Can You Sue Uber for an Accident in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas lets injured people sue Uber directly under negligent hiring and app-period coverage theories.

- Uber's full $1 million commercial policy applies once a driver accepts a trip through drop-off.

- CPRC § 16.003 gives you two years from the crash date to file a Texas injury lawsuit.

You were riding home from a friend’s place in Deep Ellum when the Uber driver ran a stop sign on Commerce Street and got T-boned. Now your back is wrecked, the medical bills are stacking up, and an insurance rep just told you Uber has nothing to do with this because the driver was “an independent contractor.” That answer felt off the moment you heard it. It should.

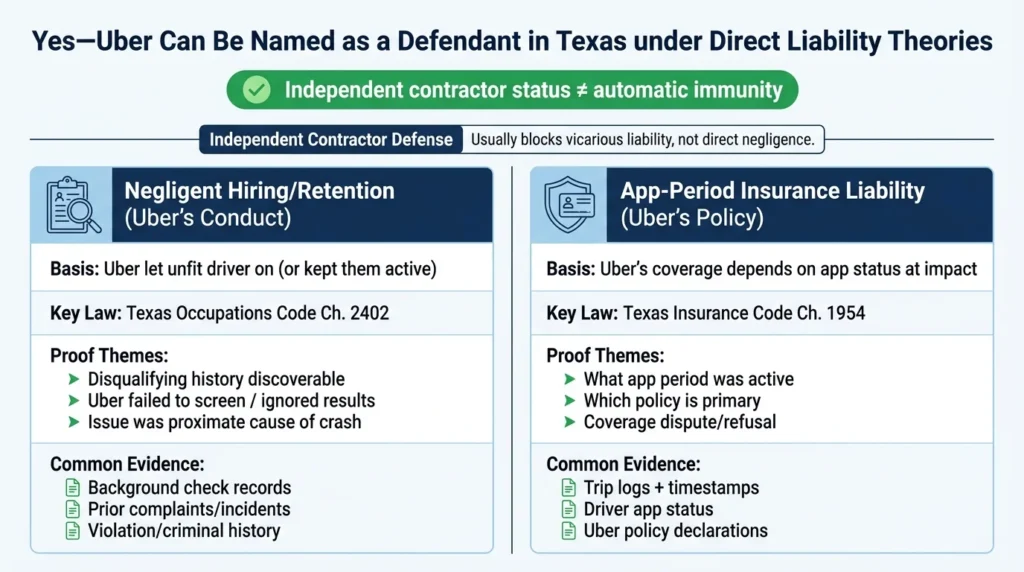

Yes, You Can Sue Uber in Texas

Texas law lets injured people name Uber as a defendant in a personal injury lawsuit, not just the driver. Two distinct theories support a direct claim against the company: negligent hiring and direct liability tied to Uber’s app-period insurance obligations. The independent contractor label does not shut either door, despite what insurance adjusters often suggest.

Which theory fits your case depends on the facts of the crash. The driver’s history, the moment the app was active, and what Uber’s own policy was supposed to cover are all important. A claim that gets nowhere on one theory may still succeed on the other, which is why the right framing of Texas rideshare accident claims is so important from day one.

Uber’s Independent Contractor Defense & Its Limits

Uber treats its drivers as independent contractors, and that classification usually defeats one type of claim: vicarious liability. Vicarious liability would hold Uber responsible for a driver’s bad driving simply because the driver works for the company. Direct negligence is different. It targets Uber’s own conduct, not the driver’s, and the contractor label does not block it.

A direct negligence claim looks at what Uber did or failed to do as a corporation. Did the company run the background check Texas requires? Did it ignore complaints about a dangerous driver? Did it meet its insurance obligations during the trip?

Texas courts treat these as separate questions from whether Uber controlled the driver’s steering wheel. If a vicarious liability theory gets dismissed, a direct negligence theory can still move forward. Reviewing how fault is determined in Texas crashes can help frame which theory applies to your situation.

Negligent Hiring Under Texas Occupations Code Chapter 2402

Texas requires every transportation network company to vet its drivers before granting platform access. Texas Occupations Code Chapter 2402, known as the Transportation Network Companies Act, sets the rules. When Uber lets a driver onto the app who should have been disqualified, an injured person can sue Uber directly for negligent hiring.

Section 2402.107 spells out the screening criteria. Drivers with certain felony convictions, DWIs within the preceding seven years, or more than three qualifying moving violations within the preceding three years are not supposed to make it onto the platform under Section 2402.107. If one of those drivers slipped through and caused your crash, Uber’s own conduct, not the driver’s, becomes the basis for the claim.

