Does UM/UIM Coverage Apply When You Are Riding in a Friend’s Car?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Passengers are covered under the vehicle owner's UM/UIM policy as long as the policy is in force and you were in the vehicle at the time of the crash.

- If the vehicle owner has no UM/UIM coverage, your own auto policy may extend protection to you as a passenger in someone else's car.

- You generally cannot collect from two policies simultaneously for the same damages, but sequential inter-policy recovery may be permitted.

The crash wasn’t your fault. You were a passenger in a coworker’s car moving south on I-35 through Austin when an uninsured driver ran a red light and hit the driver’s side. Now you are sitting in an emergency room with a bill in your lap, and no one can tell you whose insurance is supposed to pay.

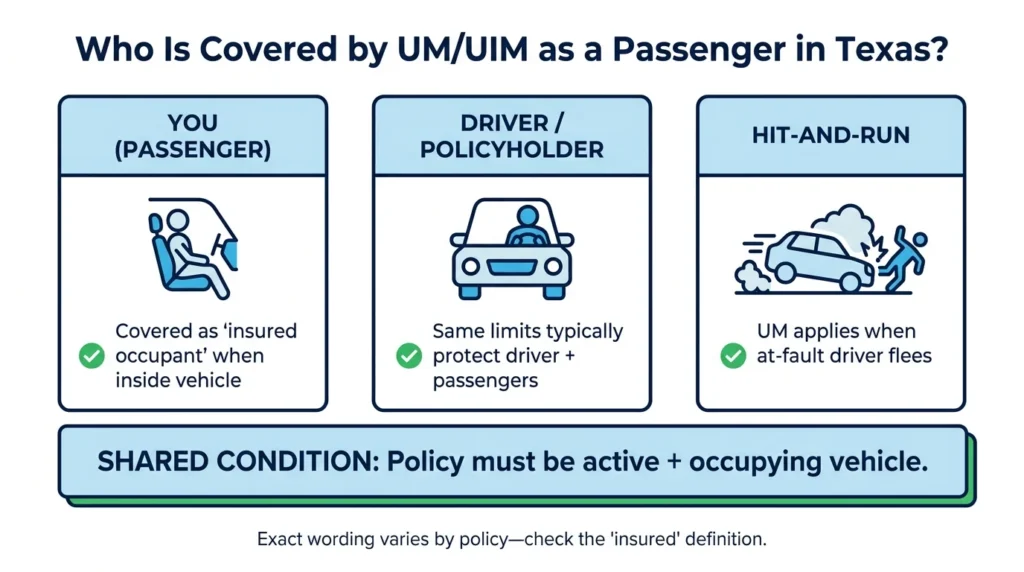

Does UM/UIM Coverage Protect Passengers?

Passengers are covered under the vehicle owner’s uninsured/underinsured motorist policy as long as the policy is in force and you were in the vehicle at the time of the wreck. You do not need to be the policyholder to file a UM/UIM claim. Texas Insurance Code Chapter 1952 requires insurers to offer UM/UIM coverage on every auto policy it issues, and that protection covers the driver and passengers.

The coverage rule is simple: If you were inside the vehicle when the collision happened, you are an insured occupant under the policy. Most standard Texas auto policies define “insured” as any person occupying the covered vehicle. The same UM/UIM limits that protect your colleague who was driving also protect you.

Between 14% and 20% of Texas drivers do not have liability insurance. That statistic makes UM/UIM coverage one of the most practically important parts of any auto policy. If your friend carries UM/UIM, you may already be protected simply by getting into the car. Uninsured motorist coverage also applies when the at-fault driver flees the scene without stopping.

