What Happens When a Truck Driver Is Underinsured

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

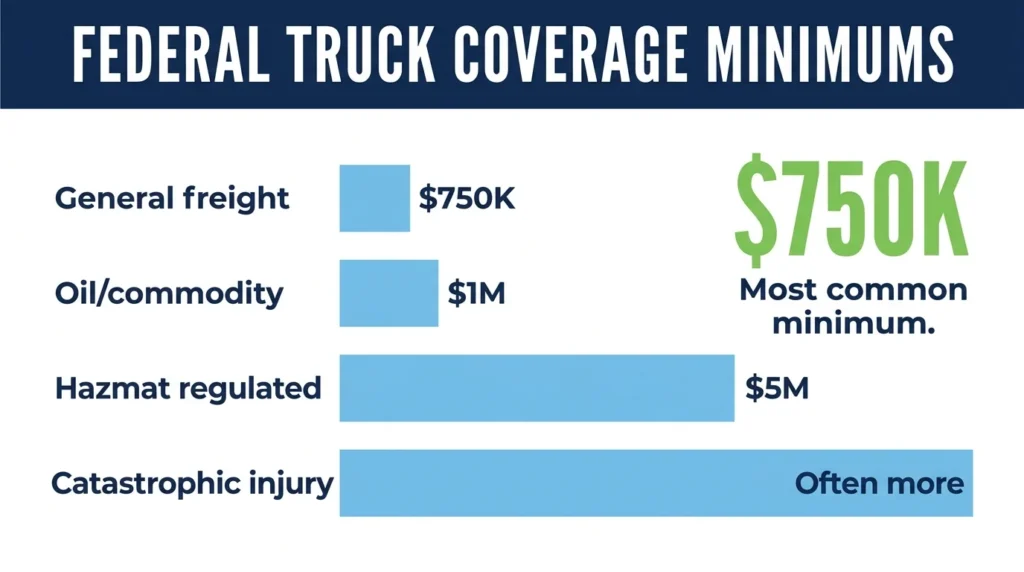

- Federal law requires motor carriers to carry a minimum of $750,000 in liability insurance for general freight, a figure that catastrophic-injury claims can easily exceed.

- The driver's underinsured status does not limit recovery. The motor carrier, the freight broker, and the shipper may carry independent coverage and face independent liability.

- Texas UIM coverage responds after the at-fault driver's limits are exhausted, but policyholders must have purchased that coverage and must follow consent-to-settle requirements to protect it.

You were seriously injured in a commercial truck crash. The insurance adjuster told you that the driver’s policy limit is $750,000, but your medical bills alone are approaching that number. You want to know whether that’s the top dollar figure or if there’s room for negotiation. In most collisions involving commercial trucks, the policy limit is not the final number.

What “Underinsured” Means After a Commercial Truck Crash

A truck driver is underinsured when their applicable liability policy limits are exhausted before a victim’s full damages are paid. Being underinsured is not the same as being uninsured, since the driver has coverage but just not enough. And the legal strategy for recovering damages from an underinsured driver is different from the one you’d use to pursue compensation from an uninsured driver.

Catastrophic injuries (spinal cord damage, traumatic brain injury, permanent disability, multiple fractures) often result in economic damages that exceed what a single policy covers. Medical expenses, lost income over years or decades of a career, future care costs, and noneconomic damages can push a legitimate claim well past the driver’s policy limits.

But the driver’s policy limits aren’t the only source to tap, as a case often includes multiple defendants, multiple insurers, and the victim’s own insurance company that provides underinsured motorist coverage.

Understanding the insurance requirements for commercial truck companies will help you get the maximum compensation for your injuries.

Federal Minimum Insurance Requirements and Why They Fall Short

Federal law sets insurance minimums for commercial trucks, but these are lower than what most people outside the industry expect. Under 49 CFR, Part 387, the required minimum public liability coverage for a for-hire motor carrier depends on what materials the vehicle is carrying.

For nonhazardous general freight (the most common commercial truck load), the minimum insurance required is $750,000. For oil and certain other regulated commodities transported in bulk, the minimum rises to $1 million. For hazardous materials transported in bulk, the minimum reaches $5 million.

The problem is that a carrier operating a general freight truck that has the $750,000 minimum insurance will easily face financial distress if the truck driver is at fault in a crash. A single hospitalization, emergency surgery, extended rehabilitation, and the cost of future medical care for a permanently disabled victim add up to way more than $750,000.

How Motor Carriers Are Held Accountable

The MCS-90 is a federal government insurance endorsement that requires motor carriers’ insurers to pay damages to accident victims up to the policy limits. But while the MCS-90 ensures that compensation at the limit is paid, the endorsement does not require insurers to pay out damages that exceed that amount.

Other Parties Who May Be Liable When Coverage Is Insufficient

In a commercial truck crash, the driver is rarely the only defendant whose conduct contributed to the wreck. These collisions often involve a chain of actors, each of whom may carry independent coverage.

