What Happens When an Unlicensed Driver Causes a Crash in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- An unlicensed driver's license status doesn't automatically determine fault; Texas comparative responsibility rules still require proof of who caused the crash.

- Insurance coverage may be denied due to named driver exclusions, unauthorized use disputes, or unlicensed driver exclusions, which makes your own UM/UIM coverage a critical backup.

- Texas has a two-year deadline for car accident claims, and coverage disputes in unlicensed driver cases can cause delays that put you at risk of missing the deadline.

You were driving home on Loop 410 in San Antonio when another car ran a red light and hit your passenger side. The police arrived, and you learned the other driver had a suspended license. Does this change the nature of your claim?

The short answer: it complicates things, but not in the way most people expect.

Liability in Unlicensed Driver Claims

Many people assume that if an unlicensed or suspended driver hits them, the driver is automatically at fault, and compensation will be higher. Unfortunately, that’s not how Texas law works.

License status doesn’t determine who caused the crash. Liability is still determined by who caused the crash and the evidence to support it. The driver who ran the red light is at fault because they violated traffic laws and caused the collision, but their license status is a separate issue.

These cases involve three key factors:

- Fault under Texas comparative responsibility rules

- Coverage availability and policy exclusions

- Alternative recovery paths (like UM/UIM claims and owner liability)

Each factor affects whether you can recover compensation and who will be responsible for paying damages. Understanding all three factors will help you avoid surprises when an insurer denies a claim or offers far less than your claim is worth.

What To Do In the First 72 Hours After a Crash

In these cases, it’s critical to document everything right away because coverage disputes and questions about who was driving or authorized to drive are common.

At the scene, collect the driver’s information and the vehicle owner’s information. Bear in mind that the driver and the vehicle owner may not be the same person. Get their insurance card, license plate, and VIN. If the driver mentions anything about their license status, make a note of it, but do not escalate the situation.

When the police arrive, confirm that the crash report lists the actual driver, the registered owner, and any witnesses. Check whether the officer issued any tickets related to license issues or the traffic violation that caused the crash.

Within the first few days, seek medical attention, even if your injuries seem minor. Keep a timeline of your symptoms. Save all receipts and avoid missing medical appointments because insurers will use this to argue that the crash did not cause your injuries or your injuries are not serious.

Comparative Responsibility in Texas

Texas uses a comparative responsibility system outlined in Texas Civil Practice and Remedies Code Chapter 33. This means that each party involved in a crash can be assigned a percentage of fault.

Here’s the critical rule: if you’re found more than 50% at fault, you cannot recover damages. This is sometimes called the “51% bar.”

This is why it’s important to watch what you say at the scene of the crash. Even saying something like “I didn’t see you” can be used against you later. Stick to the facts when speaking with the police and other drivers.

How Insurance Companies Use Unlicensed Driver Status to Challenge Claims

Even though license status doesn’t decide fault, insurers may use it to weaken your claim. Common tactics include arguing that you could have avoided the collision, that you were speeding, or that you weren’t paying attention.

Solid evidence dismantles these arguments. Photos of the scene, witness statements, and traffic camera footage all help establish what actually happened. Focus on the facts of the crash: who had the right of way, where the vehicles made contact, and which traffic laws were violated.

A traffic ticket supports your version of events, but it isn’t automatic proof that the other driver is responsible for the crash. The ticket only shows the officer’s opinion of what happened. Your claim still requires evidence of how the other driver’s actions caused your damages.

Will Insurance Cover an Accident if the Driver Is Unlicensed in Texas?

Coverage often depends on the policy and the driver’s relationship to the insured, not just whether they had a valid license.

If someone borrows a vehicle with permission from the owner, the owner’s policy usually provides primary coverage, but this can be limited by endorsements and exclusions in the policy.

