Does Insurance Cover Accidents in Parking Lots?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas insurance companies cover parking lot accidents through liability, collision, PIP/MedPay, and UM/UIM coverage.

- Since police often don't respond to private property crashes, fault decisions are determined by insurance companies and depend heavily on the evidence you collect.

- Thoroughly documenting the scene, gathering witness information, and collecting any other form of evidence immediately after your crash can strengthen your claim.

Estimates show that parking lot accidents account for approximately 20% of all car accidents in Texas. These types of accidents also create unique challenges when it comes to determining fault and providing coverage.

Understanding how Texas insurance companies handle these situations can help you strengthen and protect your claim from the start.

Why Parking Lot Crashes Are Handled Differently

Most parking lot collisions share a frustrating reality: limited official documentation. Police often will not respond to a car accident in a parking lot unless someone was injured.

This doesn’t mean your crash doesn’t matter. It means the burden of proving what happened shifts almost entirely to you and the evidence you collect.

Insurance companies still investigate these claims and assign fault. They still pay for covered losses. The difference is that adjusters rely heavily on photos, witness statements, surveillance footage, and damage patterns rather than police reports or citations. Your ability to thoroughly document the scene affects whether your claim succeeds.

How Insurance Companies Determine Fault in Parking Lot Accidents

Insurance adjusters determine fault independently of police conclusions. They evaluate parking lot conduct using the same principles that govern safe driving anywhere: maintaining a proper lookout, yielding when appropriate, backing up carefully, and operating at reasonable speeds.

In an effort to determine fault, they examine:

- Written and recorded statements from both drivers.

- Photos showing vehicle positions, damage locations, and lot layout.

- Surveillance footage from nearby businesses.

- Witness accounts.

- Physical evidence, like skid marks or debris patterns.

Inconsistent stories hurt your credibility. If your account changes between the scene, your initial claim report, and a recorded statement, adjusters will notice. Delayed reporting also raises questions about whether damage actually occurred as described.

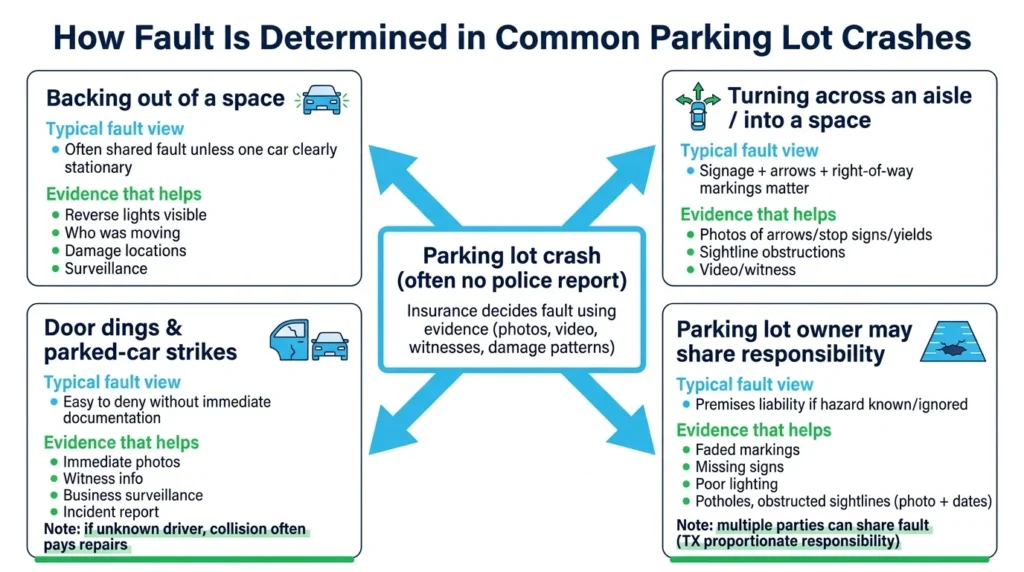

How Insurers Typically View Each Type of Parking Lot Accident

Parking lots produce predictable collision patterns. Understanding how insurers typically view these situations helps you anticipate fault arguments.

Backing Out of a Space

Backing collisions often result in shared fault unless one driver was clearly stationary. The driver backing out generally has a duty to ensure the path is clear. However, a driver traveling through the aisle also has a duty to maintain a proper lookout.

Evidence that can help your claim in this type of accident includes:

- Whether reverse lights were visible before impact.

- Which vehicle was moving at the moment of the collision.

- The extent and location of the damage on both vehicles.

- Any surveillance footage showing the accident taking place.

Insurers frequently assign partial fault to both drivers when both were moving.

Turning Across an Aisle

Disputes arise when one driver turns into a space or across an aisle while another vehicle is traveling through. Aisle direction, painted arrows, and stop signs influence fault arguments.

Claiming “I had the right of way” means little without objective proof. Photograph any directional markings, stop signs, or yield indicators. Note whether sightlines were obstructed by parked vehicles, shopping carts, or landscaping.

