How Insurance Coverage Works for Tesla Robotaxi Accidents in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas TNC insurance requirements under Insurance Code Chapter 1954 may apply to robotaxi rides, with coverage depending on trip status at the time of the crash.

- Preserving evidence early (trip details, timestamps, in-app reports) is critical because autonomous vehicle data may not be retained indefinitely.

- Multiple liability layers may exist in a robotaxi crash, including another driver, the robotaxi operator, and potentially technology-related claims.

You booked a Tesla Robotaxi for a quick trip across Austin. The ride started smoothly, but another vehicle ran a red light near the Mueller neighborhood and slammed into your door. Now you’re dealing with injuries, medical bills, and a confusing question: who exactly is responsible when there’s no human driver behind the wheel?

Autonomous ride services are expanding across Texas, and crashes are happening. Tesla disclosed multiple Robotaxi incidents to federal regulators since launching in Austin, drawing attention from the National Highway Traffic Safety Administration. For injured riders, the path forward involves understanding Texas insurance rules, preserving the right evidence, and knowing which “liability layers” may apply.

What Makes a Tesla Robotaxi Crash in Texas Different for Riders

A robotaxi crash can look like any other car accident. The difference is in who (or what) was controlling the vehicle and how that affects your claim.

When you’re injured as a passenger in a traditional rideshare, you typically look to the driver’s actions and the company’s insurance. In a robotaxi, though, there’s no human driver to point to.

Instead, you’re dealing with potential liability from multiple sources: another driver who caused the collision, the robotaxi company, the vehicle owner, and possibly the technology itself.

Think of it as “liability layers.” Each layer represents a party that might bear responsibility depending on what caused the crash. Texas is an at-fault state, meaning someone’s negligence must be established. Identifying that “someone” in an autonomous vehicle scenario requires careful investigation, though.

This liability is essential to establish for riders throughout Texas because of our state’s laws. Whether you’re visiting Dallas for business, commuting in Austin, or traveling through Houston, app-based “prearranged rides” trigger specific insurance requirements under state law.

Federal regulators have also increased scrutiny of autonomous vehicle operations, particularly around conditions like visibility and weather that often factor into crash investigations.

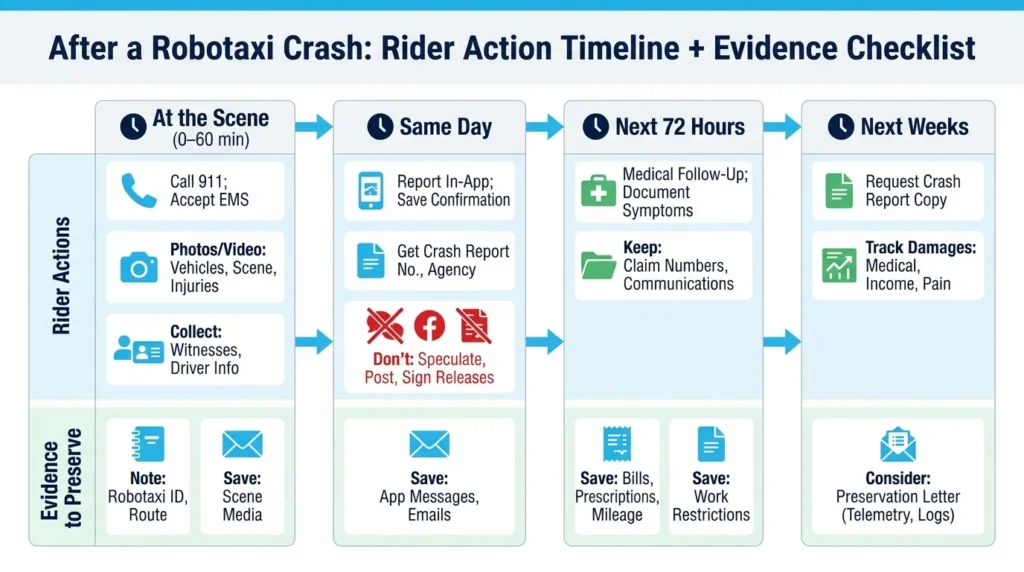

What to Do Immediately After a Robotaxi Crash

Your first priority is safety and medical care. Call 911 and accept an EMS evaluation, even if you feel fine initially. Adrenaline can mask pain, and some injuries (like soft tissue damage or concussions) don’t show symptoms for hours or even days.

Once you’re safe, report the crash through the app. Tesla’s Robotaxi support page outlines the incident workflow. Save every confirmation email and message you receive. This documentation proves the ride was active and creates a record of your report.

Capture evidence that riders often overlook:

- Trip details: pickup location, destination, timestamps, and the robotaxi’s identifier

- Photos and video: damage to all vehicles, the intersection or road, traffic signals, and your visible injuries

- Witness information: names and phone numbers of anyone who saw the crash

- Other vehicles: license plates and insurance information from any other drivers involved

Be sure to avoid common mistakes like speculating about fault when speaking to police or insurance adjusters. Don’t sign any releases or accept early settlement offers. Don’t post about your injuries or the crash on social media. Anything you say or post can be used to minimize your claim later.

