What Is the Average Settlement for an Uber Accident in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Uber's $1 million primary policy applies once a ride is matched or a passenger is onboard.

- Texas bars recovery if you're found more than 50% at fault under CPRC Chapter 33 rules.

- You have two years from the crash date to file an Uber injury claim under CPRC § 16.003.

You were riding home from a late shift in Deep Ellum when your Uber driver got T-boned at a Commerce Street intersection. Now, your back hurts, you’re missing work, and the adjuster who called this morning gave you a number that feels low. How do you know if it’s fair?

The average settlement for an Uber accident can give you a starting point, but each case is different. A realistic range for your specific situation will depend on a number of factors.

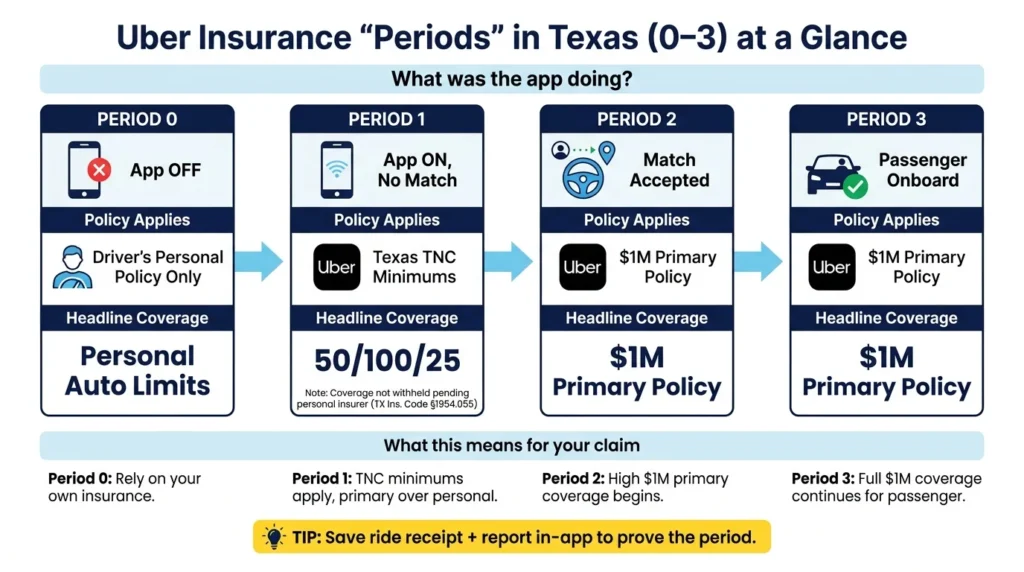

What Uber Insurance Periods Mean for Your Claim

Uber’s coverage works in four phases tied to the driver’s app status at the moment of the crash.

- Period 0 means the app was off, and only the driver’s personal policy applies.

- Period 1 means the app was on, but no ride was active, and in this case, minimum legal responsibility applies under Texas Insurance Code Chapter 1954.

- Period 2 (ride was accepted but no passenger was onboard yet).

- Period 3 (the passenger is in the vehicle) activate Uber’s $1 million primary policy.

Period 1 sets contingent minimums of $50,000 per person, $100,000 per incident, and $25,000 in property damage under § 1954.052. Uber’s Period 1 coverage does not depend on the driver’s personal insurer denying the claim first. Both policies may apply, and the TNC policy cannot be withheld while waiting for the driver’s insurance decision under Texas Insurance Code § 1954.055. In Period 1, uninsured and underinsured motorist coverage is limited, so it’s worth it to confirm the details early on.

Once a ride is matched (Period 2) or a passenger is onboard (Period 3), the $1 million aggregate primary policy kicks in. Most serious passenger injury claims apply here.

Period status is the most important factor in the amount you can recover, which is why early case review on a rideshare accident claim starts by confirming the app status at the time of impact.

