Uber and Lyft Insurance Coverage Periods Explained

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas TNC coverage is split into four periods, and the period at impact controls which policy pays.

- Period 1 carries only $50K/$100K/$25K contingent limits, which creates the biggest rideshare coverage gap.

- Periods 2 and 3 trigger the TNC's $1 million primary liability policy under Insurance Code § 1954.053.

You were crossing Lamar Boulevard near downtown Austin when a driver with the Uber app open ran a stop sign and clipped your car. The driver tells the responding officer he hadn’t picked anyone up yet. Now, two insurers are blaming each other, and the offers on the table feel nowhere near what your medical bills will cost. Which policy actually pays?

What Are Rideshare Insurance Coverage Periods?

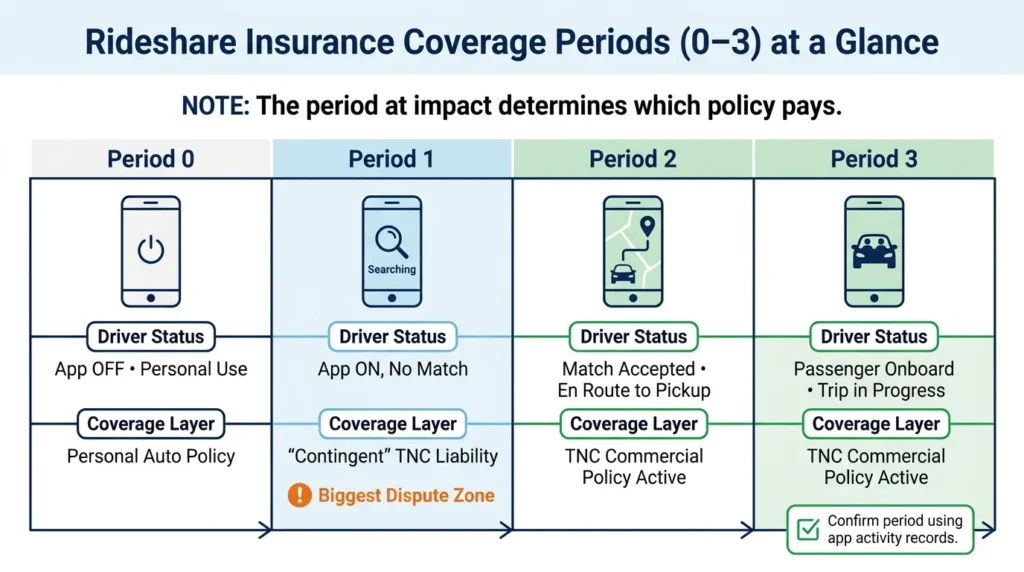

Rideshare insurance in Texas is split into four periods, based on what the driver is doing the moment a crash happens.

- Period 0 is when the app is off.

- Period 1 is when the app is on, but no ride has been accepted.

- Period 2 is en route to a pickup.

- Period 3 is an active trip with a passenger onboard.