Door Dings & Parked Car Strikes

Even minor impacts can lead to denied claims without immediate documentation. If someone hits your parked car and you witness it, get their information immediately. If you return to find damage, check for witnesses and ask nearby businesses about surveillance footage.

When the other driver is unknown, your collision coverage typically handles repairs. Store security or property management may have incident reports or camera footage that can help identify the responsible party.

When the Parking Lot Owner May Be Responsible

Some parking lot crashes involve more than driver error. Dangerous conditions created or ignored by the property owner can contribute to collisions.

Premises liability claims focus on whether the owner or manager knew about a hazard and failed to fix it or warn visitors.

Common examples of parking lot owner negligence include:

- Faded or missing lane markings

- Confusing or contradictory directional arrows

- Broken or inadequate lighting

- Obstructed sightlines from landscaping or structures

- Missing stop signs at blind intersections

- Unrepaired potholes or uneven surfaces

These claims can exist alongside driver fault claims. Texas proportionate responsibility rules allow recovery from multiple parties based on each one’s share of fault.

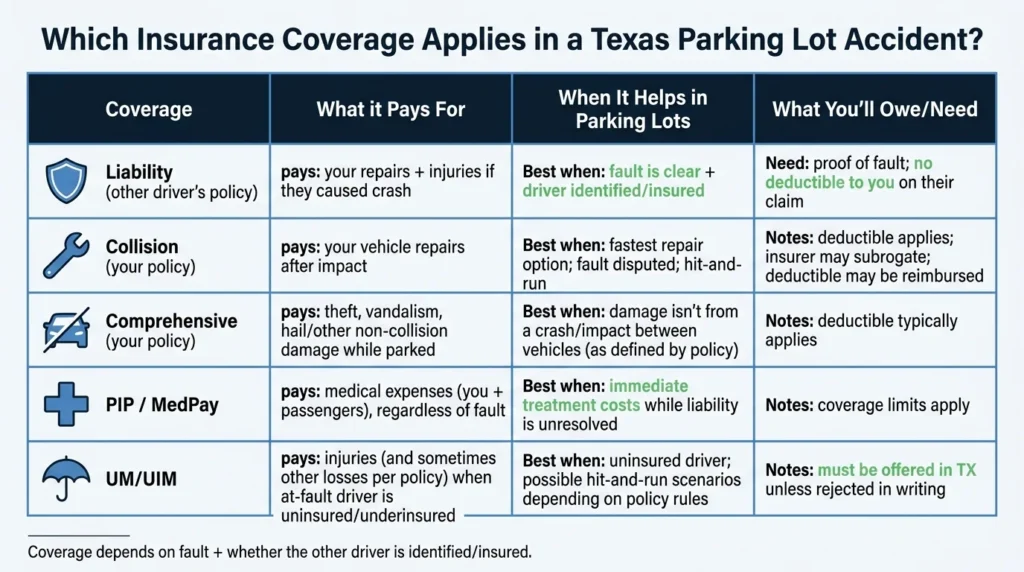

Auto Coverage You May Be Eligible for After a Texas Parking Lot Accident

Several types of auto insurance coverage may apply after a parking lot crash. The coverage you receive, if any, depends on fault, the type of loss, and whether the other driver is identified and insured.

The Texas Department of Insurance provides helpful explanations of standard coverage types.

Here’s how they typically apply to parking lot accidents:

- Liability coverage pays for injuries and property damage you cause to others. Texas law requires minimum limits of coverage under Texas Transportation Code § 601.072 ($30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage).

- Collision coverage pays to repair your vehicle after an impact, regardless of who caused it. You pay your deductible, and your insurer may pursue the other driver through subrogation (an insurer’s right to recover claim costs from the party at fault) to recover costs.

- Comprehensive coverage handles non-collision losses like theft, vandalism, or hail damage while your car is parked.

- PIP and MedPay cover medical expenses for you and your passengers regardless of fault. These can be valuable while liability questions are being sorted out.

- UM/UIM coverage protects you when the at-fault driver is uninsured or underinsured. Under Texas Insurance Code § 1952.101, insurers must offer this coverage unless you reject it in writing.

When the Other Driver Is at Fault: Liability Claims

If another driver caused your parking lot crash, their liability insurance should cover your vehicle repairs, medical bills, lost wages, and pain and suffering. The challenge is proving they were responsible.

Evidence that persuades adjusters in low-speed parking lot accidents includes:

- Video showing the other vehicle’s movement.

- Photos of the damage location being consistent with your account.

- Witness statements supporting your version.

- Damage patterns that match the described collision.

Common friction points include word-versus-word disputes, partial fault arguments, and lowball property damage offers. Adjusters for the other driver’s insurance company are working to minimize their payout. Having strong documentation and understanding your options helps counter these tactics.

Which Type of Coverage Is the Fastest?