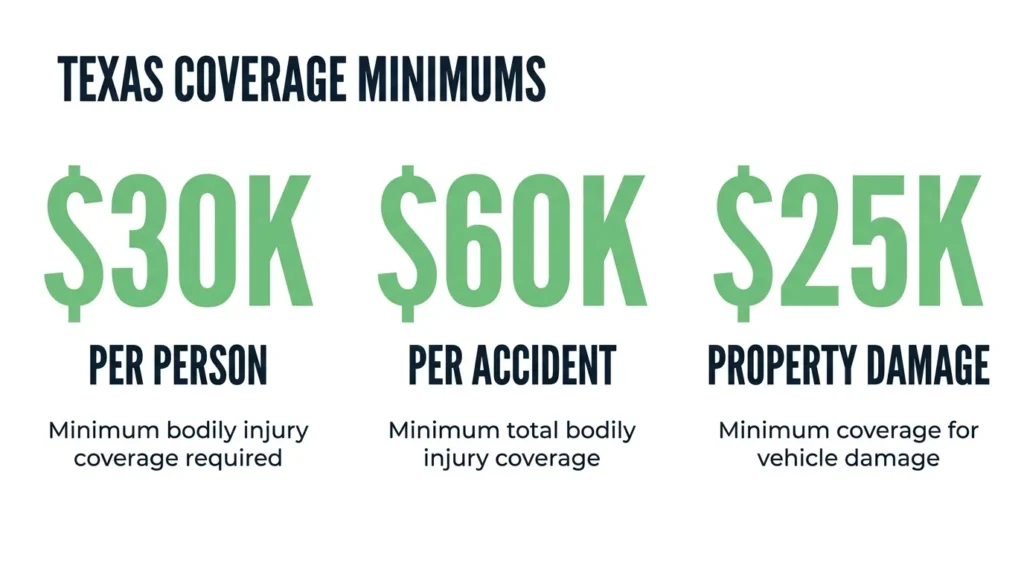

Texas requires drivers to have minimum liability coverage of $30,000 per person, $60,000 per accident for bodily injury, and $25,000 for property damage under Texas Transportation Code § 601.072. Even when the at-fault driver has this coverage, these minimums may not be enough to cover serious injuries.

Common Coverage Problems in Unlicensed Driver Crashes

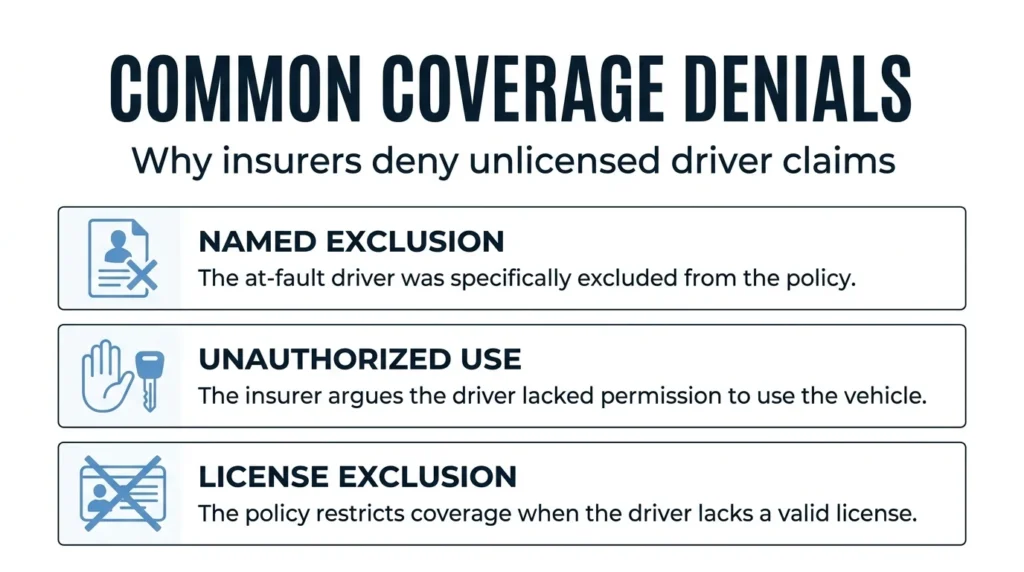

Several issues frequently cause carriers to deny or limit coverage:

- Named driver exclusions remove specific people from coverage. If the at-fault driver was excluded from the policy, the insurer will likely deny the liability claim entirely. You’ll need to understand what happens when someone lets an unlicensed driver use their car to evaluate your options.

