Who Pays Medical Bills After a Car Accident in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- In Texas, PIP coverage pays your accident medical bills first, regardless of who caused the crash.

- Health insurance covers accident injuries as secondary coverage after PIP benefits are exhausted.

- Letters of Protection and medical liens let uninsured patients get treatment and pay from settlement.

How Car Accident Medical Bills Get Paid in Texas

You are sitting in a Houston emergency room after a rear-end collision on I-10, watching a stack of paperwork grow next to you. The pain you are experiencing is one problem, and the bills you can already imagine arriving in the mail are another. You have insurance, but you are not sure whose coverage pays first, or what happens if it runs out.

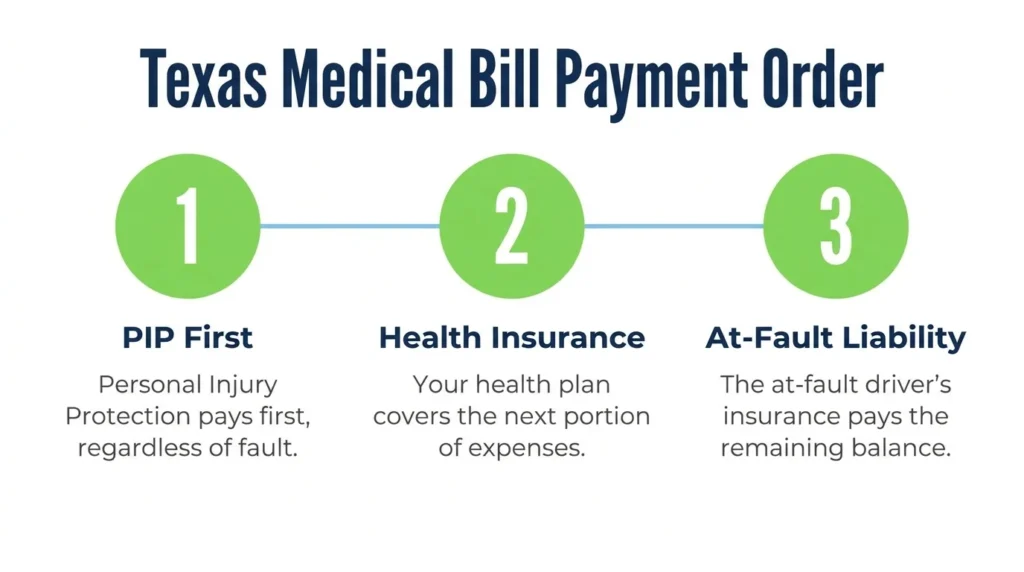

Texas Medical Bill Payment Sequence

In Texas, medical bills after a car accident follow a clear order: your own Personal Injury Protection (PIP) coverage pays first, your health insurance picks up next, and the at-fault driver’s liability insurance covers what remains at the end of your case. This sequence applies no matter who caused the crash.

PIP is a no-fault coverage required to be offered under Texas Insurance Code Chapter 1952. It pays your medical bills and a portion of lost wages quickly, without waiting for fault to be determined.

Once PIP benefits run out, your health insurance becomes the next payer. It treats accident injuries like any other covered medical care, subject to your deductible and co-pays.

The at-fault driver’s liability insurance, governed by Texas Transportation Code Chapter 601, comes into play at settlement. That payment reimburses what you and your other insurers have already covered, plus any remaining damages.

Personal Injury Protection Requirements

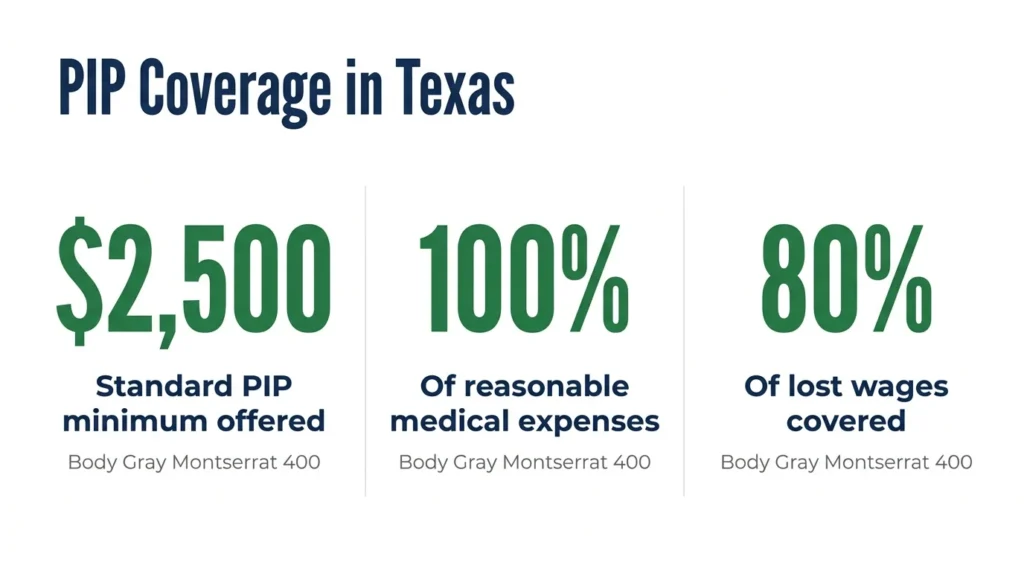

Texas insurers must offer PIP coverage on every auto policy, and you must reject it in writing if you don’t want it. Most drivers carry at least the standard $2,500 in PIP, though higher limits are available.

