What to Do If You Are Accused of Insurance Fraud in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas Penal Code Chapter 35 defines insurance fraud as knowingly making false material statements in connection with a claim.

- Special Investigations Unit “red flags” like inconsistent statements or treatment gaps prompt investigation but don’t prove fraud.

- Texas Insurance Code Chapter 541 requires insurers to handle claims fairly, even during fraud investigations, and you have the right to request written explanations for any denial or delay.

You were rear-ended in rush hour traffic on I-35 near downtown Austin last week. Your neck still hurts, and you’ve started physical therapy. Now the other driver’s insurance company wants a recorded statement, and the adjuster mentioned something about their “Special Investigations Unit” reviewing your claim. You haven’t done anything wrong, but suddenly this feels like more than a routine injury claim.

To put it simply: when an insurance company mentions getting their Special Investigations Unit (or SIU, for short) involved, what they are implying is that they suspect all or part of your claim may be fraudulent. One thing that’s important to know: this is not an accusation, and it does not mean your claim is invalid.

Fraud allegations in auto insurance claims catch more Texans off guard than you’d expect. Knowing what sets off these investigations and how to respond can be the difference between a paid claim and a prolonged legal nightmare.

How Texas Law Defines Insurance Fraud

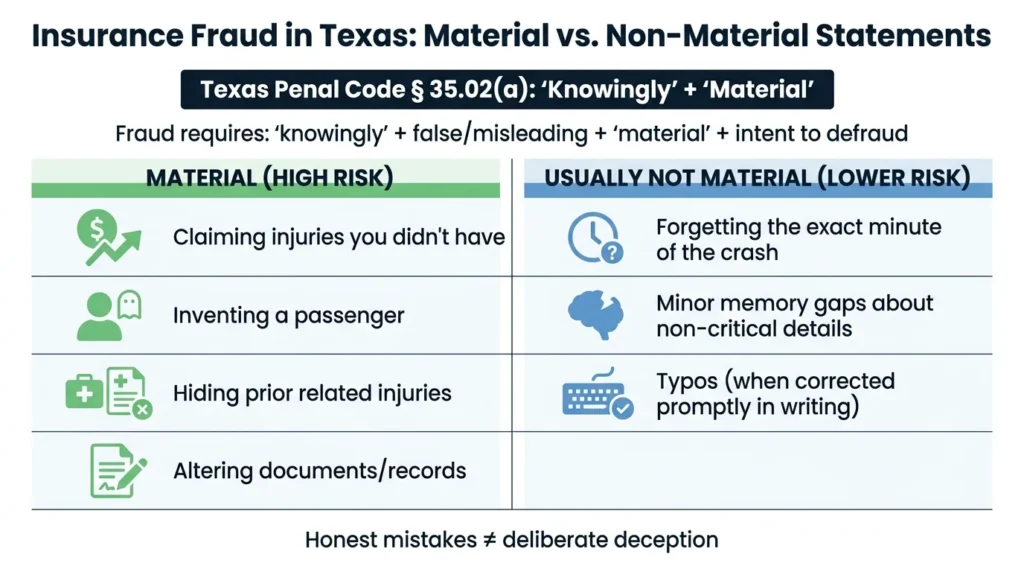

Texas Penal Code § 35.02(a) defines insurance fraud as knowingly making or causing a false or misleading material statement in connection with an insurance claim with the intent of defrauding the insurer. That word “knowingly” carries a lot of weight. Honest mistakes and foggy memory are not the same thing as deliberate deception.

Insurers know people make mistakes. In fact, they count on it. They won’t accuse you of fraud if you misremember something or you have a small detail wrong in your statement. However, if your statement and submitted evidence don’t seem to line up with the facts of your case, especially those unearthed through their own investigation, then they may get suspicious.

Insurers zero in on changing timelines, undisclosed prior injuries, and gaps in medical treatment because these patterns sometimes point to fraud. But they also sometimes point to nothing more than a shaken person trying to piece together a traumatic event.