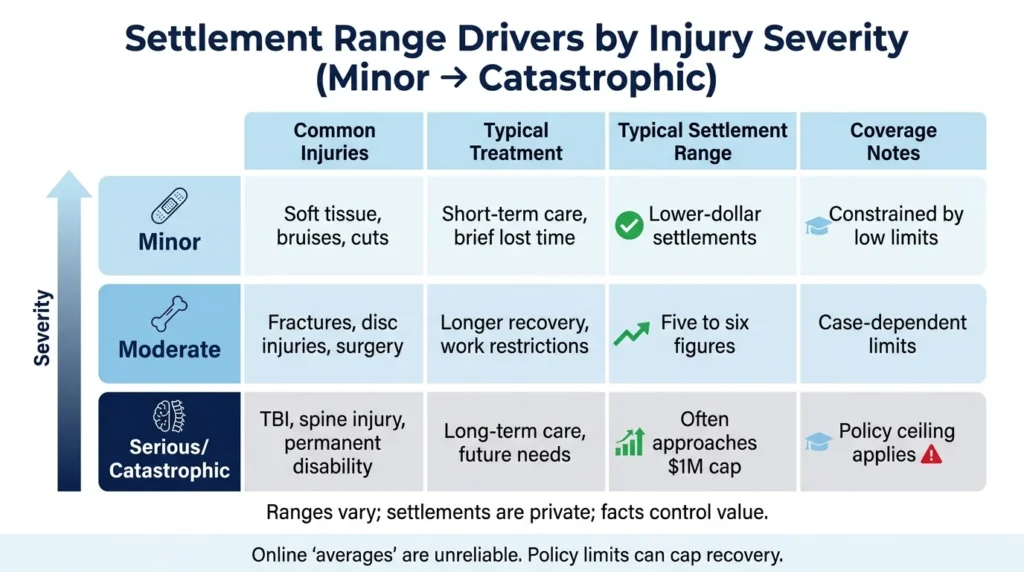

Settlement Ranges According to Injury Severity

The value of your settlement depends on the severity of your injuries, the cost of your treatment, and which insurance coverage applies. Minor injuries settle for lower amounts. Catastrophic injuries can approach the $1 million Period 2 or 3 ceiling. Published “averages” you see online are unreliable because settlements are private, and case facts vary widely.

Minor injuries (such as soft tissue injuries, bruising, and minor lacerations) usually involve short-term medical bills, brief lost wages, and modest pain and suffering. Period 0 and Period 1 claims may hit the policy limits before the full value of your injuries are calculated.

Moderate injuries (such as fractures, disc injuries, and surgical repairs) push medical costs higher and extend recovery timelines. These claims often land in five-figure or lower six-figure ranges, depending on the treatment duration and its documented impact on your daily life.

Serious and catastrophic injuries (such as traumatic brain injury, spinal cord damage, permanent disability, and wrongful death) usually reach close to Uber’s $1 million primary policy. These cases often include long-term care, structured settlement payouts, and lawsuits involving multiple parties.

Factors That Raise or Lower an Uber Settlement in Texas

Several variables can raise or lower the amount of your settlement. Some of these variables can be documented. Others will be intensely scrutinized by the opposing adjuster.

The severity of your injuries and the duration of your medical treatment will determine your settlement amount more than any other factor. Gaps in treatment or missing follow-up visits will give adjusters ammunition to argue that you weren’t really hurt in the crash.

Determining who caused the crash is also an important factor. Cases where it’s clear who’s at fault settle faster and for higher amounts. If fault is disputed, negotiations can drag on, and the amount of money you can recover will shrink.

