How Texas Insurance Companies Investigate Car Accidents

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Adjusters investigate fast and use reports, scene evidence, witness accounts, and medical records to assign fault and value your claim.

- Strong documentation, including photos, witness info, timely medical care, and saved bills/estimates, can reduce disputes and strengthen your case.

- Watch for red flags like rushed recorded-statement requests, unexplained delays, lowball offers, or blame without evidence, and seek legal help when needed.

How Texas Insurance Companies Investigate Car Accidents

You just filed a claim after a wreck on I-35, and an adjuster has just left you a voicemail saying they want your recorded statement by Friday. This is not an uncommon occurrence in the aftermath of filing a claim; Texas insurers typically begin investigating within 24 to 48 hours of receiving notice of a crash.

That quick timeline can feel overwhelming when you’re still dealing with a sore neck, and your car is still in the shop being evaluated. Knowing what adjusters look for and what you are and are not required to give them helps you protect your claim from the start.

What Insurance Adjusters Review After a Texas Crash

An adjuster’s job is to determine fault, valuate the damages and losses they are liable for, and calculate what the insurer owes. Texas follows a modified comparative fault rule. If you’re found more than 50 percent at fault, you recover nothing. Adjusters know this, so they scrutinize every detail that might shift blame toward you. To do this, they gather evidence, compare statements, and look for inconsistencies.

Here are a few of the things they review when making this analysis.

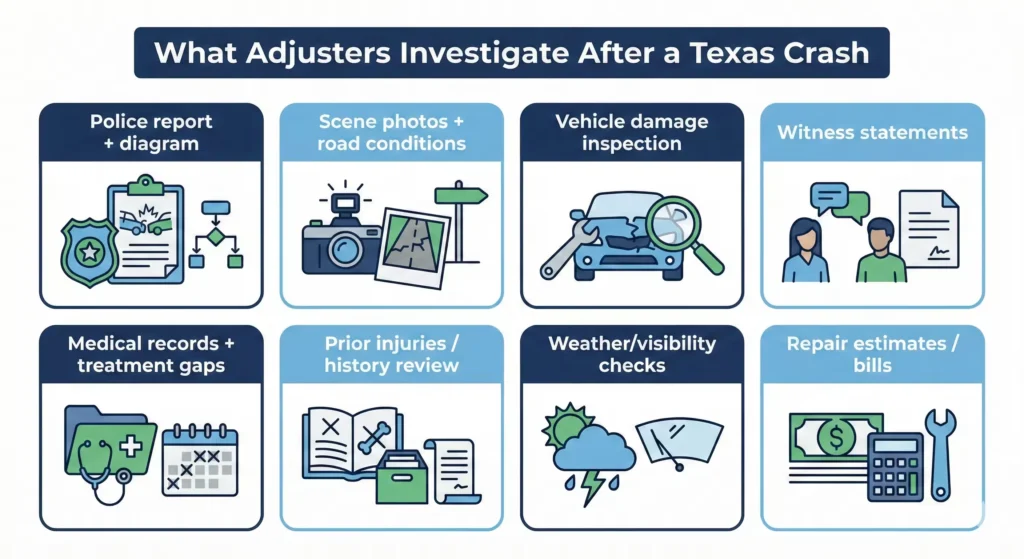

Police Reports

A crash report from DPS or a local law enforcement department gives adjusters an official account of what happened. It includes the officer’s diagram, witness names, and sometimes a preliminary fault assessment.

Texas law requires you to file a report if the crash caused injury, death, or property damage over $1,000. Even when not required, having a report strengthens your claim because it creates a third-party record. You can request your crash report through the Texas Department of Transportation’s online portal. Most reports become available within 10 business days of the incident.

Scene Documentation

Adjusters review photos of vehicle damage, skid marks, road conditions, and traffic signs in the area of the accident. They may send a field adjuster to inspect your car or visit the scene if liability is disputed. They will even evaluate the conditions on the day of the incident by checking weather records to see if either driver should have adjusted their speed.

Witness Statements

Adjusters will likely contact and collect statements from witnesses listed in the police report. They can also search for additional witnesses, including passengers, nearby business employees, or anyone who called 911. Inconsistent statements between your account and witnesses can hurt your claim; stick to the facts you remember clearly and avoid guessing.

