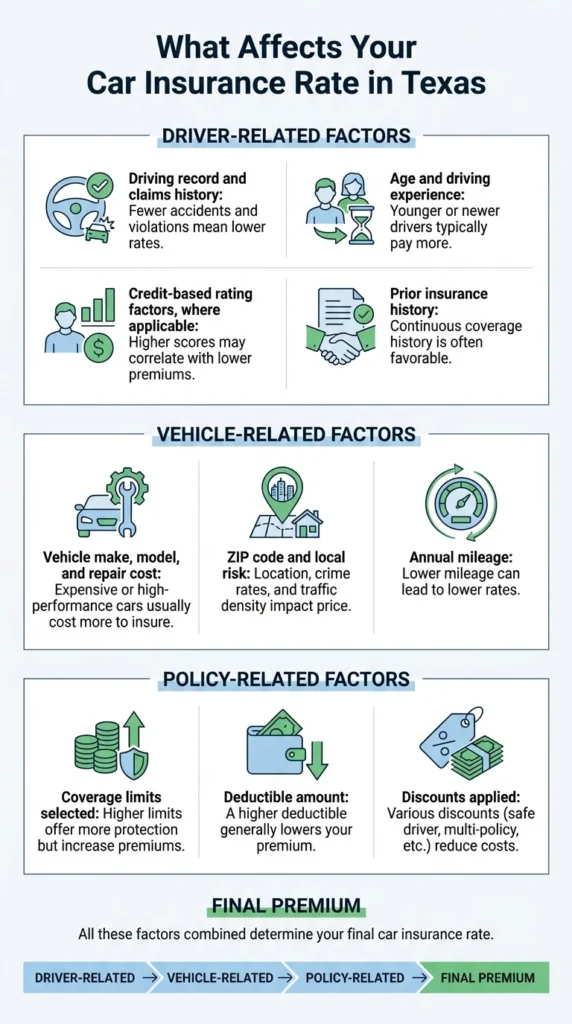

Factors That Influence Your Premiums

Your specific insurance rates will depend heavily on a multitude of factors. Here are just a few of them:

- What kind of car are you insuring? It’s much cheaper to insure a small, inexpensive commuter car like a Toyota Corolla or Hyundai Accent than it is to secure a larger luxury SUV like a Lexus or GMC. Generally, the more expensive the car, the more expensive it will be to insure.

- Who is driving the vehicle? Is this car going to be primarily driven by a teenager who just got their license, or a driver who has been behind the wheel for decades? Even so, how’s your driving record? Do you have any accident history, speeding tickets, or other moving violations on your record? Drivers who violate road laws are statistically more likely to be in an accident, so their coverage will likely cost more.

- How old is the vehicle? Two identical cars built 10 years apart could have notably different insurance rates. An older car is worth less, and therefore costs less to insure vs. a brand-new model.

- Where does the driver live? Those who live in urban areas or who frequently park on the street might pay higher rates than those who live in a rural or sparsely populated area. Accidents and theft rates are higher in densely populated cities, which can drive rates up.

Want to see for yourself how these factors can impact your monthly premiums? Check out our calculator tool up above to see an estimate of how various changes could impact your insurance rate.

Types of Insurance Policies Offered in Texas

Texas insurers offer several types of auto coverage, and understanding what each one does is the first step toward building a policy that actually protects you when you need it.

Liability coverage is the only type the state legally requires. It pays for the other party’s injuries and property damage when you are at fault, but it does not cover your own vehicle or your own medical bills.

Collision coverage pays to repair or replace your vehicle after a crash, regardless of who caused it. Comprehensive coverage handles damage from events outside your control, including hail, flooding, fire, falling objects, and theft. For a closer look at the differences, see our breakdown of collision, comprehensive, and liability coverage.

Texas weather alone is reason enough to take comprehensive coverage seriously. If you’re financing or leasing your vehicle, your lender will almost certainly require you to carry both.

Personal Injury Protection (PIP) and MedPay both cover medical expenses for you and your passengers after a crash, regardless of who was at fault. Texas law requires insurers to include PIP in every policy automatically. If you don’t want it, you’ll need to reject it in writing.