These matters primarily center around material facts. A material fact is anything that would affect whether the insurer pays, how much they pay, or whether coverage even applies. Telling an adjuster you were injured when you weren’t? Material. Claiming a passenger was in your car who wasn’t? Material. Forgetting the exact minute the crash happened? Generally not.

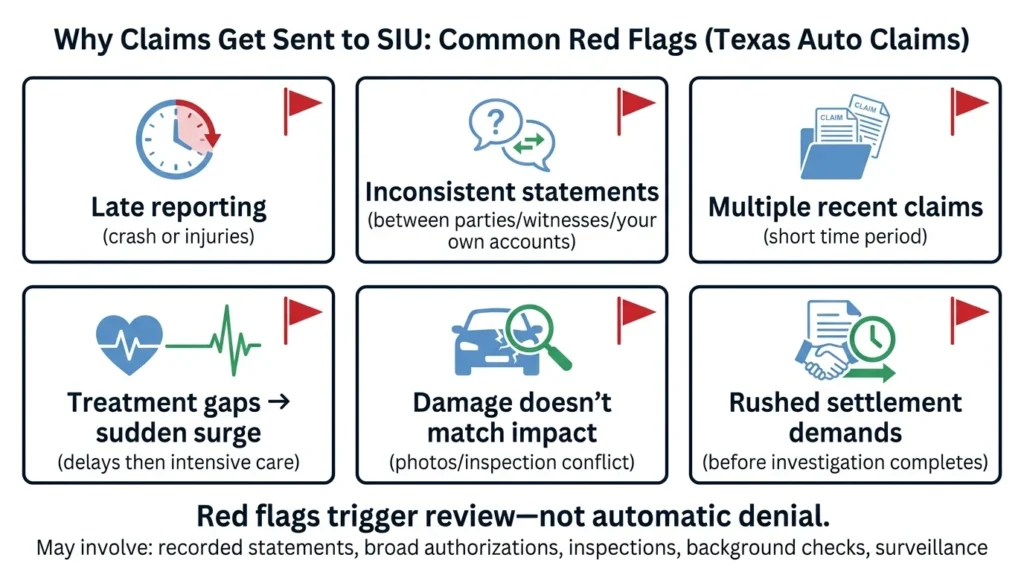

Why Claims Get Referred to Special Investigations Units

An SIU is an insurer’s in-house team for identifying potentially fraudulent claims. Most large carriers have one. A referral to SIU doesn’t mean you’re guilty of anything,it means something in your file caught their attention.

Common red flags in Texas auto claims include:

- Late reporting of the crash or injuries

- Inconsistent statements between parties, witnesses, or across your own accounts

- Multiple prior claims filed in a short period

- Treatment delays followed by a sudden surge in care

- Damage patterns that don’t match the described impact

- Settlement demands pushed through before the investigation wraps up

These flags trigger a closer look, not an automatic denial. The problem is that “closer look” often feels like an interrogation to someone who may already be going through a traumatic period in their life. The insurer may want recorded statements, sweeping medical authorizations, vehicle inspections, background checks, or even surveillance.