PIP typically pays 100% of reasonable medical expenses up to your policy limit, usually with no deductible. It also covers 80% of lost wages and certain replacement services if you cannot perform household tasks while recovering. The Texas Department of Insurance provides official guidance on these benefits.

If you are unsure what coverage you carry, check your declarations page or call your agent. Many drivers carry PIP without realizing it. The more you know about Texas minimum car insurance requirements, the easier it is to understand where PIP fits in.

Filing a PIP claim is straightforward. Notify your own insurer after the crash, submit medical bills as they arrive, and the insurer pays the provider directly or reimburses you.

Options for Uninsured Patients

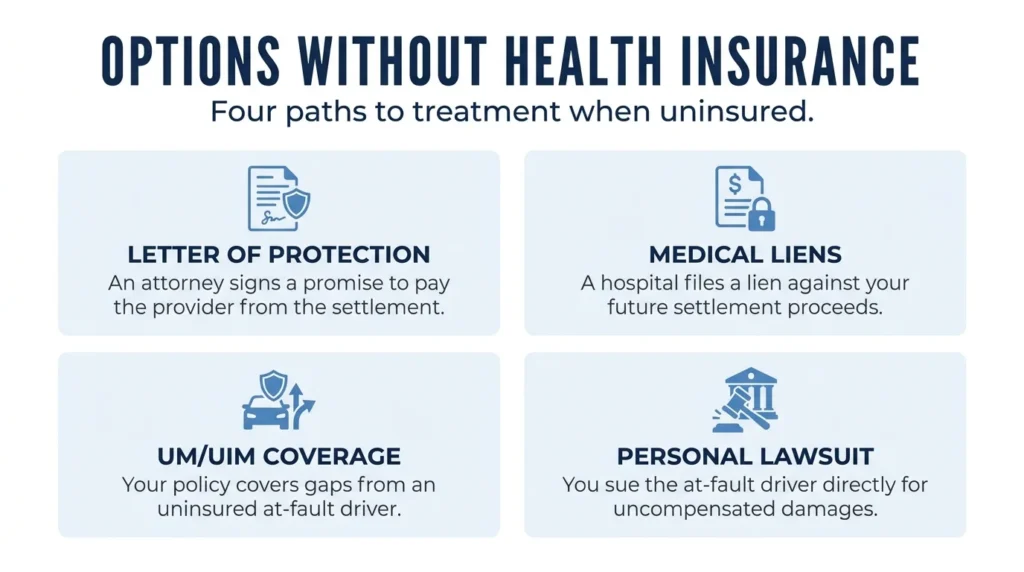

If you have no health insurance and limited PIP, you still have options for getting treatment. The two most common are Letters of Protection and medical liens, both of which let you receive care now and pay from your settlement later.

A Letter of Protection is an agreement signed by your attorney that promises payment to the provider from your eventual settlement. The provider agrees to treat you without billing you upfront. This arrangement is common with orthopedic specialists, pain management clinics, and physical therapists who regularly work with injury cases.

Medical liens work similarly but are governed by Texas Property Code Chapter 55. A hospital that treats you after a crash can file a lien against your future settlement, securing its right to be paid before the money reaches you. Liens have strict notice and timing rules that providers must follow.

Working with an attorney early helps coordinate these arrangements.

Our car accident team regularly helps clients line up treatment with providers who accept Letters of Protection.

When the At-Fault Driver Cannot Pay

If the at-fault driver has no insurance or carries only the state minimum, your own policy may step in through uninsured or underinsured motorist (UM/UIM) coverage. UM/UIM is required to be offered in Texas, and many drivers carry it. UM/UIM pays for your medical bills, lost wages, and pain and suffering up to your policy limit when the other driver cannot.

You can also pursue the at-fault driver directly through a personal injury lawsuit. Obtaining compensation from a driver with no assets, aka resources with economic value, is often difficult, but a judgment can sometimes be enforced against wages or property.

Medical providers in these situations often agree to wait for the case to resolve. They may reduce the final bill in exchange for prompt payment from the settlement. An experienced attorney negotiates these reductions on your behalf, which can leave more money in your pocket at the end.

Get Help with Car Accident-Related Bills

Angel Reyes & Associates has helped Texas car accident victims navigate medical bill payment issues for years. We work on a contingency fee basis, meaning no fee unless we win your case. Our team understands the Texas insurance system and can help you get the medical treatment you need while protecting you from overwhelming medical debt. Learn more about our firm or contact us today for a free consultation about your case.

Car Accident Medical Bill FAQs

How long do I have to file a PIP claim after a car accident in Texas?

Most Texas insurers require PIP claims to be filed within 30 days of the accident, though some policies allow up to one year. Check your policy or contact your insurer immediately after the crash to avoid missing deadlines.

What happens if my medical bills exceed all available insurance coverage?

You may be able to negotiate payment plans with providers, seek charity care programs at hospitals, or pursue additional compensation through a personal injury lawsuit. Many medical providers will also reduce bills in exchange for prompt settlement payment.

Can medical providers refuse to treat me if I only have PIP coverage?

Emergency rooms cannot refuse treatment, but specialists may require proof of payment ability before scheduling non-emergency procedures. Letters of Protection from an attorney can help secure treatment when providers are concerned about payment.

Do I need to pay my health insurance deductible for car accident injuries?

Yes, if your health insurance becomes the payer after PIP is exhausted, normal deductibles and co-pays apply. However, your health insurer may seek reimbursement from the at-fault driver’s insurance at settlement.

What if the other driver's insurance company contacts me about paying my medical bills directly?

You can accept direct payment, but be cautious about signing releases or settlements before understanding the full extent of your injuries. Consider consulting an attorney before agreeing to any payment arrangements with the other driver’s insurer.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...