If You’re Injured as a Passenger

As a passenger, you weren’t controlling the vehicle. Your claim will turn largely on documentation and prompt medical treatment.

Get the crash report number and the name of the responding agency. Ask when and how you can obtain a copy. This report becomes a key piece of evidence.

Document your symptoms and treatment from day one. Keep records of urgent care or ER visits, follow-up appointments, prescriptions, and any work restrictions your doctor imposes. Track every expense: medical bills, mileage to appointments, and time missed from work. This information directly affects the value of your claim.

For more guidance, see our article on car accident claims for passengers.

Who Can Be Held Liable in a Texas Robotaxi Accident

Texas uses a proportionate responsibility system. This means fault can be divided among multiple parties, and your recovery depends on how that fault is allocated. As a passenger, you’re typically not at fault, which simplifies your position.

The main liability sources include:

- Another driver: If a third party caused the crash (running a red light, failing to yield, distracted driving), their liability insurance is a primary target.

- The robotaxi company/owner: The entity operating the autonomous service may bear responsibility for the vehicle’s actions.

- Maintenance providers: If a mechanical failure contributed to the crash, whoever maintained the vehicle could share liability.

- Technology-related claims: In some cases, questions arise about the automated system’s performance.

Investigators typically examine road conditions, visibility, weather, construction zones, object detection, sudden braking, and whether another vehicle cut in front of the robotaxi. These factors help establish what went wrong and who bears responsibility.

“Who Is the Operator?” Under Texas Law

When an automated driving system is engaged, Texas law addresses this through Texas Transportation Code Chapter 545. The statute includes provisions treating the automated system as the “operator” for certain traffic rules when automation is active.

This affects how police reports and citations are written. It doesn’t automatically determine who pays for your injuries. That question turns on insurance contracts and fault evidence, not just the technical “operator” designation.

For riders, the practical takeaway is this: preserve your trip and app details. The status of the ride (whether automation was engaged, the exact route, timestamps) becomes important evidence when sorting out responsibility.

Insurance Coverage Layers for Robotaxi Rides in Texas

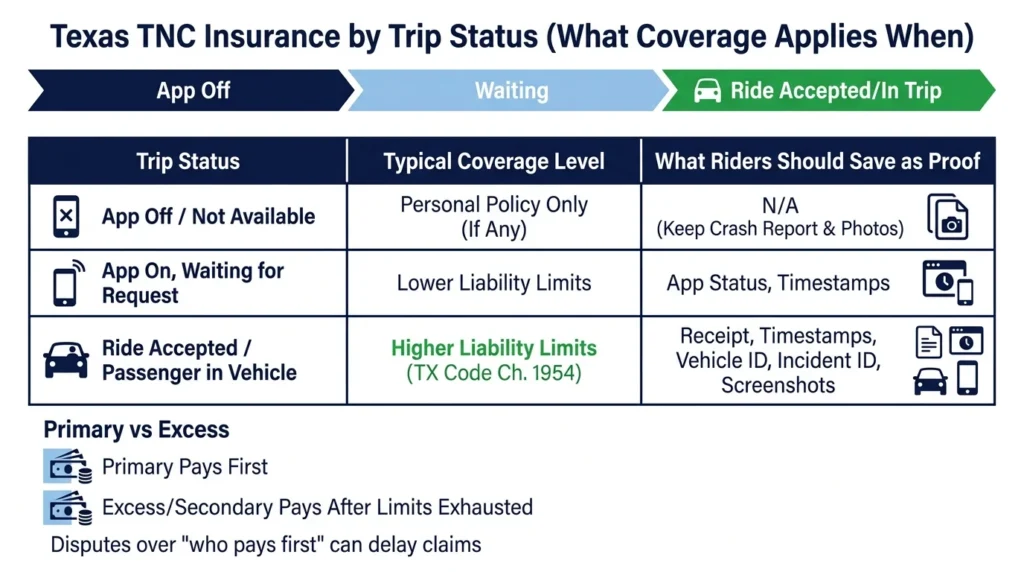

Many riders assume “the app covers everything.” Reality is more complicated. Texas rideshare and TNC (Transportation Network Company) insurance operates on a status-based system. Coverage changes depending on whether a ride is prearranged, in progress, or completed.

Texas Insurance Code Chapter 1954 establishes the framework for TNC insurance requirements. The coverage tiers work like this:

| Status | Coverage Level |

| App off / not available | Personal policy only (if any) |

| App on, waiting for ride request | Lower liability limits |

| Ride accepted / passenger in vehicle | Higher liability limits required |

For robotaxi passengers, the key period is when you’re in the vehicle during a prearranged ride. This typically triggers the highest coverage requirements. Proving the ride status requires documentation, though, which is why saving your trip details is so important.

Understanding “primary” versus “excess” coverage helps set expectations. Primary coverage pays first. Excess or secondary coverage kicks in only after primary limits are exhausted. When multiple policies apply, insurers often dispute who should pay first, which can delay your claim.