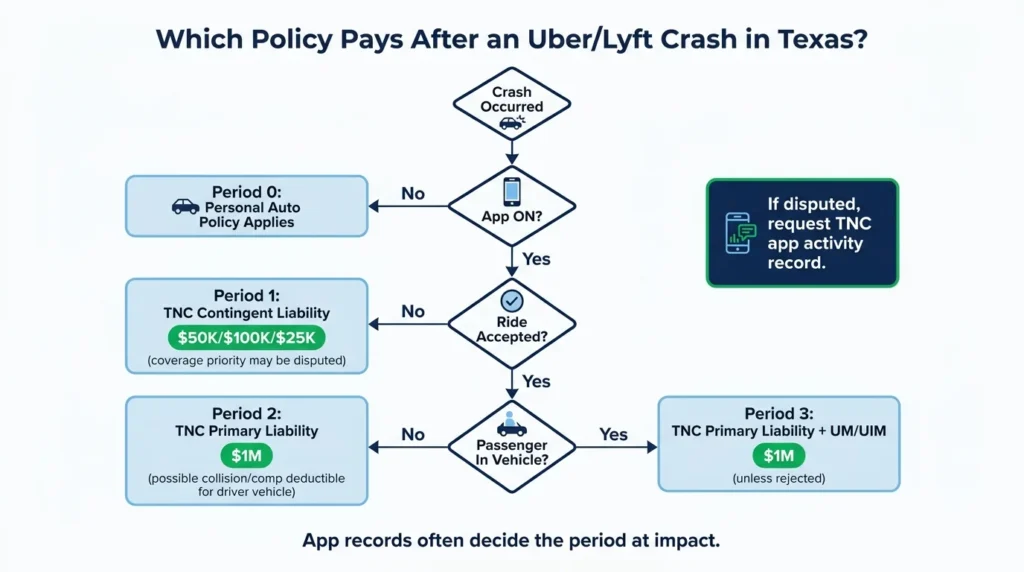

The period at the time of the impact decides which policy will cover the damages.

Uber and Lyft are regulated as transportation network companies (TNCs) under Texas Insurance Code Chapter 1954. Their coverage obligations for each period are set by the law, not by the companies. The same period rules apply to both platforms across Texas.

To confirm which period was active, you usually need the TNC app’s activity record. That record is often disputed, and the dispute can decide whether you recover $50,000 or $1 million.

Period 0 & Period 1 Coverage: The Coverage Gap

Period 0 and Period 1 are where most coverage fights happen. People often confuse them because both involve “no passenger,” but the policy rules are completely different, and getting the period wrong can seriously hurt your claim.

Period 0: App Off, Personal Policy Only

In Period 0, the driver is using the vehicle for personal reasons. The app is off. In this case, only the driver’s personal auto policy applies, and Uber and Lyft owe nothing.

There is no minimum TNC insurance requirement at this stage because the driver is not engaged in rideshare activity. In this situation, only the driver’s personal policy applies. If the at-fault driver wasn’t using the app at the time of the wreck, you can only file a claim against the driver’s personal insurer.

Period 1: App On, No Passenger Match Yet

Period 1 starts the moment the driver activates the app and becomes available for ride requests. Under Texas Insurance Code § 1954.052, the TNC must keep backup insurance (called “contingent liability coverage”) of $50,000 per person, $100,000 per accident, and $25,000 for property damage during this stage.

Under Texas Insurance Code § 1954.055, the TNC’s coverage does not have to wait for the driver’s personal insurer to deny the claim first, but in real life, TNC companies often treat their Period 1 policy as secondary coverage, which can lead to disputes over which policy pays first. These disputes are common and can delay payment.

Texas law allows personal auto insurers to exclude coverage from rideshare activity. A driver in Period 1 is considered to be working for a TNC, so that exclusion applies in this case. The result is a slow back-and-forth between two insurers before anyone writes a check. For a sense of how these claims resolve, see our blog on average settlement values in Texas Lyft accidents.

A lawyer who is familiar with TNC laws can request the app records and determine which policy layer is responsible for your claim, as outlined in this guide on steps to take after a Texas rideshare crash.

Periods 2 & 3: Full TNC Coverage Active

Once a driver accepts a ride, the rules change dramatically. The TNC’s full commercial insurance policy is active throughout the entire trip until its completion. Period 2 and Period 3 have the same minimum coverage amounts, but they differ in who counts as a covered victim and how physical damage is handled.

Period 2: Match Accepted, En Route to Pickup

Period 2 begins the second the driver accepts the request and is heading to the pickup spot. Under Texas Insurance Code § 1954.053, the TNC must provide primary liability coverage of at least $1,000,000 total per incident for death, bodily injury, and property damage, which covers the entire ride from acceptance through trip completion.

This is the TNC’s own commercial policy. It does not depend on the driver’s personal insurer. It pays first.