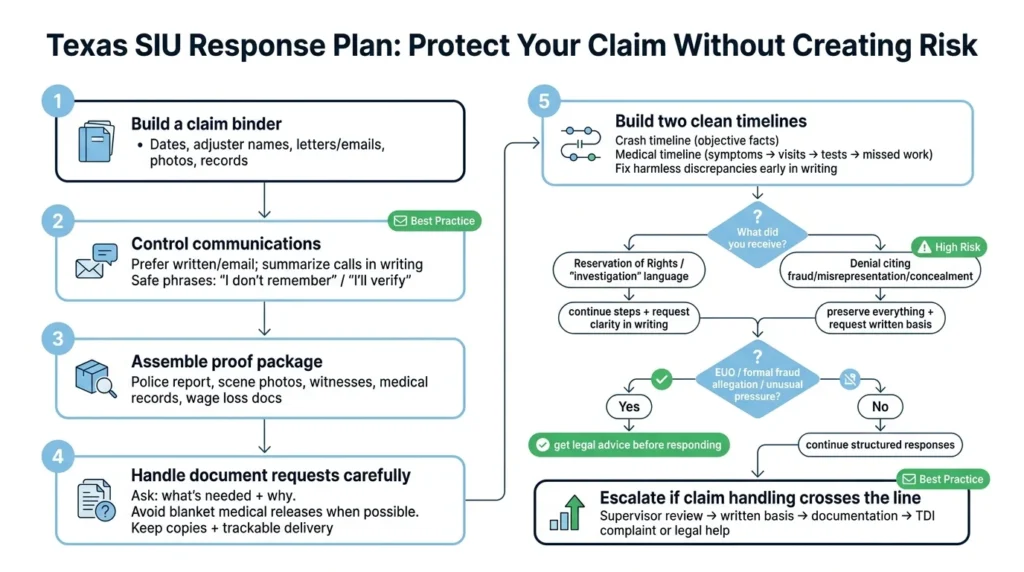

If you receive a “reservation of rights” letter or language about an ongoing investigation, the insurer is signalling they haven’t committed to paying. A denial letter citing “fraud,” “misrepresentation,” or “concealment” is a different, more serious situation. Save everything, resist the urge to argue on the phone, and ask for the specific basis for any denial in writing.

A Texas-Specific Response Plan for SIU Investigations

If you have a legitimate injury claim, protecting it through an investigation comes down to organization and discipline. Start by building a claim binder: every date, adjuster name, letter, email, photo, and medical record in one place. The Texas Department of Insurance recommends keeping detailed notes throughout any claim process.

Take control of your communications. Use email or written correspondence whenever you can. If a phone call is unavoidable, follow it up with a written summary of what was discussed. Never guess. “I don’t remember” and “I’ll need to verify that” are perfectly acceptable answers, and far safer than filling gaps with information you’re not certain about.

Pull together accurate, organized proof: the police report, scene photos, witness contact information, medical records you already have, and wage-loss documentation. Present this as a coherent package rather than piecemeal responses to individual requests.

Managing Document Requests

Insurers often ask for broad medical authorizations covering “all providers, all time.” That kind of blanket request can drag in unrelated records and create apparent inconsistencies where there are none. A narrower authorization, one covering treatment related to the crash and a reasonable look back for relevant prior conditions, is usually more appropriate.

When you respond to document requests:

- Ask specifically what’s needed and why

- Set reasonable deadlines

- Keep copies of everything you send

- Use trackable delivery methods

- Verify provider names and dates before submitting

High-risk items include blanket releases, pharmacy records going back years, and employment records that have nothing to do with your wage loss claim. Every document you hand over becomes part of the claim file, and it will be scrutinized for inconsistencies.

Building a Clean Timeline

A tight, consistent timeline undercuts “inconsistency” arguments before they can take hold. Build a crash narrative around objective facts: the time, location, vehicles involved, weather conditions, and police report number. Cross-reference it against your photos and witness accounts.

Build a parallel medical timeline: when symptoms first appeared, your first medical visit, referrals, diagnostic tests, and missed work days. Keep it aligned with your actual records. If you spot harmless discrepancies, a typo in a date, a misspelt provider name, address them in writing early. Don’t let them sit and become “evidence” of something they’re not.

Protecting Yourself from Criminal & Civil Exposure

Once “fraud” language enters the conversation, the stakes shift. Under Texas Insurance Code § 701.051, insurers have a duty to report suspected fraudulent insurance acts. That means what you say, and what you submit, may end up in front of authorities.

