How to Claim Lost Wages After a Car Accident in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas PIP coverage can pay a portion of lost wages (often up to 80%) within 30 days after you submit satisfactory proof, regardless of who caused the crash.

- MedPay typically covers only medical expenses, not lost income, so check your policy for PIP or UM/UIM if you need wage replacement.

- Procuring and providing complete documentation (employer letter, doctor's work restrictions, pay stubs) from day one prevents the most common claim denials and delays.

You were rear-ended in rush hour traffic on I-35 last week. The doctor says you need at least two weeks off work, but your bills keep coming. Now, you’re wondering how you’ll replace your missing paycheck while you recover.

The good news: Texas drivers often have more than one path to claim lost wages after a crash. Understanding how much each type of coverage pays (and when you’ll be paid) can help you get your money faster and avoid common claim mistakes.

What “Lost Wages” Means in a Texas Car Accident Claim

Lost wages include more than just the hours you missed. They can cover your reduced schedule when you return on light duty, overtime you would have worked, and bonuses you missed because you couldn’t hit your targets.

The key distinction is that “lost wages” refers to income you’ve already lost. “Loss of earning capacity” describes long-term impacts on your ability to earn.

First-party insurance coverages like PIP typically address immediate lost wages. Long-term earning capacity claims usually come through an injury lawsuit against the at-fault driver.

Your fastest path to wage replacement usually runs through your own policy’s coverage, rather than waiting on the other driver’s insurance to accept fault. However, policy limits and proof requirements determine how much you can actually recover.

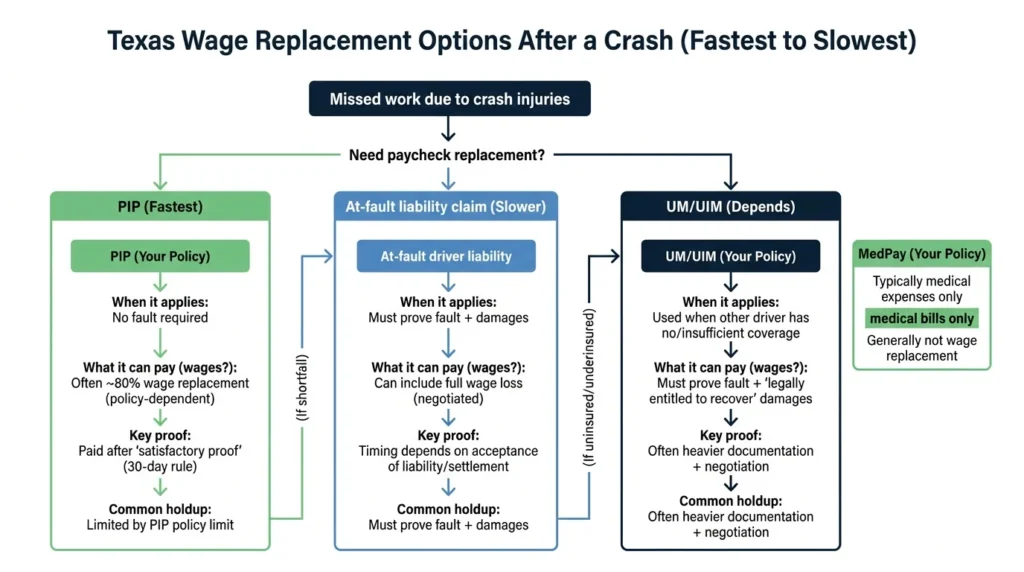

Where Wage Replacement Comes From

Most Texas drivers should think about wage replacement in this order:

- PIP (Personal Injury Protection) on your own policy pays regardless of fault.

- Liability claim against the at-fault driver’s insurance requires proving fault.

- UM/UIM (Uninsured/Underinsured Motorist) on your own policy kicks in when the at-fault driver can’t fully pay the claim.

Here’s where confusion often starts: [MedPay is not the same as PIP] (/blog/pip-vs-medpay-vs-um-uim/). MedPay typically covers medical expenses only. It generally won’t reimburse your lost wages. If you’re counting on MedPay for income replacement, you may need to adjust your strategy.