Collision and comprehensive coverage may also apply in Period 2 if the driver has these coverages. During Period 2, Lyft’s policy includes a $2,500 deductible for contingent collision and comprehensive coverage, which covers damages to the driver’s vehicle. However, it does not reduce the $1 million coverage limit available to third parties injured in the crash. Any pedestrians, cyclists, and other drivers who were hit during Period 2 can still claim up to the full $1 million policy.

Period 3: Passenger in the Vehicle

Period 3 covers the trip itself, from pickup through drop-off or cancellation. The $1 million TNC liability policy stays fully active during this period.

Passengers injured in Period 3 are covered under the same $1 million insurance limit. Uninsured and underinsured motorist (UM/UIM) coverage is also legally required during Periods 2 and 3, unless the insured person named on the policy officially refuses it in writing. This is important if the at-fault party is a third-party driver with no insurance of their own. Physical damage is handled the same way as in Period 2, but the deductible still applies.

How Texas Law Governs TNC Insurance Requirements

Chapter 1954 of the Insurance Code is the controlling statute for every TNC operating in Texas. It defines what a TNC is, sets the minimum coverage required for each period, allows personal auto insurance to exclude TNC use, and requires companies, drivers, and insurers to share information.

The Texas Department of Licensing and Regulation issues TNC permits and enforces their compliance. Both Uber and Lyft have TDLR permits and must follow the coverage rules set by Chapter 1954. Drivers must keep primary auto insurance while logged into the app and during rides.

Disclosure rules are more important than they seem. Texas law requires TNCs to make their policies available for inspection and tell drivers when company coverage applies and when personal coverage is the primary or backup (contingent) coverage. In a claim, these records can establish what the driver knew about how the coverage layers work.

If you help with a denied or underpaid rideshare claim, our attorneys can get the app record and match it to the right policy layer.

Work with a Texas Rideshare Injury Attorney

Figuring out which period applies, handling coverage layer disputes, and dealing with contingent denials are complicated, and insurers know it. Angel Reyes & Associates has over 30 years of experience handling rideshare accident claims. We work on contingency, meaning you pay no fee unless we win, and we have recovered more than $1 billion for clients.

Take a look at our recent case results, then contact us for a free case review so we can determine which coverage period was active, and which policy is responsible for paying you.

Past results do not guarantee future outcomes.

Rideshare Insurance Coverage Period FAQs

Can a rideshare driver's personal auto policy cover a crash during Period 1 if the TNC denies the claim?

Personal auto policies in Texas may exclude TNC activity under Insurance Code § 1954.151. If it is excluded, then the TNC’s contingent coverage typically applies. If both the driver’s personal insurer and the TNC argue over primary responsibility, then the injured person may face delayed payment while the two insurers sort out which policy layer applies first.

Does the $1 million TNC liability policy cover the rideshare driver's own injuries or only other people?

No. The $1 million commercial liability policy covers third-party claims, meaning injuries to passengers, pedestrians, other drivers, and cyclists. A rideshare driver who is injured in their own at-fault crash would need to look to their personal medical payments coverage or health insurance for their own injuries.

What is contingent collision coverage, and does it pay for a passenger's injuries?

Contingent collision coverage pays for physical damage to the driver’s vehicle when the driver’s personal policy also includes collision coverage. It does not pay for bodily injury to passengers or other people; those claims are covered by the TNC’s commercial policy.

Can UM/UIM coverage from a passenger's own auto policy stack on top of the TNC's $1 million limit after a Period 3 crash?

Yes, in some cases. If an uninsured or underinsured third-party driver causes the crash during Period 3, and the TNC’s UM/UIM coverage falls short, the passenger’s own personal UM/UIM policy may provide additional coverage, depending on the terms and limits of their policy.

How long do you have to file a personal injury lawsuit after a Texas rideshare crash?

Texas has a two-year statute of limitations for personal injury claims, meaning you generally must file a suit within two years of the crash date. Missing that deadline typically prohibits recovery, regardless of which coverage period was active at the time of the crash.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...