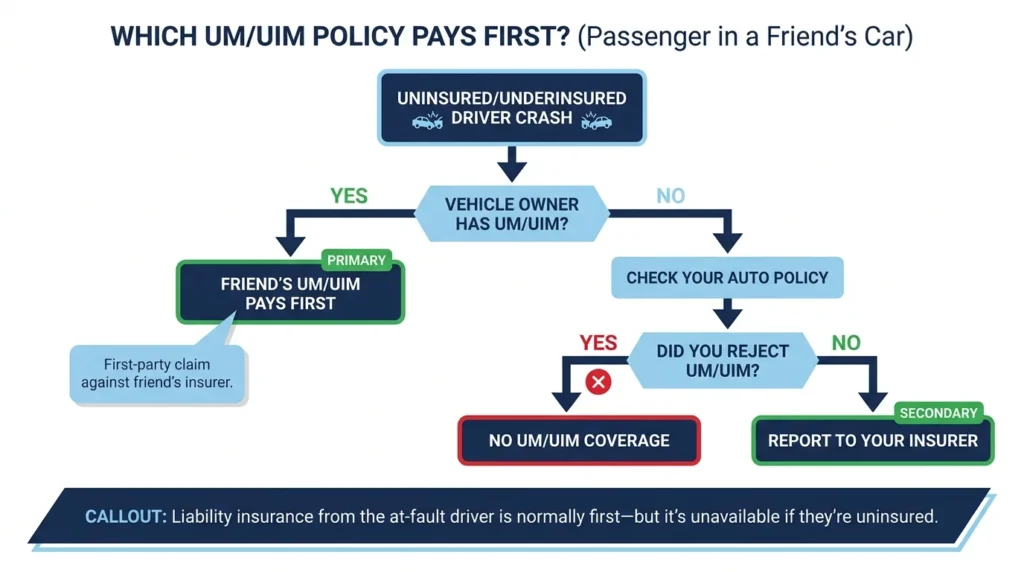

Which Policy Covers You First?

When an uninsured driver hits the vehicle you are riding in, the vehicle owner’s UM/UIM policy is the first to come into play. The insurer treats you as an insured occupant. You file your injury claim through the car owner’s policy as long as they carry UM/UIM coverage.

The at-fault driver’s liability coverage is normally the starting point after a crash. If the driver doesn’t have any insurance, your liability claim goes nowhere until UM/UIM coverage fills the gap. The vehicle owner’s insurer will step in and pay your claim up to the policy’s UM/UIM limit.

The process resembles a standard insurance claim in some ways, but you are actually making a first-party claim against your friend’s insurer. That distinction affects the applicable statute of limitations and the insurer’s obligations toward you under Texas law.

For a more in-depth outline of your rights and options as an injured passenger, see car accident claims for passengers in Texas.

When Your Own UM/UIM Policy Steps In

If the vehicle owner has no UM/UIM coverage, your auto policy may protect you, as Texas UM/UIM coverage follows the policyholder, not the vehicle. So if you have UM/UIM, that coverage may extend to injuries you sustain as a passenger in someone else’s car.

There is a key condition: Your UM/UIM coverage must be active on your policy. Some drivers decline UM/UIM in writing when buying coverage to lower their premiums. If your friend rejected UM/UIM on their policy and you also opted out of it on yours, neither source is available to pay your claim.

If your friend declined UM/UIM, but you carry it on your own policy, report the accident to your insurer and provide the facts. Your carrier will determine whether your policy covers you as an occupant of a non-owned vehicle. Many standard policies include this protection, though the exact language varies.

If you aren’t sure whether your policy extends to other vehicles, check your insurance declarations page for “non-owned vehicle” occupancy language. The answer is in your policy contract. For a detailed explanation of coverage options see our uninsured motorist guide.