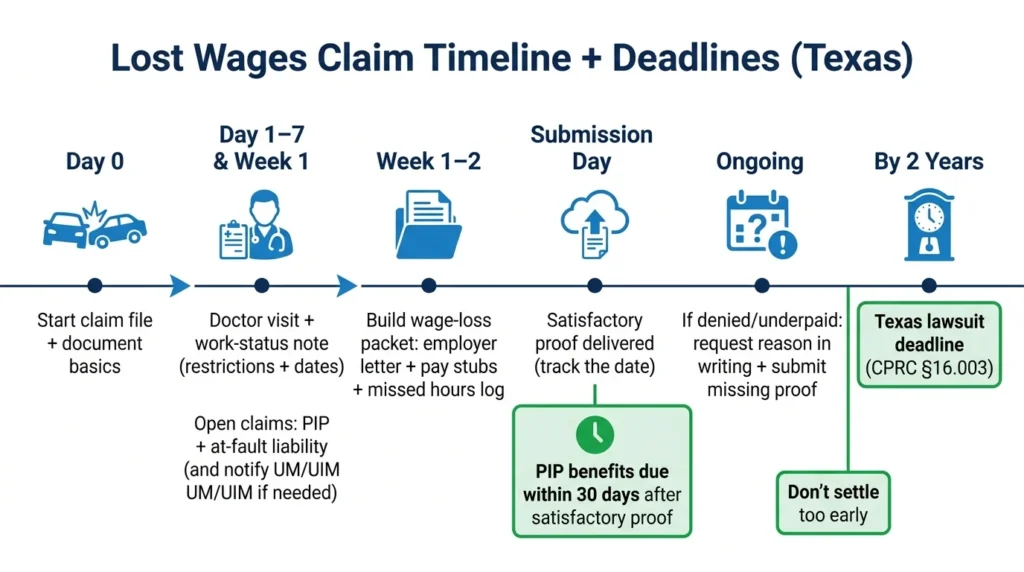

You’re also working against two different clocks. Insurance claim deadlines run on their own timeline, while Texas law gives you two years from the crash date to file a personal injury lawsuit under Texas Civil Practice and Remedies Code § 16.003. Missing either deadline can cost you.

PIP vs MedPay vs UM/UIM for Wage Loss

PIP includes income replacement as a stated benefit under Texas Insurance Code § 1952. It can pay a portion of your lost wages (commonly up to 80%) within your policy limits.

MedPay typically applies only to medical bills. Check your specific policy language, but don’t expect wage reimbursement from this coverage.

UM/UIM can pay wage loss as part of the damages you’re legally entitled to recover when the at-fault driver has limited or no insurance. The Texas Department of Insurance explains these coverages in plain terms.

PIP: The Fastest Path to Wage Replacement

PIP works as a first-party benefit. You file with your own insurer, and fault doesn’t matter. Texas insurers must offer PIP coverage, though drivers can reject it in writing.

PIP can pay a portion of your lost income up to your policy limits. Many policies pay around 80% of lost wages, but your actual coverage depends on your specific policy terms. If you earn $1,000 per week and miss three weeks, PIP might cover $2,400 of that $3,000 gap (assuming adequate limits).

The remaining 20% and any amount beyond your PIP limits must come from other sources: the at-fault driver’s liability coverage, your UM/UIM coverage, or a lawsuit.

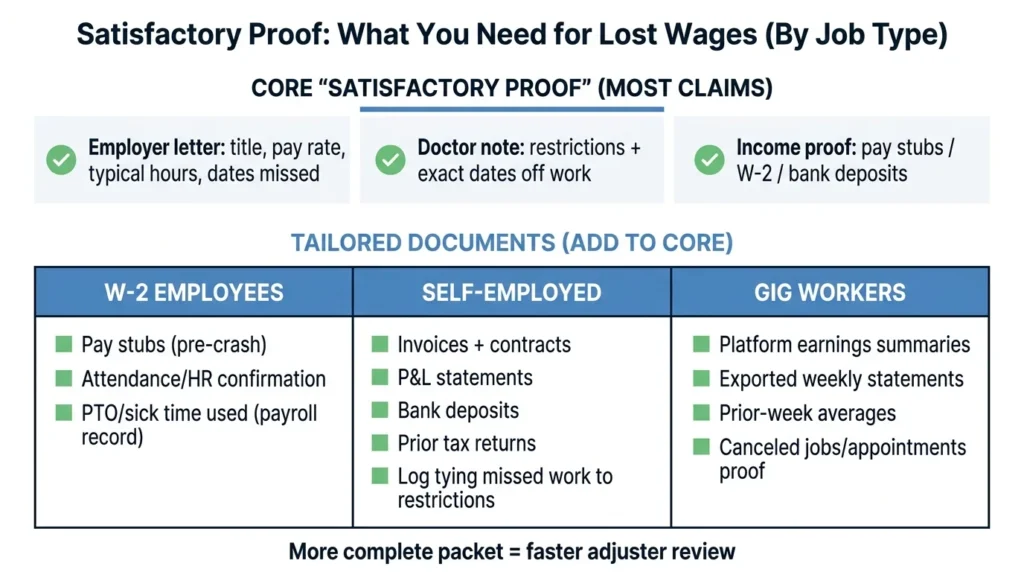

What “Satisfactory Proof” Means

Your PIP insurer needs documentation before they’ll pay. “Satisfactory proof” typically includes:

- Proof you missed work: An employer verification letter stating your job title, pay rate, typical hours, and specific dates missed

- Proof the crash caused the absence: A doctor’s note or work-status report with your restrictions and dates

- Proof of income amount: Recent pay stubs, your W-2, or bank statements showing direct deposits

The more complete your initial submission is, the faster payment typically arrives. Texas Insurance Code Chapter 1952 requires insurers to pay PIP benefits within 30 days after receiving satisfactory proof of loss. That clock starts when they have everything they need.

When UM/UIM Can Pay Lost Wages

Uninsured Motorist (UM) coverage applies when the at-fault driver has no insurance. Underinsured Motorist (UIM) coverage applies when the at-fault driver’s insurance limits aren’t enough to cover your damages.

