How Does Your Auto Insurance Grade?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas ranks among the nation’s leaders for uninsured drivers, with an estimated 14.5 percent of motorists lacking coverage, making UM/UIM protection increasingly important.

- Texas only requires minimum liability coverage of $60,000 per accident, but the blog argues that amount can be exhausted quickly by vehicle damage and medical bills after a crash.

- Policies that combine higher liability limits with UM/UIM coverage and supplemental protections like PIP or MedPay are better prepared for a serious claim.

Our Interactive Tool Measures How Your Auto Policy Would Fare in a Wreck

If you’re involved in an accident, either with another car, a motorcycle, or even a commercial truck, the last thing you want is for your insurance to not adequately cover everything involved. You pay your monthly premiums for that peace of mind, but not all policies are created equal.

That same policy with the same limits you have been renewing for the last 10 years or more might not be robust enough to support you in the event of an accident. We believe nobody should take to the roads unprepared, so we have developed a way to help readers better understand their auto policy and how it stacks up to the true costs associated with an accident or incident in today’s driving world.

Evaluating Your Insurance Coverage

The first step in determining how your coverage grades is to evaluate what coverages you have. Not all policies are created equal, and this wide variance means two different drivers with identical records and driving the same car might face a completely different situation if they are involved in a wreck.

Here are a few key factors we look at.

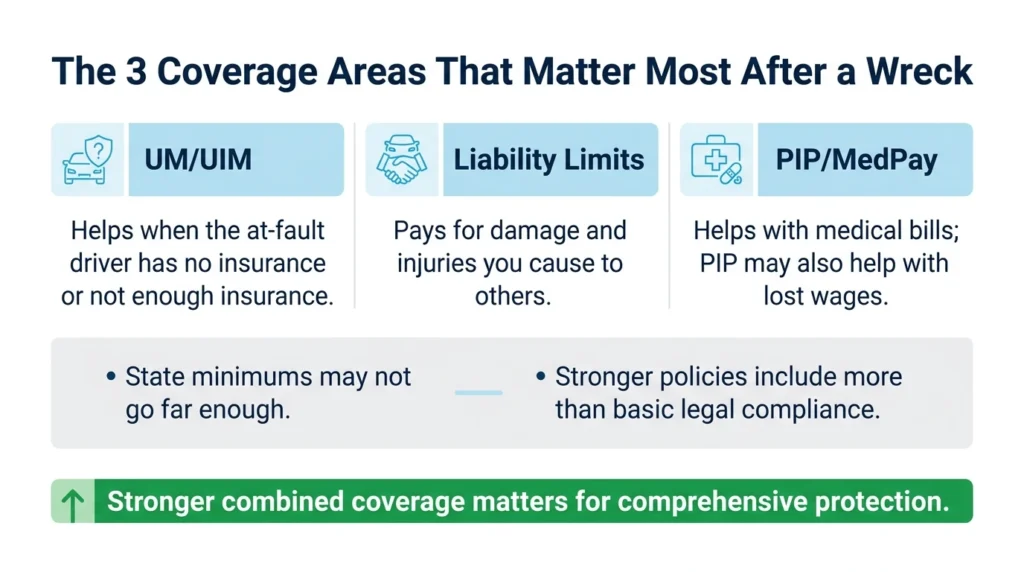

UM/UIM

Uninsured motorist (UM) or under-insured motorist (UIM) coverage is optional, but it is becoming increasingly necessary with every passing year. Texas frequently ranks among the nation’s leaders in terms of the number of uninsured drivers on the road, with the Insurance Information Institute ranking Texas 19th out of 50 in a study released in 2025.

By their estimate, 14.5% of all drivers don’t have insurance, meaning about one out of every seven drivers does not have any policy in place to protect themselves or those around them.

A UM/UIM policy provides this protection, adding additional coverage should the driver responsible for an incident either not have insurance at all or not have adequate insurance to fully cover the extent of the damage they cause.