- Unauthorized use disputes arise when insurers argue that the driver didn’t have permission to drive the vehicle. Evidence like text messages, prior instances of the driver borrowing the vehicle, or learning how the driver accessed the keys can resolve these disputes.

- Unlicensed driver exclusions appear in some policies and restrict coverage when the driver lacks a valid license. The exact policy language determines whether this applies.

If you receive a denial, request the denial letter and the policy with all endorsements. The specific reason for denial can determine what your next steps should be.

Your Recovery Options if the At-Fault Driver Has No Coverage

When liability coverage is missing or denied, you may still have paths to compensation.

Start by pursuing a claim with the at-fault driver’s or owner’s insurance company while you research alternative sources of compensation. This way, if the claim is delayed or denied, you’ll already have a backup plan ready.

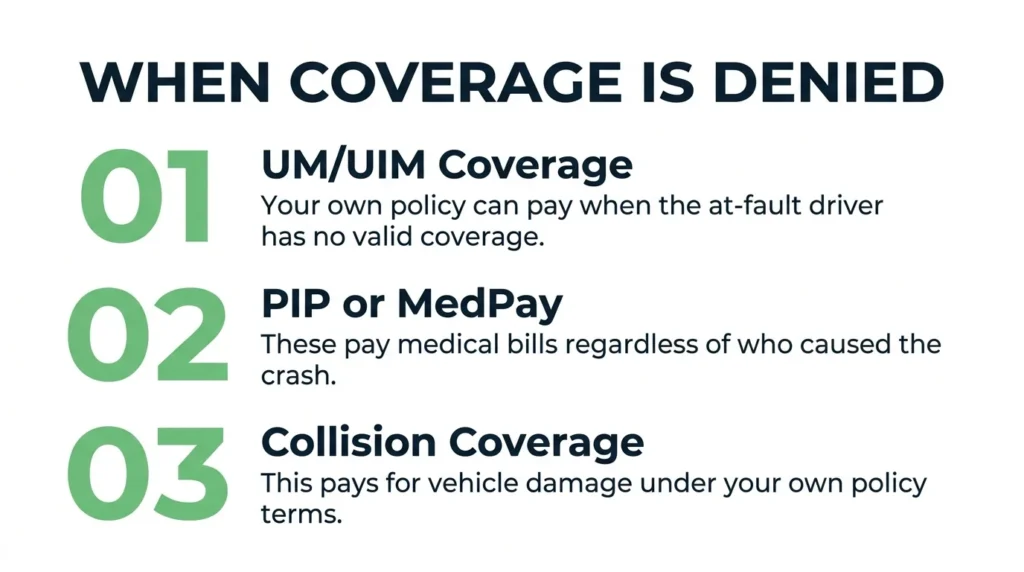

Your own policy may provide coverage through:

- UM/UIM (uninsured/underinsured motorist coverage)

- PIP or MedPay (for medical expenses)

- Collision coverage (for vehicle damage)

The available options will depend on the types of coverage you purchased. Review your declarations page or call your insurer to confirm which coverage you have.

Understanding UM/UIM Coverage

UM/UIM coverage becomes critical when the other driver has no insurance, does not have enough insurance, or their coverage is denied. This happens frequently in unlicensed driver accidents.

Under Texas Insurance Code § 1952.101, insurers must offer UM/UIM coverage. You can only decline it by rejecting it in writing. If you never signed a rejection form, then you likely have this coverage.

The Texas Department of Insurance explains that UM coverage for property damage may involve a deductible, but bodily injury coverage typically does not.

To support a UM/UIM claim, collect proof of the other driver’s fault, documentation of your damages, and evidence that the other driver did not have enough insurance coverage. This includes denial letters, the other driver’s declarations page, and/or confirmation that they had no insurance. Our uninsured motorist accident guide explains this process in detail.