Filing through your own collision coverage is often the fastest path to getting your car repaired. You don’t need to prove the other driver was at fault. You pay your deductible, choose a repair shop, and get your vehicle fixed.

Your insurer then pursues the other driver through subrogation. If they recover money, you may get your deductible reimbursed.

This approach makes sense when:

- The other driver’s fault is disputed.

- The other driver fled the scene.

- You need repairs quickly and can’t wait for a liability investigation.

- The other driver is uninsured.

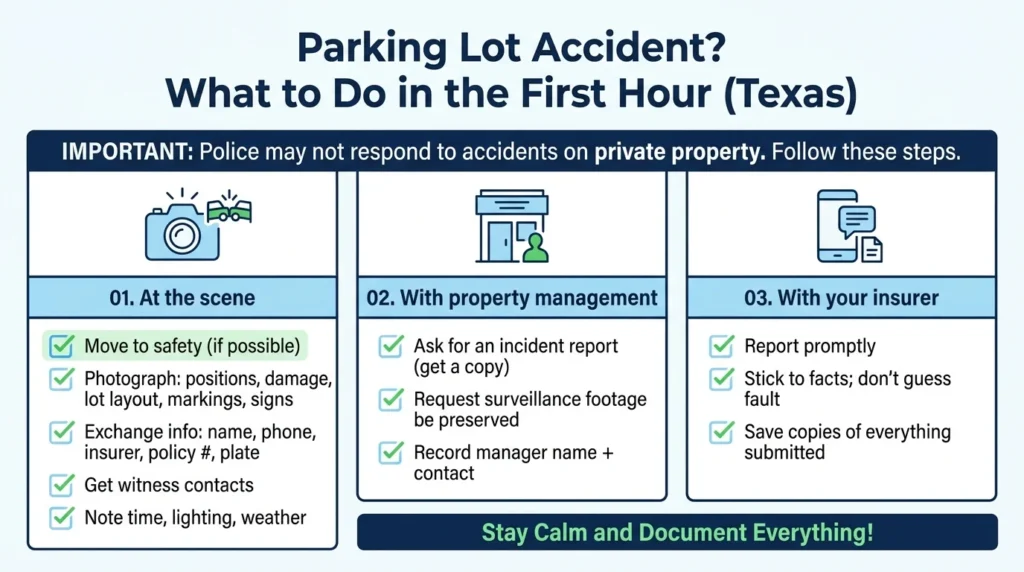

What to Do After a Parking Lot Accident in Texas

Your actions in the first hour after a parking lot crash significantly affect your claim outcome. Because police often don’t respond to these types of accidents, and video surveillance can disappear quickly, evidence collection falls to you.

Here’s what to do at the scene:

- Move to safety if possible, then photograph everything, including vehicle positions, damage, the lot layout, lane markings, and any signage.

- Exchange information with the other driver, including their name, phone number, insurance company, policy number, and license plate.

- Get contact information from any witnesses.

- Note the time, lighting conditions, and weather.

Here’s what you should do with property management:

- Ask for an incident report and get a copy.

- Request that surveillance footage be preserved.

- Get the manager’s name and contact information.

Here’s what you should do with your insurance company:

- Report the accident promptly.

- Stick to facts you know; avoid speculating about fault.

- Keep copies of everything you submit.

How Angel Reyes & Associates Can Help

Parking lot accident claims often become disputes about evidence and fault percentages. Insurance companies are businesses focused on minimizing payouts. When your word conflicts with another driver’s, or when an adjuster assigns you partial fault you don’t deserve, having experienced legal guidance matters.

At Angel Reyes & Associates, our team has spent over 30 years helping Texas accident victims navigate insurance claims and recover fair compensation. We’ve recovered more than $1 billion for our clients. We offer free consultations and work on contingency, meaning you pay no fees unless we win.

If you’ve been injured in a parking lot accident or if you’re facing a disputed claim, contact us to discuss your situation. We serve clients throughout Texas with 16 locations across the state and can handle most of your case remotely.

Parking Lot Accident FAQs

Will a parking lot accident raise my insurance rates in Texas?

It can, but rate changes depend on your insurer, your claim history, and whether the company decides you were at fault. Even a not-at-fault claim may affect future pricing in some situations.

Can I use uninsured motorist coverage if my parked car was hit and the driver was never found?

Possibly, but it depends on your policy and the type of loss. In many cases, collision coverage is the main source for vehicle repairs, while UM/UIM may be more important if you were injured or the facts meet your policy’s requirements.

What if a shopping cart damaged my car in a Texas parking lot?

Coverage often depends on what caused the cart to move and whether anyone was negligent. Your collision or comprehensive coverage may apply in some cases, and a property owner or another person could also be responsible if the facts support it.

Do I have to pay a deductible for a parking lot accident claim?

Usually, yes, if you use your own collision or comprehensive coverage, because this type of coverage commonly has deductibles. If the other driver’s insurer accepts full responsibility, you generally would not pay your own deductible through that third-party claim.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...