Finally, Uninsured/Underinsured Motorist (UM/UIM) coverage steps in when the at-fault driver either has no insurance or does not have enough insurance to cover your losses. Texas consistently ranks as one of the leading states for the number of uninsured drivers, which makes this coverage especially worth carrying. Our guide on PIP, MedPay, and UM/UIM coverage breaks down each option and what it costs to add.

When liability, collision, comprehensive, PIP, and UM/UIM are combined, that is what most people call full coverage car insurance.

Important Factors to Consider When Buying Insurance in Texas

Legal Minimums & Policy Limits

Texas law requires every driver to carry at least $30,000 in bodily injury liability per person, $60,000 per accident, and $25,000 in property damage liability (commonly written as 30/60/25). These numbers represent the minimum, not a recommended level of protection.

A single serious accident can generate medical bills and property damage that far exceed those limits. When that happens, the at-fault driver can be held personally responsible for whatever the insurance doesn’t cover.

Carrying higher limits on your policy does increase your premiums, but it provides real protection for your savings, your home, and your income. For a full breakdown of what the law requires and why minimum coverage is often not enough, see our guide to Texas minimum car insurance requirements. The Texas Department of Insurance also maintains a consumer guide that explains your rights and what insurers are required to offer you.

Deductibles

Your deductible is the amount you pay out of pocket before your insurer covers the rest of a collision or comprehensive claim. A higher deductible means a lower monthly premium, but it also means a larger bill when you actually file a claim.

The right deductible depends entirely on your financial situation. If writing a $1,000 check tomorrow would create a genuine hardship, a lower deductible is worth the extra monthly cost. Our guide on how auto insurance deductibles work in Texas walks through the tradeoffs so you can make a decision that fits your budget.

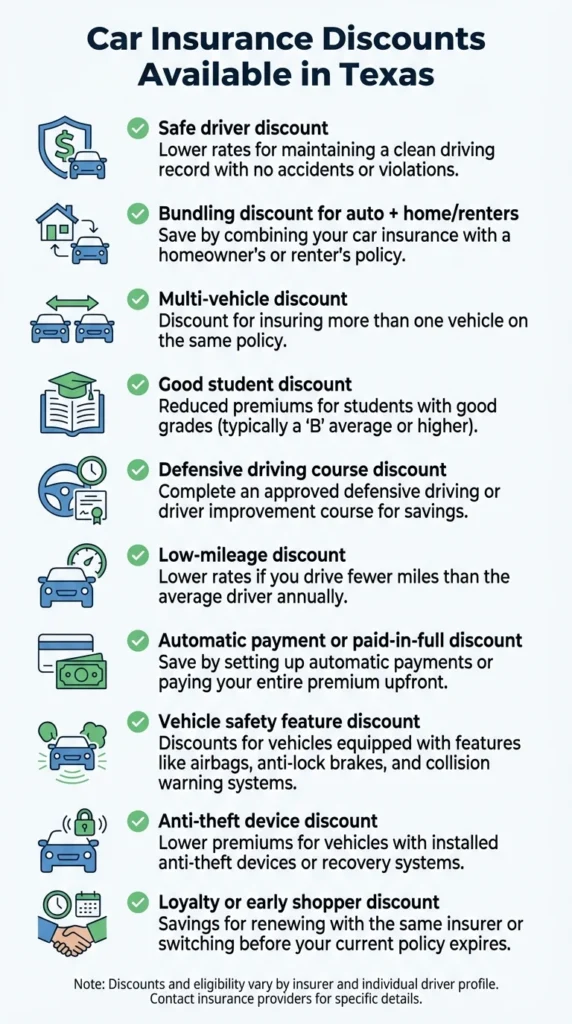

Available Discounts

Most Texas insurers offer a range of discounts that can meaningfully reduce your premium. Common opportunities include:

- Bundling your home and auto policies with the same carrier (typically 10–26% savings).

- Completing a defensive driving course can save you 5–10% on qualifying coverages for up to three years.

- Telematics or usage-based programs track your driving habits and can reward safe, low-mileage drivers with savings, sometimes as high as 40%.

- Good student discounts may apply for teen drivers on the policy with strong academic records

- Low mileage discounts for drivers who log significantly fewer miles than the state average

Discounts can often be stacked, so it’s worth asking your insurer exactly what you qualify for every time you renew.