Under Texas Insurance Code § 1952.101, insurers must offer UM/UIM coverage unless you reject it in writing. These coverages can pay for damages you’re “legally entitled to recover” from the at-fault driver, including lost wages.

The difference between UM/UIM and PIP: UM/UIM claims often require more proof of fault and damages. You’re essentially making a mini injury claim against your own insurer, from the perspective of the uninsured or underinsured driver.

Evidence UM/UIM Adjusters Look For

Beyond wage documentation, UM/UIM adjusters typically want to see:

- Liability support: The crash report, witness statements, photos, and anything showing the other driver was at fault

- Medical causation: Treatment records connecting your injuries to the crash, and work restrictions to those injuries

- Wage calculations: The same employer letters and pay stubs, plus clear math showing past losses and anticipated future restrictions

Step-by-Step: How to Claim Lost Wages in Texas

Step 1: Identify your coverages and open the right claims. File a PIP claim with your own insurer. File a liability claim with the at-fault driver’s insurer. If they’re uninsured or underinsured, notify your own insurer about a potential UM/UIM claim.

Step 2: Get medical work-status documentation immediately. Ask your doctor for a written note specifying your restrictions and the dates you cannot work. Update this as your condition changes.

Step 3: Build your wage-loss packet. Gather your employer verification letter, recent pay stubs, and a log of missed hours. Include documentation of typical overtime or bonuses if applicable.

Step 4: Submit everything and track deadlines. Confirm receipt in writing. Note the date you submitted satisfactory proof, so you can track the 30-day PIP payment window.

Step 5: If denied or underpaid, get the reason in writing. Ask specifically what’s missing or disputed. You may need additional documentation or legal help to resolve the issue.

How to Calculate Lost Wages

Hourly workers: Multiply your regular hourly rate by your missed hours. Calculate overtime separately if you have documentation showing you typically worked extra hours.

Salaried workers: Divide your annual salary by work days per year to get your daily rate. Multiply by days missed.

Variable income: Average your earnings over a recent period (e.g., the last 3-6 months) using bank deposits or pay records. Insurers scrutinize variable income more closely, so thorough documentation is key.

Documentation Checklist by Employment Type

W-2 Employees: Employer verification letter, pre-crash pay stubs, attendance records, HR confirmation of days missed, PTO or sick-time usage details

Self-Employed: Invoices, profit/loss statements, bank deposits, client contracts, prior tax returns, and a detailed log of missed work tied to medical restrictions

Gig Workers: Platform earnings summaries, exported statements, prior-week averages, and documentation of cancelled jobs or appointments.

Common Denial & Underpayment Pitfalls

Missing causation link: Your doctor’s note doesn’t cover the exact dates you missed, or there’s no written restriction at all.

Incomplete wage proof: Your employer won’t respond, your income varies without supporting documents, or your self-employment records are disorganized.

Policy limit surprise: PIP limits cap your quick-pay benefits. A $2,500 PIP limit won’t cover $5,000 in lost wages. The remainder must come from liability or UM/UIM claims.

Recorded statement mistakes: Inconsistencies between what you tell the adjuster and what your documents show can create disputes about your ability to work.

When to Talk to a Lawyer About Lost Wages

Consider getting legal help when:

- Your claim is denied or delayed despite submitting complete documentation

- The adjuster keeps requesting additional proof without clear explanations

- Your lost wages significantly exceed your PIP limits

- You’re self-employed with complex income documentation

- The at-fault driver is uninsured or underinsured

At Angel Reyes & Associates, we’ve spent over 30 years helping Texas crash victims recover what they’re owed. We offer free consultations, and you pay nothing unless we win. Our team has recovered more than $1 billion for clients across the state. Reach out to us today to discuss your wage-loss claim and understand your options.

Past results do not guarantee future outcomes.

Lost Wage FAQs

Can I get paid for sick days or PTO that I had to use after a car accident in Texas?

Sometimes, yes—using PTO or sick leave can still reflect real wage-related loss, but insurers may ask for payroll records showing that the time was used due to crash-related absences. Whether it is reimbursed may depend on your policy language and the facts of your claim.

What if my employer lets me work light duty or work from home after the crash?

You may still have a wage-loss claim if your hours, pay, commissions, or bonuses dropped due to medical restrictions. Keep records that show the difference between what you normally earned and what you earned while restricted.

Do I need the police report to claim lost wages in Texas?

You do not always need the police report for a basic PIP claim, but it can help confirm the crash date and support related claims. For UM/UIM or liability claims, the police report is often more important because fault becomes a bigger issue.

Can passengers use PIP for lost wages after a Texas car wreck?

Often yes—if PIP applies under the policy covering the vehicle or another applicable auto policy, as PIP can extend to certain passengers in addition to the named insured. Coverage depends on who is insured under the policy and the exact policy terms.

What happens if the at-fault driver’s insurer offers a settlement before I know how much time I will miss from work?

In this case, you must be careful because a settlement release may hinder your ability to seek additional wage losses later. It is usually smart to make sure your missed time, work restrictions, and expected return-to-work plan are reasonably clear before signing anything.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...