Can You Sue the Owner for Letting an Unlicensed Driver Behind the Wheel?

If the driver is unlicensed, uninsured, or has no assets, the vehicle owner may be held responsible. Texas law allows claims against vehicle owners under a legal theory called “negligent entrustment.” This means the owner gave permission to use the vehicle while knowing the driver was unfit to operate the vehicle.

To prove this theory, you may be able to use an unlicensed or suspended license as relevant evidence, but it’s not automatic proof.

Further evidence that strengthens this claim includes:

- The owner’s knowledge of prior crashes or DWIs

- Known license suspensions or revocations

- Previous admissions that the driver had no license

- Patterns of letting the driver use the vehicle despite known risks

Other parties may share responsibility, depending on the facts of your claim. For example, if the driver was working at the time of the crash, then an employer might be liable. Angel Reyes & Associates handles car accidents and truck accidents involving multiple responsible parties.

Texas’s Two-Year Deadline for Filing a Lawsuit

Texas provides a two-year deadline for personal injury and property damage claims under Texas Civil Practice and Remedies Code § 16.003. If you miss this deadline, you lose the right to sue.

Unlicensed driver cases are often delayed due to coverage investigations. Insurers may take months to “review permission” or “evaluate exclusions.” Don’t let these delays push you past the deadline.

Preserve evidence early. Request traffic camera or surveillance footage quickly, as it’s often deleted within weeks. Keep your damaged vehicle or detailed photos of it. Obtain the 911 audio and crash report. Maintain consistent medical treatment records.

When It’s Worth Getting Legal Help

If the other driver is unlicensed, you may face problems collecting payment and determining insurance coverage. Both problems require legal strategies to resolve.

Consider speaking with an attorney if:

- You receive a denial letter

- The insurer claims the driver was excluded from the policy or an unauthorized user of the vehicle

- You have serious injuries

- Fault is disputed

- You need to negotiate a UM/UIM claim

A legal team can investigate the policy and its endorsements, evaluate whether the owner knew about the driver’s license status, identify all potentially liable parties, and organize all the evidence required to support your damages claim.

At Angel Reyes & Associates, we’ve spent over 30 years helping Texans navigate complicated car accident claims. We offer free consultations and work on contingency, which means there’s no fee unless we win. Our team can review your coverage options and help identify every available path to recovery.

If you’ve been hit by an unlicensed or suspended driver, contact us to discuss your situation. We’re available 24/7 and serve clients across Texas.

Past results do not guarantee future outcomes.

Unlicensed Driver FAQs

Can an unlicensed driver file a car accident claim in Texas?

Yes. Not having a valid license does not automatically prevent someone from making an injury or property damage claim if another driver caused the crash.

What if the unlicensed driver was driving a borrowed car in Texas?

The claim may involve both the driver and the vehicle owner, and coverage often depends on whether the owner gave permission and what the policy says. In some cases, there may also be a dispute over whether the driver was specifically excluded from the coverage.

Does uninsured motorist property damage coverage have a deductible in Texas?

Usually, yes. In Texas, uninsured motorist property damage coverage commonly comes with a deductible, while uninsured motorist bodily injury coverage generally does not.

What documents should I ask for if an insurance company denies coverage?

Ask for the written denial letter, the full policy, and any endorsements or exclusion forms that the insurer is relying on. These documents often show whether the denial is based on a named driver exclusion, a permission issue, or another policy term.

Can a passenger make a claim if the driver of the car was unlicensed?

Usually, yes. A passenger may still have a claim against the person or party that caused the wreck, even if the driver of the passenger’s vehicle did not have a valid license.

About the Authors

Spencer Browne

Writer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials across Texas. He focuses on car, truck, and wrongful death cases, with notable verdicts including a landmark win in the Choctaw Casino bus crash case. A recognized speaker and legal educator, Spencer is a member of the American Board of Trial Advocates and has been honored as a Texas Super Lawyer and one of D Magazine’s Best Lawyers in Dallas. He brings deep trial experience and relentless advocacy to every client he represents.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...