Enrollment Requirements

When you apply for a policy, insurers evaluate several factors beyond your driving record. One of the most impactful is your credit score. Texas law permits insurers to use credit-based insurance scoring when calculating premiums, and the difference between good and poor credit can be significant. Drivers with weaker credit histories can pay considerably more for the same level of coverage compared to those with strong scores.

Understanding how this works gives you the opportunity to take steps that lower your rate over time. Our article on how credit scores affect car insurance rates in Texas covers the mechanics of credit scoring and what options are available to you.

Customer Satisfaction

Price matters, but it is not the only factor worth weighing. An insurer that is slow to pay claims, difficult to reach after a crash, or quick to deny coverage is not actually saving you money.

Before committing to a policy, check how each company handles claims. Look at independent consumer ratings and see whether any company has an unusual pattern of complaints on file with the Texas Department of Insurance. Our look at the worst insurance companies in America is a useful starting point for understanding what to watch out for.

Other Tips for Purchasing Insurance

Evaluate Your Coverage Needs Beforehand

Before you start collecting quotes, think clearly about what level of protection your situation actually requires. A paid-off vehicle with a low market value may not justify the added cost of full collision and comprehensive coverage. On the other hand, if you have meaningful assets to protect, relying solely on the state minimum in liability could put everything you’ve built at serious financial risk. Consider your vehicle’s value, your daily commute, who else will be listed on the policy, and what you could realistically absorb out of pocket after a crash.

Shop Around

Rates for identical coverage can vary by hundreds of dollars a year between carriers, and insurers regularly reprice their books based on internal factors that have nothing to do with your behavior behind the wheel. Comparing quotes from multiple companies every one to two years is one of the simplest ways to make sure you’re not overpaying.

When you compare, make sure every quote is built on the same foundation: identical coverage types, matching limits, and the same deductible levels. A 30% lower premium that comes with half the liability coverage is not a better deal.

When an Accident Happens, We Can Help

Buying the right policy is about more than keeping monthly costs down. It is about making sure you are protected when something actually goes wrong. If you have been in a crash and are dealing with a claim, a coverage dispute, or an insurer that is not responding fairly, that is exactly what our firm is here for.

At Angel Reyes & Associates, we have more than 30 years of experience representing injured Texans and have recovered more than $1 billion for our clients. We offer free consultations, charge no fee unless we win, and are available 24/7. Reach out to us today if you have questions about a claim or need guidance on what your coverage should cover.

*Angel Reyes & Associates is not affiliated with any insurance company, including those both listed here and excluded from this list, and does not endorse or recommend any particular company over another. We always strongly recommend doing your own research and reaching out to companies for quotes tailored to your situation and your coverage needs.

All data presented in this piece is based on estimates/averages obtained at the time of writing, and is not intended to reflect or provide any realistic cost estimate for any particular company. All figures are speculative and purely for demonstrative, educational purposes only.

Past results do not guarantee future success.

Car Insurance Shopping FAQs

Does Texas auto insurance cover you if you drive into Mexico?

Usually not. Mexico does not recognize U.S. auto policies, so you usually need a separate Mexican liability policy before crossing the border.

Do any insurance companies force you to use their preferred repair shop?

No. Under Texas insurance rules, you have the right to choose the repair shop and the parts used on your vehicle, although the insurer only has to pay a reasonable amount for repairs and parts of like kind and quality.

What happens if your car is totaled and you still owe money on the loan?

A standard auto policy usually pays the car’s market value, not the remaining loan balance. If you owe more than the vehicle is worth, gap insurance or loan/lease coverage may help cover the difference.

How long does your own insurance company have to respond to a claim in Texas?

In Texas, your insurer generally has 15 business days to acknowledge your claim and 15 business days after receiving the information it needs to accept or deny it, with a limited extension if it explains why more time is needed. Once the claim is approved, payment is generally due within five business days.

Can you get your deductible back after a Texas crash that was not your fault?

Sometimes. If you use your own collision coverage, your insurer may try to recover what it paid from the at-fault driver’s insurer, and if that happens, you might get some or all of your deductible reimbursed.

About the Authors

Kyle Nicolas

Writer

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing content strategist, author and editor, with past work spanning numerous legal topics and practice area verticals.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...