Why Insurance Companies Delay Settlements in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurers face strict claim-response deadlines, but they can use delays to pressure you into accepting a low settlement.

- Repeated document requests, silence from adjusters, lowball offers, and recorded-statement pressure can signal intentional stalling.

- Protect yourself by documenting everything, demanding written explanations, avoiding broad releases, and speaking with an attorney before settling.

Why Insurance Companies Delay Settlements in Texas

You just got off the phone with the adjuster for the third time this month and the end seems to be nowhere in sight. Your medical bills are still piling up on the kitchen counter, and funds are getting tight as the process drains your savings. While insurance claims are not typically quick affairs, extensive delays may be the insurance company attempting to pressure you into accepting a lesser settlement.

Texas law gives insurers specific deadlines to respond to claims, but many use legal gray areas to stretch timelines. Your time matters. So does your recovery. Understanding why delays happen puts you in a stronger position to push back.

How Insurers Use Delays as a Strategy

Insurance companies are businesses: every dollar they hold onto longer earns interest, and every claimant who gives up or accepts a lowball offer saves them money.

Adjusters know that injured Texans face real pressure. Rent comes due, car payments don’t pause, and medical providers send collection notices. Delay tactics exploit this pressure. The longer they wait to present their settlement offer, the more likely you are to settle for less than your claim is worth.

While sometimes mistakes happen or circumstances dictate needing an adjustment, repeating patterns suggests underhanded tactics. If you’ve been in a wreck and your claim is dragging, you’re likely experiencing one of these tactics right now.

Texas Deadlines Insurers Must Follow

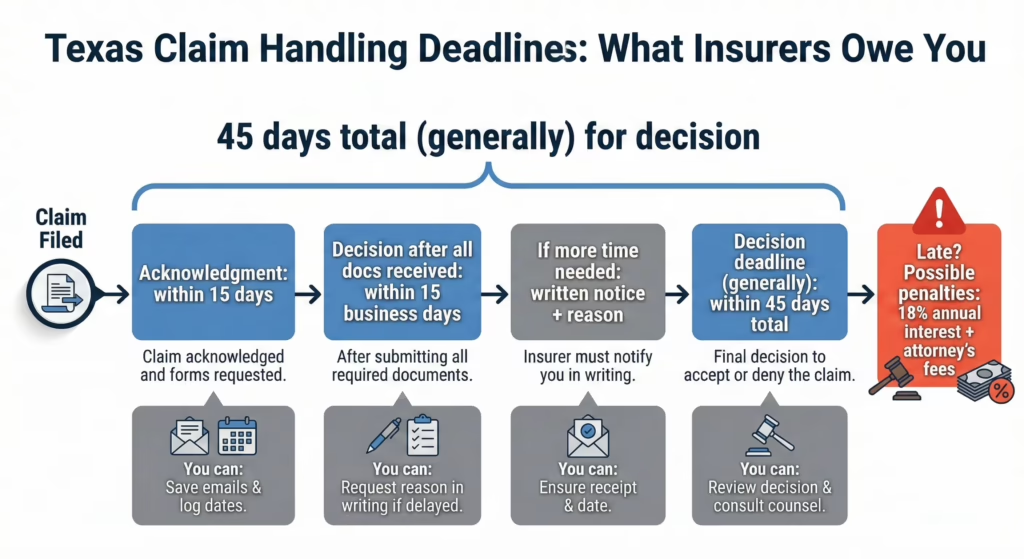

Under the Texas Prompt Payment of Claims Act, insurers must acknowledge your claim within 15 days and accept or deny it within 15 business days after receiving all required documentation (Texas Insurance Code Chapter 542).

If they need more time, they must notify you in writing and explain why. Even then, they generally have 45 days total to make a decision.

When insurers miss these deadlines without a valid reason, they may owe you interest (at the rate of 18 percent annually) plus reasonable attorney’s fees in addition to the original settlement amount. These penalties exist because the Texas Legislature recognized that delay harms claimants.

However, insurers often wager that most people won’t know their rights or won’t push back. The penalties are steep, so it’s within your best interest to speak to an attorney as soon as possible if your insurer misses their deadline to make a decision.

