Electric Air Taxi Insurance in Texas: How eVTOL Coverage Works

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- eVTOL trips involve multiple separate policies, and gaps between them can affect your injury claim.

- Federal law sets an insurance floor for air taxi operators, but Texas contracts often require more.

- Texas law gives you two years to file a claim, but key evidence must be preserved well before then.

You have probably seen the test footage, a quiet multi-rotor aircraft lifting off somewhere in Texas and wondered what it was. Those are electric air taxis, and the day you can book one for yourself is getting closer. Before that day comes, it is worth knowing that the insurance behind these flights works nothing like what covers your car or a commercial airline ticket.

What Makes eVTOL Insurance Different From Car or Airline Coverage

When you fly on a major airline, a single federal regulatory framework governs the carrier’s liability. When you ride in a car, Texas auto insurance law sets the floor. eVTOL air taxi operations sit in a different category, and the coverage picture involves several separate policies that do not always work together cleanly.

The operator running the service carries aviation liability coverage, which pays for passenger injuries caused by flight operations. But that is not the only policy in play. A commercial general liability policy covers injuries that happen on the ground at the vertiport, the facility where passengers board and exit the aircraft.

Auto coverage applies if a shuttle transports you to or from the vertiport. Each policy covers a different phase of your trip, and gaps between them are common.

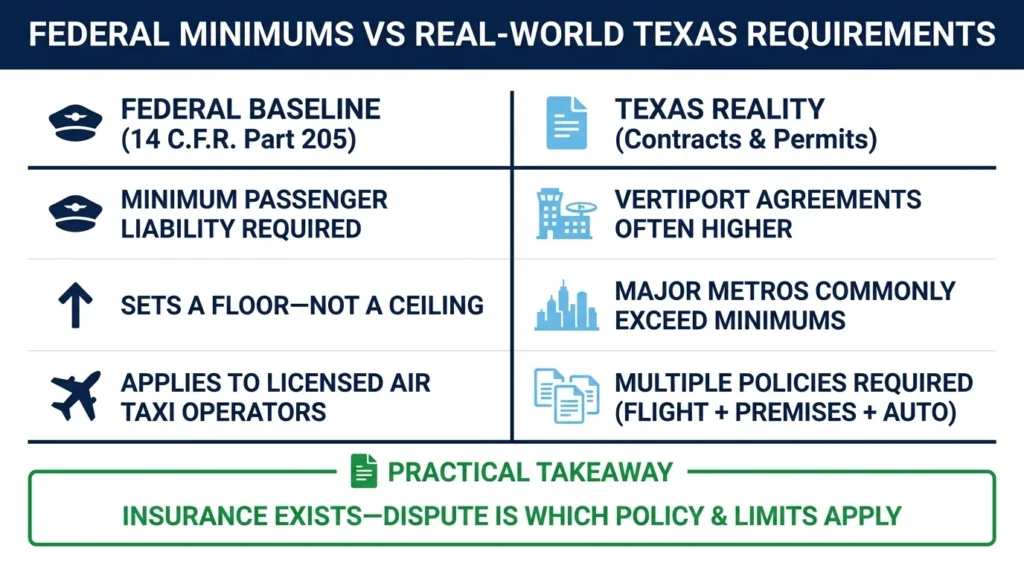

What Federal Minimums Actually Require

Federal regulations under 14 C.F.R. Part 205 require commercial air taxi operators to carry minimum liability coverage for passenger injuries and deaths. These are floor requirements. Vertiport agreements and operating contracts in Dallas, Houston, and other Texas cities routinely require operators to carry limits far above the federal minimum.

The practical takeaway: a licensed air taxi operator will have insurance. The question after an incident is which policy responds to your specific injury and whether the limits are adequate.

How the Coverage Layers Affect You as a Passenger

Most eVTOL operators carry multiple policies because no single policy covers every exposure. Understanding how they divide responsibility helps you know where a claim goes if something goes wrong.

Aviation liability covers bodily injury during flight. It typically includes injuries during takeoff, the flight itself, and landing. Passengers are usually covered, though the policy may set per-passenger limits that cap what any single rider can recover. Per-passenger limits apply regardless of the total policy limit.

If multiple passengers are injured in the same incident, those limits can be reached quickly. Understanding the specific limits on the operator’s policy is one of the first things an attorney will look at after an aviation injury.

If the aircraft itself had a defect, your claim may not stop with the operator. A products liability claim against the aircraft manufacturer is a separate legal pathway, covering injuries caused by a flawed design or a manufacturing error. These two claims can be pursued at the same time.

The commercial general liability policy covers the vertiport premises. If you slip on a wet floor before boarding or are injured during passenger loading, that claim may fall under the premises policy rather than the aviation policy. Some commercial general liability policies contain aviation exclusions, which means a ground-side injury near the aircraft might not be covered by either policy without the right endorsements in place.

Ground transportation creates a third layer. If a shuttle van transporting you to a vertiport off Loop 610 in Houston is involved in a crash, that is an auto liability claim, not aviation. Operators who provide ground transportation need separate auto coverage aligned with their passenger operations.

Where the Gaps Create Problems

The most common coverage disputes arise when an incident crosses policy boundaries. Consider a passenger who slips on a wet vertiport floor before boarding. The aviation policy may exclude the claim because the aircraft was not in operation. The commercial general liability policy may exclude aviation-related incidents. The right coverage depends entirely on how the policies are written and coordinated.

These layered disputes are similar to what injured passengers face in rideshare accidents, where multiple insurance phases and parties create disagreements over which coverage applies first.