Liability Limits

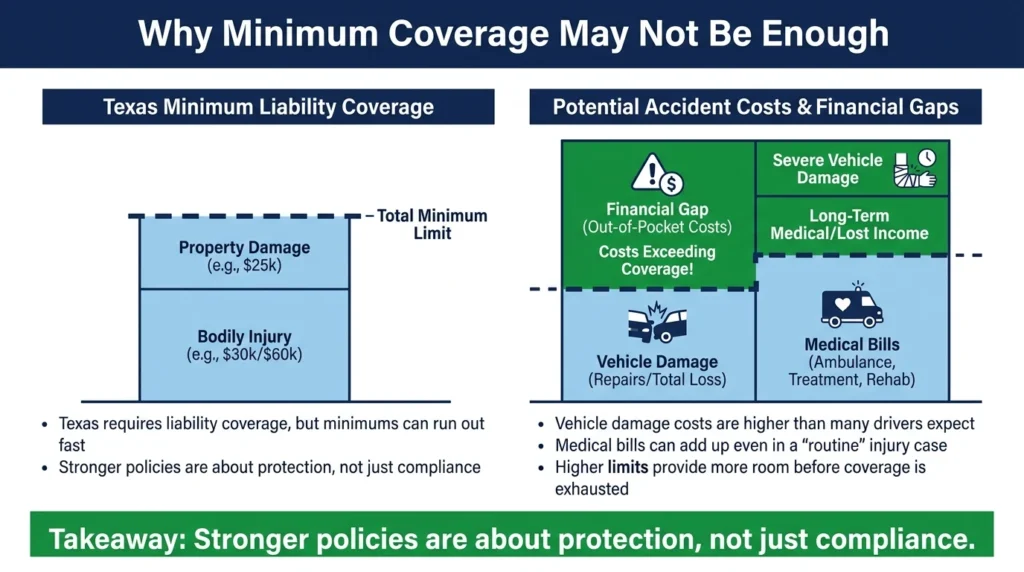

Liability insurance is the only type of coverage Texas law mandates that you have in order to legally operate a vehicle on public roads. The legal minimum of $60,000 per accident may sound like a lot, but the truth is that amount can disappear quickly.

$30,000 in damage isn’t all that hard to hit these days, especially when the average cost of a new car is now roughly in the range of $50,000—nearly double that amount. And that’s not even considering the cost of any medical bills, which can easily extend into the thousands or even tens of thousands for routine treatment for common accident-related injuries.

For this reason, policies with higher liability limits receive a much higher grade, as they are far better equipped to bear the full financial burden of an average wreck without completely exhausting all available funds.

Additional Options

Texas auto policies can also include supplemental products like personal injury protection (PIP) or MedPay coverage.

Texas law requires insurers to offer personal injury protection coverage on all policies they write, and it must be included by default. If you wish to decline this protection, you have to do so in writing.

However, this supplemental protection can help bridge the gap if you have any medical expenses while your claim is ongoing, and it can even be used to replace lost wages should you miss work due to your injuries. MedPay can also help cover your medical expenses, but it does not cover any lost wages.