Signs Your Claim Is Being Stalled on Purpose

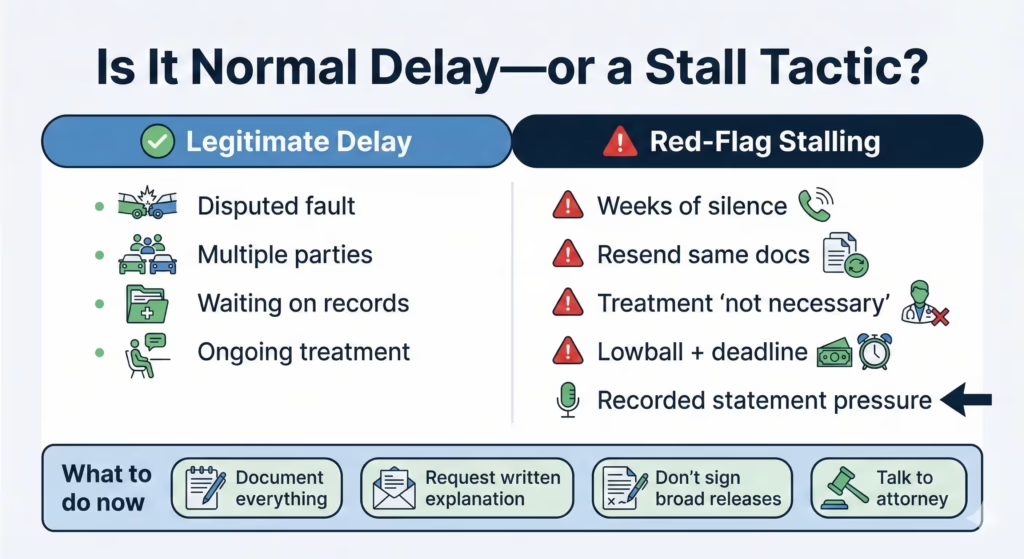

Not every delay is bad faith. Some claims involve genuine disputes over fault or injury severity, and these disputes take time to resolve.

But certain patterns suggest intentional stalling:

- The adjuster stops returning calls or emails for weeks

- You’re asked to provide documents you’ve already sent

- The insurer disputes treatment your doctor recommended

- You receive a lowball offer with a short deadline to accept

- The adjuster pressures you to give a recorded statement before you’ve finished treatment

If you’re juggling work, medical appointments, and family responsibilities, these tactics hit harder. That’s the point—the adjuster wants you to feel pressured to take their offer and wrap up your case.

However, you don’t have to settle for their tactics. Document every interaction, save emails, and note the date, time, and name of every person you speak with. This record matters if you need to prove bad faith later.

When Delay Becomes Bad Faith

Texas recognizes “bad faith” actions against insurers who unreasonably deny or delay valid claims. Bad faith isn’t just slow service; it’s a pattern of conduct that violates the duty insurers owe to claimants, such as:

- Ignoring evidence that supports your claim

- Misrepresenting policy terms to deny coverage

- Failing to conduct a reasonable investigation

- Offering far less than the claim is clearly worth

If you can prove bad faith, you may recover damages beyond your original claim, including attorney’s fees and, in some cases, additional penalties. However, this is generally difficult to do on your own. We recommend speaking with an attorney if you suspect your claim is being mishandled.

What You Can Do Right Now

You don’t have to wait for the insurer to act. Taking steps now protects your claim and your options.

- Keep copies of everything. Medical records, bills, repair estimates, photos of damage, and correspondence with the insurer.

- Request written explanations. If your claim is denied or delayed, ask for the specific reason in writing. Texas law requires insurers to explain denials.

- Don’t sign broad releases. Some insurers ask you to sign documents that give them access to your entire medical history or release them from future claims. Read carefully before signing anything.

- Avoid recorded statements without guidance. Adjusters may use your words against you later. You’re not required to give a recorded statement to the other driver’s insurer.

- Talk to an attorney before accepting any offer. Once you settle, you can’t go back. An experienced attorney can tell you whether the offer reflects the full value of your claim.

You generally have two years from the date of the wrongful conduct to file a bad faith claim in Texas. Missing that deadline can eliminate your options entirely.

Our experienced attorneys at Angel Reyes & Associates have guided Texans through situations like this for over 30 years. If your claim is stalled and you’re not sure what to do next, call us for a free consultation to help you understand your options. Every case is different; past results do not guarantee future outcomes.

Insurance Bad Faith FAQs

Can I sue my own insurance company for delaying my claim?

Yes, if your own insurer unreasonably delays or denies a valid claim, you may have a bad faith claim against them. Texas law allows policyholders to pursue damages when insurers violate their duties. You’ll need to document the delay and, in most cases, provide notice before filing suit.

What should I do if the adjuster won’t return my calls?

Send a written request by email or certified mail asking for a status update and response by a specific date. Keep a copy. If the insurer continues to ignore you, this documentation supports a potential bad faith claim and shows you acted reasonably.

Does hiring an attorney speed up my settlement?

It can. Insurers often take represented claimants more seriously because they know an attorney will hold them accountable for deadlines and tactics. An attorney can also handle communication so you can focus on recovery.

What if the insurer says my treatment wasn’t necessary?

Insurers sometimes dispute medical treatment to reduce what they pay. Your doctor’s records and opinions matter. If the insurer is second-guessing your care, gather your medical documentation and consider getting a second opinion. An attorney can help you respond to these disputes effectively.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...