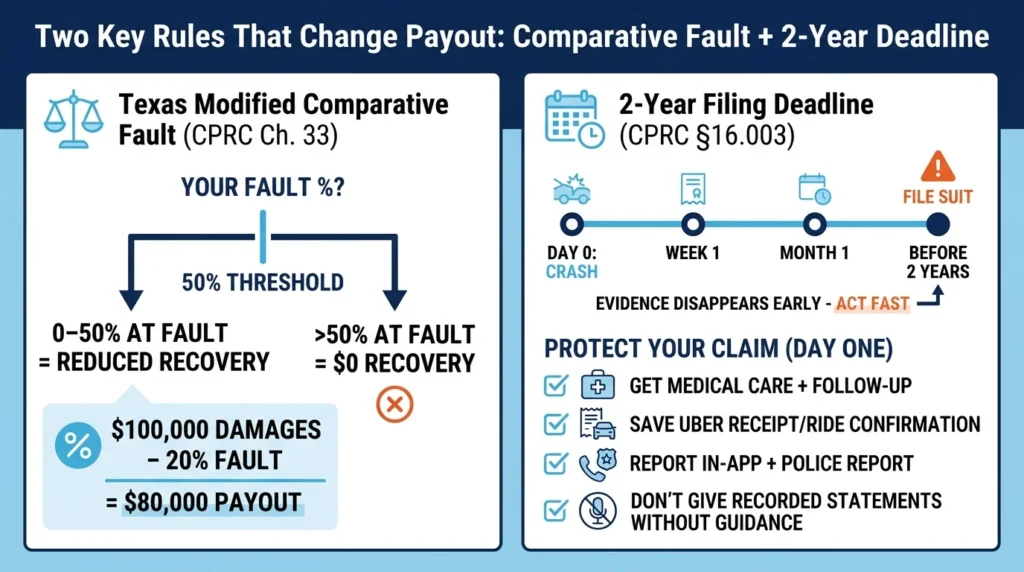

Texas uses modified comparative fault under Texas Civil Practice and Remedies Code Chapter 33. This means if you’re found more than 50% at fault, you recover nothing. If you’re found to be less than 50% at fault, then your recovery is reduced proportionally. This rule also applies to passengers in some scenarios, which is why it’s important to understand partial fault rules in Texas crashes before you accept any offer.

The amount of insurance available can limit how much money you can recover. For example, in a Period 1 crash with serious injuries, you may only recover the minimum insurance amount, no matter how well-documented your losses are. Documented economic losses (such as medical bills, paystubs, and future treatment estimates) hold up better than vague guesses.

You may also recover non-economic damages for pain and loss of enjoyment, but these damages are harder to measure. The severity of your injuries, the duration you are expected to suffer from them, and strong medical records will be the determining factors for non-economic damage recovery.

Filing Deadlines & Next Steps After an Uber Crash

Texas gives you two years from the date of the crash to file a personal injury lawsuit under CPRC § 16.003. If you miss that deadline, then it’s almost impossible to file your claim. Wrongful death claimants get their own two-year clock that starts at the date of death.

Two years sounds like a lot of time… until evidence starts disappearing. Here’s how to protect your claim from day one:

- Get medical care promptly and follow through on treatment.

- Save your Uber trip receipt and ride confirmation because they can help prove what stage of the ride the driver was in during the crash.

- Report the crash through the Uber app and to law enforcement, so there’s official documentation.

- Do not give a recorded statement to any insurer (including Uber’s carrier) without legal guidance. Early statements are routinely used to limit the value of your settlement later.

The two-year deadline applies equally to passengers, third-party drivers, pedestrians, and cyclists. If you’re still sorting out what happened, our guide on what to do after a Texas rideshare accident can walk you through the first steps to protect the value of your claim.

Talk to an Attorney About an Uber Accident in Texas

The value of an Uber settlement depends on which insurance period applied, how severe your injuries are, and how clearly fault can be distributed. None of those questions answer themselves, and adjusters are not on your side when they call.

Our injury attorneys at Angel Reyes & Associates have over 30 years of experience and have recovered more than $1 billion for clients. We work on contingency, so there’s no fee unless we win, and consultations are free. Contact us today to discuss your Uber crash and what your claim may be worth.

Past results do not guarantee future outcomes.

Uber Accident Settlement FAQs

Can I sue Uber directly if their driver caused my crash?

It depends. In most Texas cases, you’ll file a claim against Uber’s insurance policy, rather than suing Uber as an employer, because Uber classifies its drivers as “independent contractors.” However, certain facts about how much control Uber had over a driver could allow you to argue that Uber was directly responsible for the crash.

Does Uber's insurance cover a passenger's injuries if the driver was under the influence?

Yes. Uber’s primary policy does not automatically exclude DUI cases, so the $1 million coverage can still apply during Periods 2 and 3, even if the driver was impaired. The driver may face separate criminal charges, and the passenger may also have an uninsured or underinsured motorist claim through their own auto insurance policy if the driver does not have enough coverage.

Can a minor injured in a Texas Uber crash still file a claim after turning 18?

Yes. Texas pauses the time limit to file a lawsuit for minors, so the two-year clock generally does not start counting down until the injured person turns 18. A parent or guardian may also file a claim on the child’s behalf before that point.

What happens to my Uber accident claim if the driver had no personal auto insurance?

If the driver carried no personal policy, and the crash happened during Period 0, then you need to file a claim with your own uninsured motorist coverage (if you have it). During Periods 2 and 3, Uber’s primary policy applies, regardless of whether the driver carried personal insurance.

Does a settlement from Uber's insurer affect my ability to recover from a third-party driver who was also at fault?

No. Settling with Uber’s insurer does not automatically stop you from suing a third party who was also at fault. You may pursue both sources of recovery, but the settlement agreement language is important, as it could restrict further claims if it is written in vague terms.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...