Medical Records

Your medical records show the nature and severity of your injuries. Adjusters review ER visits, imaging results, follow-up appointments, and physical therapy notes, often looking for gaps in treatment. If you waited two weeks to see a doctor, the adjuster may argue your injuries weren’t serious or weren’t caused by the crash.

They also check for pre-existing conditions. Texas law allows recovery for aggravation of a prior injury, but adjusters sometimes use old records to minimize your claim.

How to Document Your Crash for a Stronger Claim

Strong documentation can greatly limit what an adjuster can dispute. If you’re involved in an accident, start collecting evidence at the scene if you’re physically able to do so.

At the scene:

- Take photos of all vehicles, including damage, license plates, and positions on the road.

- Photograph skid marks, debris, traffic signals, and weather conditions.

- Get contact information from witnesses.

- Exchange insurance and driver’s license information with the other driver.

- Call 911 if anyone is injured or if damage exceeds $1,000.

In the days after the incident:

- Request a copy of the police report.

- See a doctor within 24 to 72 hours, even if you feel fine. Some injuries take time to appear.

- Keep all medical receipts, bills, and appointment records.

- Save repair estimates and rental car receipts.

- Write down your own account of what happened while details are fresh.

For a complete checklist, see What Information to Collect After a Car Accident in Texas.

Red Flags During an Insurance Investigation

Most investigations proceed without major issues. But certain patterns may signal that an insurer is undervaluing your claim or acting in bad faith.

Pressure for a Quick Recorded Statement

Adjusters often ask for a recorded statement within days of the crash. You’re not legally required to give one to the other driver’s insurer. If you do give a statement, stick to basic facts. Avoid speculating about fault or the full extent of your injuries before you’ve finished treatment.

Unexplained Delays

Texas law requires insurers to acknowledge your claim within 15 days and make a decision within 45 days after receiving all requested information. Repeated requests for documents you’ve already sent, or silence for weeks at a time, may indicate stalling.

Texas has a two-year statute of limitations for personal injury claims. You have time to evaluate offers carefully.

Lowball Settlement Offers

An early offer that doesn’t cover your medical bills and lost wages is a red flag. Adjusters sometimes hope you’ll accept a settlement offer before you understand the full value of your claim.

Disputing Fault Without Clear Evidence

If an adjuster blames you for the crash but can’t point to specific evidence, ask for their reasoning in writing. You have the right to challenge their conclusions.

When to Talk to a Texas Car Accident Lawyer

You can handle a straightforward fender-bender claim on your own. But some situations benefit from legal guidance.

Consider consulting an attorney if:

- You suffered serious injuries or expect ongoing medical treatment.

- The adjuster disputes fault or offers far less than your documented losses.

- The insurer misses statutory deadlines or stops responding.

- Multiple vehicles or parties were involved.

- The other driver was uninsured or underinsured.

An attorney can review the adjuster’s evidence, gather additional documentation, and negotiate on your behalf. Most personal injury attorneys work on contingency, meaning no upfront fees. Our team at Angel Reyes & Associates has guided Texans through situations like this for over 30 years. Reach out to us for a free consultation and get help understanding your options.

Past results do not guarantee future outcomes.

Car Accident Investigation FAQs

Can I refuse to give a recorded statement to the other driver’s insurer?

Yes. You have no legal obligation to provide a recorded statement to the at-fault driver’s insurance company. You may still need to cooperate with your own insurer under your policy terms.

How long does a Texas insurance investigation usually take?

Timelines vary by case complexity. Simple claims may resolve in a few weeks. Disputed liability or serious injuries can extend investigations for months. Texas law requires insurers to decide within 45 days of receiving all requested documentation.

What if the police report contains errors?

You can submit a correction request to the law enforcement agency that filed the report. Attach supporting evidence such as photos, witness statements, or medical records. Adjusters consider corrections, but the original report remains part of the file.

Will my claim be denied if I was partially at fault?

Not necessarily. Texas allows recovery if you’re 50 percent or less at fault, but your compensation is reduced by your percentage of responsibility. If you’re found 51 percent or more at fault, you cannot recover damages from the other driver.

Should I accept the first settlement offer?

Evaluate whether the offer covers all your medical expenses, lost wages, and other documented losses. Early offers often undervalue claims, especially before treatment is complete. You can negotiate or reject an offer without losing your right to file a lawsuit within the two-year deadline.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...