A negligent hiring case requires three pieces of proof. The driver’s disqualifying history had to be discoverable through the screening Uber was supposed to do. Uber either failed to check or ignored what the check showed. And that disqualifying issue had to be a proximate cause of the wreck.

Negligent retention is a close cousin. It applies when Uber received notice after onboarding, through complaints, prior incidents, or violations that should have triggered deactivation, but kept the driver active anyway. Damage values in these cases vary widely, and the average settlement in a Texas Uber accident depends heavily on which liability theory carries the case.

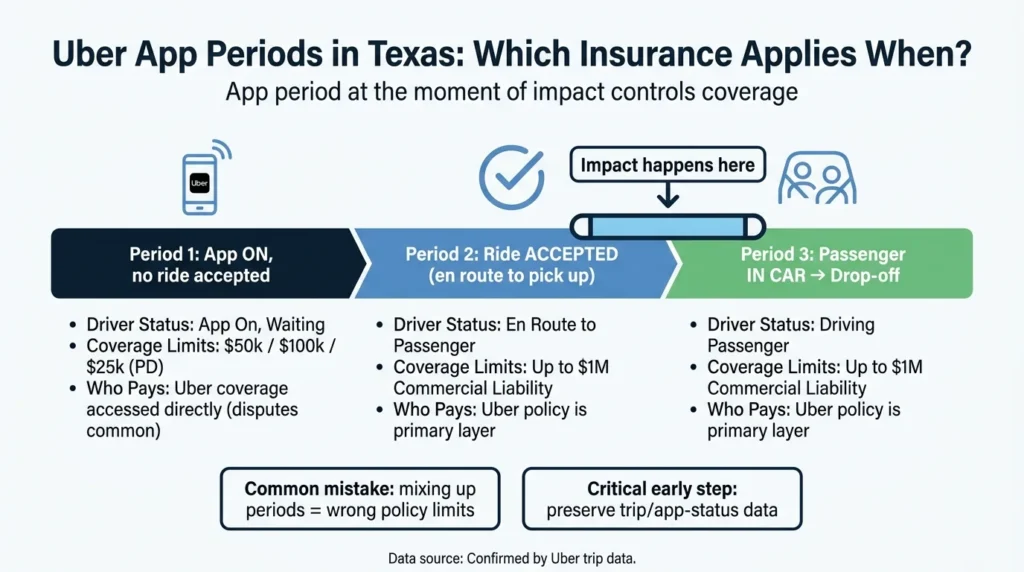

App Period & Which Insurance Covers Your Claim

The app period at the moment of impact decides which insurance policy is on the hook. Uber’s coverage tiers shift based on what the driver was doing when the crash happened. Conflating these periods is one of the most common, and most expensive, mistakes injured Texans make.

Period 1 Coverage (App On, No Ride Accepted)

When the app is open but no trip is accepted yet, Texas law requires minimum liability coverage of $50,000 per person, $100,000 per incident, and $25,000 for property damage. These limits are far lower than the full commercial policy that applies once a ride is accepted. The Texas Insurance Code Chapter 1954 sets the minimum coverage floor for this window.

Under Texas Insurance Code §1954.055, Uber’s coverage obligation during this window is not contingent on the driver’s personal auto insurer first denying the claim. Uber’s policy can be accessed directly, though disputes over which layer pays first are common and can delay recovery. That makes Uber a proper defendant when the Period 1 coverage is disputed or refused.

Periods 2 & 3 Coverage (Ride Accepted Through Drop-Off)

Once the driver accepts a trip, and through the moment the passenger steps out, Uber’s full commercial liability policy applies. That coverage currently sits at one million dollars per occurrence. During this window, the case for naming Uber directly is at its strongest, because Uber’s own policy is the primary layer of protection.

The exact app period at impact is a threshold factual question in every rideshare crash. It is established through trip data Uber keeps internally. Locking down that data early is critical, and it shapes how a Texas car accident claim involving a rideshare vehicle gets valued. Knowing which period was active can mean the difference between a one-million-dollar policy and a much smaller contingent limit.