Coverage Sources That May Pay Your Injuries

Even when fault is unclear early on, multiple insurance policies may be available:

- The TNC/platform policy: Often the first place riders look during a prearranged trip. Your app status proof is critical to accessing this coverage.

- The at-fault driver’s liability insurance: If another vehicle caused or contributed to the crash, their policy may apply.

- Your own coverage: PIP (Personal Injury Protection), MedPay, UM/UIM (Uninsured/Underinsured Motorist), and health insurance can fill gaps or provide additional recovery.

Subrogation (where one insurer seeks reimbursement from another) can affect your final settlement. An attorney can help navigate these overlapping claims. Learn more about rideshare accidents and how coverage works.

Important Evidence in Robotaxi Claims

Autonomous vehicles generate valuable digital evidence: telemetry data, camera footage, software logs showing whether autonomy was engaged, and dispatch or remote support notes. This evidence isn’t automatically shared with injured riders.

Early preservation is crucial. Digital data can be overwritten or deleted if no one requests it be kept. A preservation letter (sometimes called a spoliation letter) formally asks the company to retain relevant evidence.

Rider actions that help your case:

- Screenshot your ride screen showing trip details, location, and timestamps

- Note any in-app incident ID or confirmation number

- Photograph the scene before vehicles are moved

- Get contact information for witnesses

When speaking to police, insurers, or the platform, stick to observable facts. Describe where you were seated, what you felt (impact direction, sudden braking), your injuries, and what happened afterward. Avoid speculating about software or hardware failures. Keep copies of every communication and claim number.

How a Texas Robotaxi Injury Claim Typically Unfolds

Understanding the process reduces anxiety. A typical timeline looks like this:

- Initial reports: You report to police, the app, and relevant insurers

- Medical treatment: You focus on recovery while documenting everything

- Investigation: Insurers and attorneys gather evidence, request records

- Liability decisions: Fault is allocated among responsible parties

- Settlement negotiations: Parties attempt to resolve the claim

- Litigation: If settlement fails, a lawsuit may be necessary

Common friction points include disputes over app status, arguments about which insurer is primary, delayed injury symptoms that complicate causation, and requests for recorded statements. For more on navigating these challenges, read our guide on what to do after a rideshare accident in Texas.

Damages for injured riders typically include medical bills (past and future), lost income, pain and suffering, and out-of-pocket expenses. The strength of your documentation directly affects what you can recover.

When to Talk to a Lawyer

Robotaxi cases involve layered insurance and technical evidence that can overwhelm injured riders handling claims alone. Early guidance prevents missed evidence and costly mistakes.

Consider contacting an attorney if you experience:

- Serious injuries requiring surgery or ongoing treatment

- Head, neck, or back symptoms

- Disputed fault among multiple parties

- Insurer delays, denials, or lowball offers

- Multiple vehicles involved in the crash

An attorney can coordinate claims across multiple insurers, request and preserve platform evidence, handle adjuster communications, and evaluate all available coverage layers. You can review our case results and client testimonials to see how we’ve helped others.

How Angel Reyes & Associates Can Help

Autonomous vehicle accidents raise questions that didn’t exist a few years ago. The technology is new, but Texas insurance and liability principles still apply. You need someone who understands both.

At Angel Reyes & Associates, we’ve spent over 30 years helping injured Texans navigate complex claims. We offer free consultations and work on contingency, meaning no fee unless we win. Our firm has recovered more than $1 billion for clients across Texas. We have more than 20 office locations statewide, offer service in Spanish, and are available 24/7.

If you’ve been hurt in a Tesla Robotaxi crash or any rideshare accident, contact us to discuss your options. We can help you understand the coverage layers, preserve critical evidence, and pursue the compensation you deserve.

Tesla Robotaxi Accident FAQs

Can you get a copy of the Texas crash report if you were just a passenger?

Yes. Passengers who were involved in the crash can usually request the Texas peace officer’s crash report, which can help with insurance claims and identifying the vehicles and insurers involved.

Will your health insurance pay after a robotaxi crash in Texas?

It may help cover treatment while liability claims are being sorted out, but your health plan may later seek reimbursement from a settlement depending on the policy and the facts. This is separate from auto-related coverage like PIP, MedPay, or UM/UIM.

What if the robotaxi crash happened in bad weather or low visibility?

Weather does not automatically excuse a crash, but it can become an important part of the investigation because safe operation may depend on visibility, road conditions, and how the vehicle or other drivers responded.

Do you have to give a recorded statement to the other insurance company after a robotaxi accident?

Usually, you are not required to give a recorded statement to an opposing insurer right away. It is often safer to provide basic facts first and avoid detailed speculation before you understand your injuries and the claim.

What happens if more than one vehicle caused the robotaxi crash?

Texas claims can involve fault shared by multiple parties, so more than one insurer may end up participating in the case. For a passenger, that can matter because recovery may come from several coverage sources rather than just one policy.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...