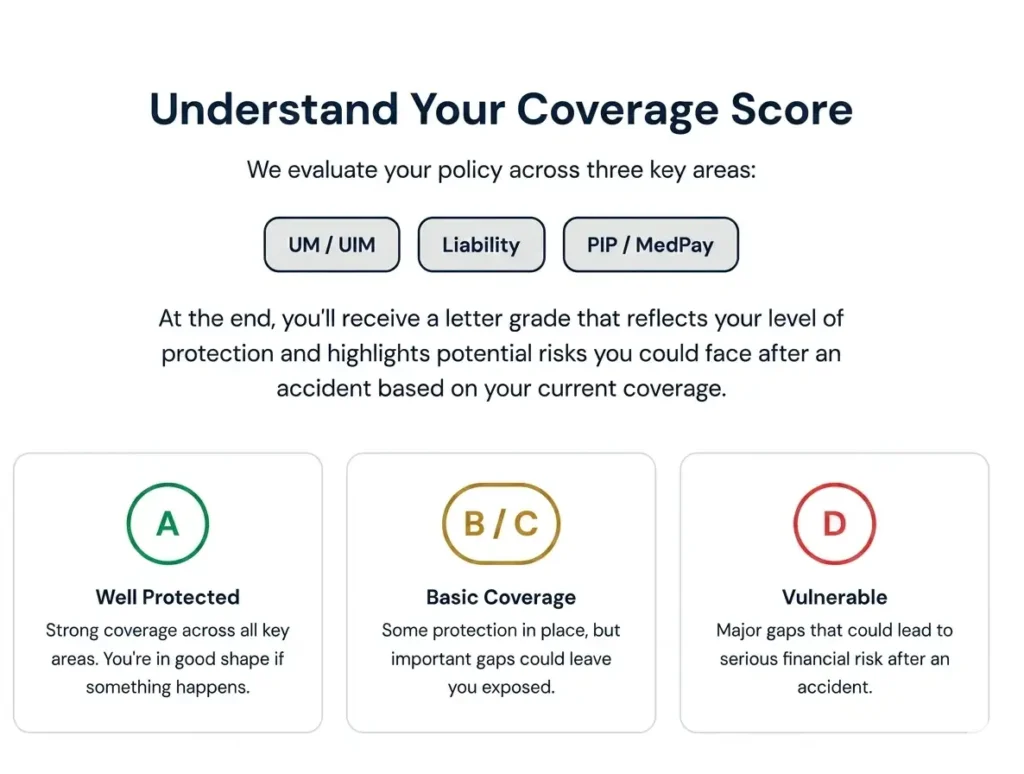

How We Grade Policies

Grade A: Your policy includes all three major injury-related coverages. Your liability coverage is also considerably higher than the state-mandated minimum.

Grade B: Your policy includes UM/UIM and elevated liability limits, but does not include any supplemental injury protection. This isn’t necessarily a bad thing—your own personal health insurance may cover your injuries. However, it’s never a bad idea to have additional protection should you be seriously hurt.

Grade C: Your policy is either missing UM/UIM coverage, or your liability protection is still the state minimum. With roughly one in seven Texas drivers being uninsured, not having UM/UIM on your policy could leave you vulnerable.

Grade D: Your current policy lacks more than one key protection. Should an accident occur, these policies are more likely to be depleted before all losses are fully covered.

What If My Policy Grades Poorly?

If you’ve tested your policy and the results aren’t where you would like them to be, it might be time to update your insurance and seek a new, better policy that is built to protect you in today’s driving environment.

If you’re worried about the cost of changing your policy, we can help. We have developed an auto policy premium estimating tool that uses real-world data to help you get a picture of what a policy you build might cost. Along with this tool is information on what can cause your premiums to increase, and some tips that might help you save some money on your monthly bills.

Need Legal Help? Call Angel Reyes & Associates

Even if you have a well-equipped policy, insurance companies don’t always play nice. If you have been in an accident and your insurer is either undervaluing your claim, has denied your claim outright, or is trying to shift blame onto you to reduce their payout, an attorney can help you protect your claim.

Angel Reyes & Associates has helped injured Texans recover damages for over 30 years. With a substantial record of success, our team is prepared to pursue all available options to help you recover damages, whether the insurer in question is another driver’s or your own.Request a free, no-obligation case evaluation today. Call us or use our online contact form for more information.

Insurance Grading FAQs

Why is liability coverage weighted so heavily?

Liability is the only type of insurance required by law, and it’s the type of insurance that kicks in to cover any damage or injuries you may be at fault for. If an incident involves two or three other vehicles, liability policy limits can be reached quickly.

If you don’t have enough to cover all losses in an accident, the other drivers could come after you and your assets personally, including your car, your home, and more.

Does this tool grade commercial insurance policies?

It isn’t expressly designed to, but the core principles hold true whether you’re looking for a personal car or a business-owned vehicle. Elevated liability limits are critical to protect your business, and it’s still important to carry protection from uninsured drivers, too.

Does my high-scoring policy cover a rental car or a borrowed car?

Usually, but not always. Texas consumer guidance says most policies cover accidents in rental cars, and when you crash a borrowed car, the owner’s insurance usually pays first before your coverage may apply.

Does my high-scoring policy cover anyone who drives my car?

No. Policies only cover drivers named in them, and a driver who gets in a wreck in your covered vehicle but who isn’t listed on your policy can create a huge problem. Insurance companies may outright deny a claim on a vehicle they cover if the wreck was caused by someone that the policy doesn’t list as an authorized driver.

Is PIP or MedPay insurance mandatory in Texas?

No. Texas law requires all insurance carriers to offer personal injury protection (PIP) coverage, and it must be included by default, but you can decline it. If you’re on a tight budget and you have your own health insurance protection, this could be a way to help you save money, but keep in mind your health insurance may have limits too.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...