When you give a statement, remember: accuracy is more than speed. The risk of a misstatement getting reframed as fraud is low, but don’t overlook it. Stressed, medicated, or exhausted people often guess at details they don’t clearly remember, and those guesses can later be treated as intentional misrepresentations.

What not to do when SIU is involved:

- Don’t fill gaps with guesses. If you don’t know, say so.

- Don’t alter documents or “clean up” records. Preserve originals and explain errors transparently.

- Don’t post about the crash, your injuries, or your daily activities on social media while a dispute is active.

If you’re facing a formal fraud allegation, an Examination Under Oath request, or unusual investigative pressure, get legal advice before you respond. A car accident attorney can manage claim communications while you focus on getting better. In cases with potential criminal exposure, coordinated representation may be necessary.

Insurer Obligations Under Texas Law

Even if they suspect fraud, the insurer still has to play by the rules. Texas Insurance Code Chapter 541 addresses unfair methods of competition and deceptive practices, including specific unfair settlement practices under § 541.060.

Prohibited conduct includes misrepresenting policy provisions, refusing to offer a fair settlement when liability is reasonably clear, and failing to explain why a claim was denied. Fraud suspicion doesn’t give an insurer a blank check to delay indefinitely or hide behind vague denials. You have the right to a written explanation for any adverse decision.

If you think the investigation has crossed a line, escalate in order:

- Request supervisor review

- Request a written basis for any denial or delay

- Pull together your documentation

- Decide whether to file a TDI complaint or seek legal help

The Texas Department of Insurance draws a clear line between consumer complaints about claim handling and fraud reports about suspected criminal schemes. If you’re unsure which lane you’re in,or if you’re the target of a fraud allegation rather than a victim of one, legal guidance can help you figure out the right move.

How a Texas Car Accident Lawyer Can Help

When SIU is in the picture, having an attorney handle communications can prevent a lot of self-inflicted damage. A lawyer can organize your evidence, address inconsistencies before they become problems, and push back on claim handling that crosses the line.

Depending on the facts, outcomes might include a fair settlement, reversal of an improper denial, preparation for litigation, or documentation of statutory violations that support additional claims. Truck accident cases often face even more intensive scrutiny, higher damages, multiple insurance policies, and tangled liability questions, making early evidence preservation critical.

At Angel Reyes & Associates, we’ve spent over 30 years helping Texans navigate difficult insurance situations. We offer free consultations, and you pay nothing unless we recover compensation for you. With more than 20 offices across Texas, we can handle most of your cases remotely. If an SIU investigation is complicating your injury claim, contact us today to discuss your options.

Fraud Accusation FAQs

Can a typo or paperwork mistake turn into insurance fraud in Texas?

Usually, no, if it was an honest error and you correct it quickly. But repeated inconsistencies or errors involving important facts can raise suspicion. Fix mistakes in writing and keep a copy of the correction.

What is an Examination Under Oath in a Texas insurance claim?

An Examination Under Oath is a formal question-and-answer session where the insurer’s attorney asks about the claim while a court reporter records your answers. It’s more serious than a routine adjuster call, and many people get legal advice before attending.

Can an insurance company look at my social media during a fraud investigation?

Yes. Insurers may review public posts, photos, videos, and activity they believe relates to the crash or your injuries. Even harmless posts can be taken out of context, so it’s wise not to post about the accident or your physical activities while the claim is active.

Should I repair my car before the insurance investigation is finished?

If the car can be safely preserved, photograph it thoroughly and make sure the insurer has a chance to inspect it first. If you need to move forward sooner, keep detailed photos, repair estimates, invoices, and any damaged parts your shop can save.

What is the difference between a Texas Department of Insurance complaint and a fraud report?

A consumer complaint is generally for claim-handling problems like delay, poor communication, or an unexplained denial. A fraud report is for suspected criminal or dishonest conduct. The right option depends on whether you’re challenging how your claim was handled or reporting suspected fraud.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...