Does Texas Require eVTOL Operators to Carry Insurance?

Texas does not impose a single statewide insurance mandate for aircraft. Requirements flow from federal commercial operating rules, airport and vertiport agreements, and lender contracts.

Texas Transportation Code Chapter 21 addresses Advanced Air Mobility infrastructure in the state, which affects how cities and local authorities structure operating permits. Those permit terms almost always include insurance requirements as a condition of access. A Texas operator cannot realistically run commercial passenger service without satisfying multiple insurance obligations, even without a single state mandate requiring it.

The result for passengers is that coverage exists. The complexity is in knowing which policy applies to your specific situation.

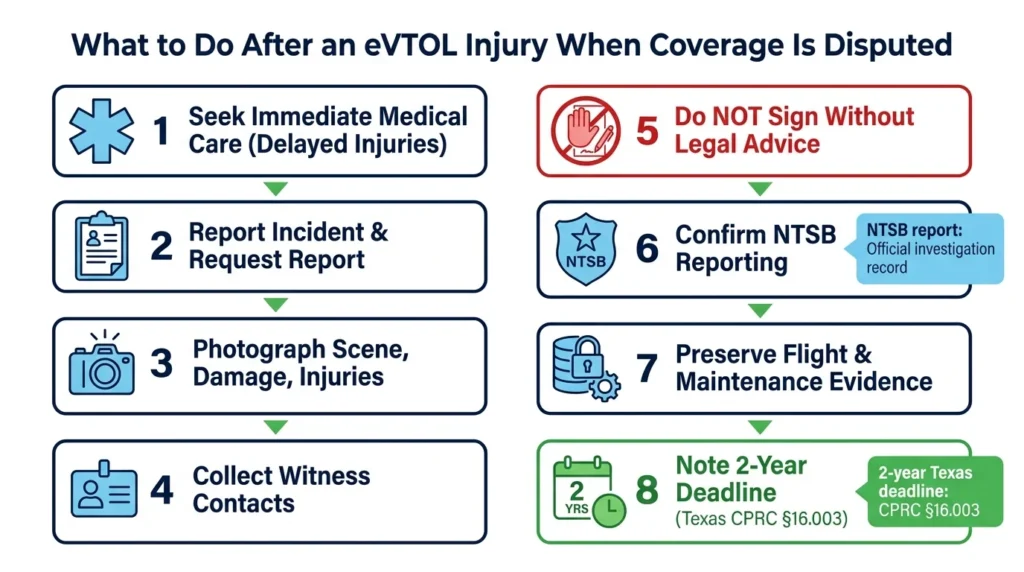

What to Do If You Are Injured & Coverage Is Disputed

If you are hurt during an air taxi trip and the operator or their insurer disputes which policy covers your claim, the steps that protect a car accident claim apply here too, with a few additions.

- Seek medical attention immediately. Aviation incidents can cause delayed-onset injuries.

- Report the incident to the operator and vertiport staff and ask for a written incident report.

- Photograph the aircraft, the vertiport, any visible damage, and your injuries.

- Get the names and contact information of witnesses.

- Do not sign any documents from the operator or their insurer before speaking with an attorney.

Federal law requires operators to report aviation accidents to the National Transportation Safety Board (NTSB). That report becomes part of the official investigation record and is often critical evidence in coverage disputes and injury claims.

Texas law gives you two years from the date of injury to file a personal injury lawsuit under Texas Civil Practice and Remedies Code § 16.003. Evidence from flight data systems and maintenance records needs to be preserved well before that deadline.

How Angel Reyes & Associates Can Help

Multi-policy aviation claims require identifying which coverage responds, preserving specialized evidence, and navigating federal regulatory involvement at the same time. At Angel Reyes & Associates, our personal injury attorneys have guided injured Texans through complex, multi-party cases for over 30 years. Learn more about our firm and our approach.

We offer free consultations and work on contingency, meaning no fee unless we win. Contact our team today to talk through what happened and understand your options. Every case is different.

Electric Air Taxi Insurance FAQs

What Is the Difference Between Aviation Liability & a Vertiport Premises Claim?

Aviation liability covers injuries that occur during flight operations, while a premises claim covers injuries caused by unsafe conditions at the vertiport facility itself. Which policy applies depends on exactly where and how the injury occurred.

Can an eVTOL Operator's Insurance Deny My Claim if I Was Partly at Fault?

Texas follows a modified comparative fault rule, meaning your compensation is reduced by your percentage of fault but you can still recover as long as you are 51% or less responsible. Insurers will look for ways to assign fault to you, which is why preserving evidence early matters.

Do Federal Minimum Insurance Requirements Protect Passengers Adequately?

Federal minimums under 14 C.F.R. Part 205 set a floor, not a ceiling. Major Texas metro operators typically carry significantly higher limits under their vertiport and operating agreements, but the adequacy of any specific policy depends on the limits written into it.

What Happens if the Shuttle Van Taking Me to the Vertiport Is in an Accident?

Ground transportation injuries fall under auto liability coverage, not aviation liability. If the operator provides the shuttle, their auto policy responds. If it is a third-party vendor, that vendor’s coverage applies, and you may need to pursue a claim against them separately.

Does eVTOL Insurance Cover Luggage or Personal Property Damaged During a Flight?

Aviation liability policies focus on bodily injury. Damage to personal property may be excluded or subject to separate limits. Passengers should check the operator’s terms of service and consider whether their own renters or homeowners policy covers personal property in transit.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...