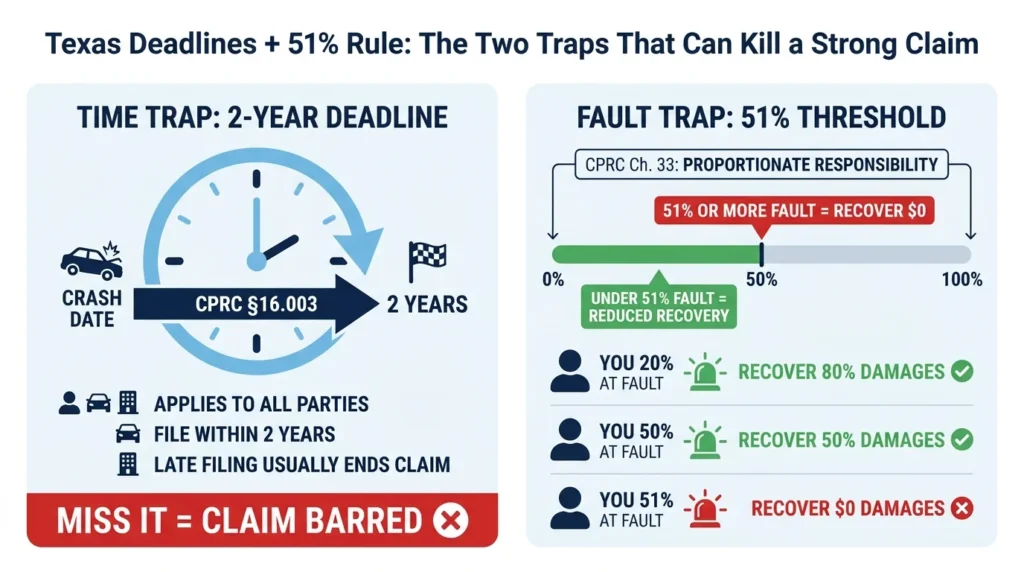

Filing Deadlines & Comparative Fault in Texas

Two rules can quietly end a strong case before it starts: the filing deadline and the way Texas splits fault among everyone involved. Both apply to claims against Uber and the driver.

The Texas Civil Practice and Remedies Code (CPRC) § 16.003 gives you two years from the date of the crash to file a personal injury lawsuit. That clock applies to claims against Uber, the driver, and any other party at fault. Missing it almost always bars recovery completely, no matter how strong the negligent hiring or coverage claim looked on paper.

Fault gets divided under CPRC Chapter 33, the proportionate responsibility statute. In a rideshare wreck, fault may be split among Uber, the Uber driver, other drivers, and you. A plaintiff assigned 51% or more of the total fault recovers nothing. Below that, your recovery is reduced by your assigned percentage.

Uber and its insurers will push to shift blame onto the driver or onto you. That tactic directly affects what your claim is worth. The Texas 51 percent comparative negligence rule explains how the math plays out when multiple parties share fault.

Talk to a Texas Rideshare Accident Attorney

Suing a company the size of Uber is not something to handle alone. Angel Reyes & Associates handles rideshare accident claims across Texas and has more than $1 billion recovered for clients. Past results do not guarantee future outcomes. We work on contingency, which means no fee unless we win, and our case results reflect decades of work for injured Texans. Contact us today to talk through what happened and what your claim may be worth.

Uber Accident Lawsuit FAQs

Can Uber deactivate a driver after a crash, and does that affect my claim?

Yes, Uber can deactivate a driver at any point, including after a reported accident. Deactivation does not resolve your claim or substitute for a legal settlement, and it has no effect on the two-year filing deadline that applies to your case.

Does uninsured motorist coverage apply if an Uber driver causes a crash?

If the at-fault Uber driver had no personal policy in effect and the crash occurred in Period 1, your own uninsured or underinsured motorist coverage may apply depending on your policy terms. Texas law does not require Uber to carry uninsured motorist coverage on its commercial policy, so your own policy language is important.

What if the Uber driver was in an accident caused by another driver, not the Uber driver?

Uber’s commercial policy can still apply during Periods 2 and 3, but your claim would primarily target the at-fault driver’s insurer. If that driver is underinsured, Uber’s underinsured motorist coverage may fill part of the gap, depending on the policy terms and the period active at the time of the crash.

Can a minor injured as an Uber passenger sue Uber in Texas?

Yes, but the two-year statute of limitations is tolled for minors in Texas, meaning the clock does not start until the minor turns 18. A parent or guardian may also bring a claim on the child’s behalf before that point under Texas Civil Practice and Remedies Code Section 16.001.

Does Texas law require Uber drivers to carry their own auto insurance?

Yes. Texas Occupations Code Chapter 2402 requires TNC drivers to maintain personal auto insurance that meets Texas minimums. However, many personal auto policies exclude coverage when the vehicle is used for hire, which is why Uber’s layered commercial coverage exists to fill those gaps.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...