For example, a motor carrier that hired a driver with a disqualifying safety record, that failed to enforce hours-of-service rules, or that allowed a truck with known mechanical problems to be put on the road can be held liable. When that happens, the amount the trucking company is held liable for must be covered by the carrier’s own policy, which may be the same policy that covers the driver, or a separate coverage layer.

In owner-operator arrangements, a lease agreement typically requires the motor carrier to provide coverage for the driver while operating under the carrier’s authority. The practical effect is that the carrier’s policy, not the driver’s bobtail policy, applies to a crash that occurs while the driver is on duty.

Freight brokers may face liability if they selected a carrier without doing adequate safety screening or with knowledge of the carrier’s prior violations. Brokers who carry contingent liability policies provide another coverage layer that may respond when the broker’s own negligence contributed to the crash.

If improperly loaded or unsecured cargo caused or contributed to the accident, the shipper can be held liable and its insurer will have to pay damages.

How Texas Underinsured Motorist Coverage Bridges the Gap

Texas law requires insurers to offer underinsured motorist coverage with every auto policy. You may reject it in writing, but the insurer must give you the option. If you accepted that coverage when you purchased your policy, it may respond after the at-fault driver’s limits are exhausted.

UIM coverage works on three conditions.

- First, the at-fault driver must have had liability insurance.

- Second, the driver’s policy must have paid out to the maximum amount.

- Third, the accident victim’s remaining unpaid damages must exceed the at-fault driver’s limits.

If you are injured in a wreck with a commercial truck and all of these conditions are met, your own insurer will pay up to the limit of your UIM policy to cover the shortfall.

Say that you have $250,000 in UIM coverage on a claim with $1 million in total damages and a $750,000 at-fault policy. You may receive the full $750,000 from the at-fault trucking company and then up to $250,000 from your UIM insurer, depending on offset provisions and policy language.

If you declined UIM coverage when you purchased your policy, that option is no longer available for this claim. Check out our Texas UM/UIM motorist accident guide and what falls under PIP, MedPay and UM/UIM.

How to Protect Your Claim When Policy Limits Are Low

If you find out that the truck driver’s policy limits are low, you should take the following steps simultaneously.

Pursue all potentially liable defendants from the start. Do not limit the claim to the driver alone before investigating the carrier’s conduct, the broker’s selection process, and the shipper’s loading decisions. Each of those parties carries independent coverage that may respond before or along with the driver’s policy.

Open a UIM claim with your own insurer at the same time as the third-party claim against the at-fault carrier. Waiting until the trucking company’s limits are exhausted can create procedural delays and consent-to-settle issues that affect your UIM recovery. Many UIM policies require the insurer’s consent before you settle with the at-fault carrier, and missing that step can affect your UIM rights.

Preserve all evidence of the crash before it is lost or destroyed. This includes electronic logging device data, black box information, driver qualification files, the carrier’s safety inspection history, and maintenance records. In commercial crashes, some of this evidence is kept for only a limited time.

Do not sign a release with the at-fault carrier’s insurer without confirming the effect on your UIM claim. A general release of “all claims” against the at-fault driver can unintentionally affect your ability to collect UIM benefits from your own insurer.

It’s essential to understand the full timeline of a Texas truck accident claim so that you make the right moves in each phase of the process.

Work with a Personal Injury Attorney

If the truck driver’s policy limits fall short of your damages, you will need to seek additional compensation from multiple defendants, which requires figuring out multiple coverage layers and procedural requirements. Angel Reyes & Associates has handled Texas truck accident cases for over 30 years. Our firm has recovered more than $1 billion for clients. We work on contingency, so we receive no fee unless we win your case. Contact us today for a free consultation.

Past results do not guarantee future outcomes.

Underinsured Truck Driver FAQs

How do you find out whether a trucking company has umbrella or excess insurance?

Umbrella or excess policies are usually identified through insurer disclosures, discovery, subpoenas, and a review of the motor carrier’s contracts and safety filings. These layers may matter when the primary trucking policy is not enough to cover serious injuries.

Can an injured person recover more than the truck driver’s insurance policy limits in Texas?

Yes, but usually not from the driver’s policy alone; additional recovery may depend on other liable parties, excess coverage, or the injured person’s own UIM coverage. Texas law requires UM/UIM coverage to be offered with auto policies, unless it is rejected in writing.

Does the MCS-90 endorsement create extra insurance after a truck crash?

No. The MCS-90 is a financial-responsibility endorsement that can require payment of a covered public-liability judgment, but it does not create unlimited coverage beyond the applicable required limits.

Will health insurance affect a settlement after an underinsured truck accident?

It can, because health insurers, Medicare, Medicaid, or medical providers may assert reimbursement or lien rights against a personal injury recovery. Those claims should be reviewed before settlement so the injured person understands what portion of the recovery may need to be repaid.

How long do you have to file a Texas truck accident lawsuit if insurance negotiations are still ongoing?

In most Texas personal injury cases, the deadline to file suit is two years from the date the claim accrues, and insurance negotiations usually do not extend that deadline. Texas Civil Practice and Remedies Code Section 16.003 controls the general two-year limitations period.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...