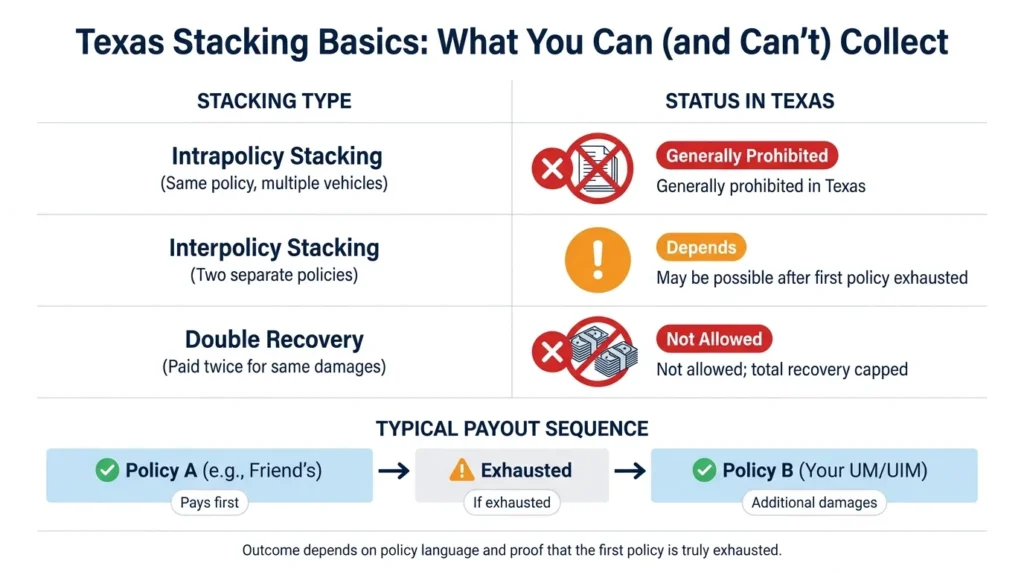

Texas Stacking Rules & Double-Recovery Limits

Accessing UM/UIM benefits from two separate policies after an automobile crash is called stacking, a practice that Texas limits. There are two types.

- Intrapolicy stacking, combining coverage limits for two vehicles listed on one policy, is generally prohibited.

- Interpolicy stacking, combining coverage from separate policies held by different people, may be possible when one policy is fully exhausted.

The typical sequence works like this. The vehicle owner’s UM/UIM policy pays first, up to its limit. If that limit does not cover all your costs, including medical bills and lost wages from missing time at a job, you may seek additional compensation from your own UM/UIM policy.

Texas courts have generally permitted this approach when the first policy is genuinely exhausted and the second policy covers you as an occupant of a vehicle you don’t own.

What you cannot do is collect from both policies simultaneously for the same damages. Most Texas policies include anti-stacking language that caps total recovery at the single-vehicle limit. Courts have upheld these clauses in most cases.

The line between acceptable interpolicy recovery and prohibited stacking depends on your specific policy language. If you attempt to navigate the rules without legal guidance, you run the risks of not recovering the full amount you are entitled to and making procedural errors that could damage your claim.

To learn the roles that UM/UIM coverage, PIP, and MedPay have after an accident, see PIP vs MedPay vs UM/UIM in Texas: A Practical Guide.

Talk to a Texas Injury Attorney

If you’ve been injured in a car crash caused by an uninsured driver, your recovery depends on identifying every available coverage source before any deadline passes. Angel Reyes & Associates has helped injured Texans work through UM/UIM claims for over 30 years. With our fully remote process and more than 20 office locations across the state, we can handle cases in any court or any district.

Initial consultations are free, and you pay nothing unless we win your case. Contact us today to get started.

UM/UIM Coverage FAQs

Does UM/UIM coverage apply to me as a passenger if I don't own a car?

If you don’t own a vehicle and hold no auto policy, your only source of UM/UIM coverage is the vehicle owner’s policy, which will cover you as an occupant.

What are my options if neither the vehicle owner nor I have UM/UIM coverage?

Without UM/UIM coverage on either policy, your main option is a direct lawsuit against the at-fault driver for their personal assets, though recovery is often difficult when the driver carries no insurance. Texas law also allows claims against third parties that may share fault, such as a government entity responsible for a road defect.

How long does a passenger have to file a UM/UIM claim in Texas?

Texas treats UM/UIM claims as first-party contract disputes, which generally have a longer statute of limitations than the two-year deadline for personal injury lawsuits. But many policies contain shorter contractual claim deadlines. Check your policy’s terms, and report the accident to your insurer as soon as possible after the accident.

Will filing a UM/UIM claim through a friend's policy raise their insurance premiums?

Filing a UM/UIM claim through the vehicle owner’s policy may affect their rates at renewal, depending on their insurer’s surcharge rules. Texas law does not prohibit insurers from increasing premiums after a UM/UIM claim, even when the policyholder was not at fault.

Can a passenger collect both PIP and UM/UIM benefits after the same crash?

Yes. PIP and UM/UIM are separate types of coverage that can pay claims after the same accident. PIP pays regardless of fault and covers medical expenses and lost wages up to the policy limit; UM/UIM compensates for the at-fault driver’s lack of adequate coverage and covers broader damages, including pain and suffering.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...