How Multi-Car Insurance Policies Work in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas lets you bundle multiple vehicles under one policy or insure them separately based on your needs

- Most policies block UM/UIM stacking, meaning your payout limit may be lower than you expect after a crash

- Unlisted drivers, missed deadlines, and per-accident limits cause most multi-car claim denials in TX

How Multi-Car Insurance Policies Work in Texas

There are lots of reasons to need to add an additional car to your auto insurance policy. Maybe a teen just got their license, or you bought a truck for weekend hobbies. You can choose to bundle multiple cars under one policy or you can insure them separately. The structure you choose affects your premium, your coverage limits, and how a claim gets paid after a wreck.

The wrong setup can leave you with a denied claim, a coverage gap you didn’t know existed, or a higher premium than necessary. Most people don’t think about this until something goes wrong, by which point they are stuck with the decision they made months ago.

What a Multi-Car Policy Actually Covers

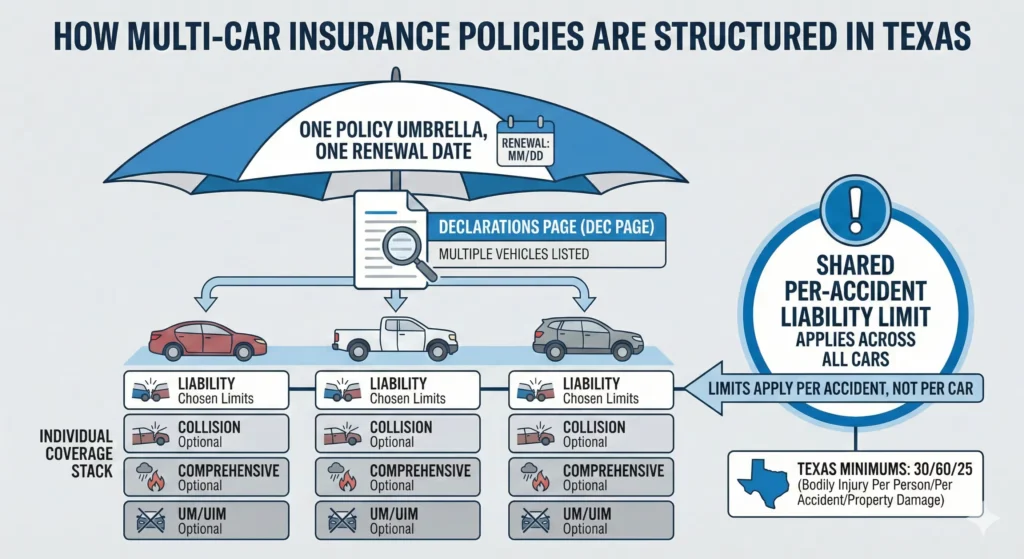

A multi-car insurance policy bundles two or more vehicles under a single contract with one insurer. Each vehicle gets its own coverage selections, and you deal with both one monthly premium and one renewal date.

Every vehicle on the policy must meet Texas’s minimum liability requirements. You can add collision, comprehensive, and UM/UIM coverage to each car individually. The bundled structure means one declarations page lists all vehicles, drivers, and coverage limits.

Your liability limits apply per accident, not per vehicle. If two of your cars are in the same crash on I-35E or LBJ/635, your policy pays up to the stated limit for that single incident. You don’t get double coverage because two vehicles were involved.

Who Qualifies for Multi-Vehicle Coverage

Most insurers require all vehicles on a policy to be registered at the same Texas address. However, they do sometimes allow for a few exceptions.

A teen driver is typically listed on the same policy rather than getting their own.

A college student living away from home can keep their car on your policy without having to live at your address full-time. Even though they primarily live near campus at UT Austin or Texas Tech, they won’t need to purchase their own insurance.

Cars, trucks, and SUVs owned by household members but that primarily operate elsewhere can usually also be included. For example, a Southwest Airlines pilot who lives near Austin but is based out of Dallas Love Field may choose to keep a small, inexpensive car in Dallas to allow them to get around while on a short layover at their operating base.

Finally, vehicles used for commercial purposes, such as operating for delivery or rideshare companies, can sometimes be included, but might also need separate commercial coverage.

Vehicles used for commercial purposes, such as delivery or rideshare, often need separate commercial coverage.

How Bundling Affects Your Premium

Insurers typically offer a multi-car discount when you add a second or third vehicle. Discount amounts vary by insurer, driving history, and the vehicles involved. But bundling generally costs less than insuring each car separately.

For insurers, multi-car policies mean reduced administrative costs. They also assume a household with multiple vehicles is stable and lower-risk.

But bundling doesn’t always mean lower total costs. If one driver in your household has a poor record, their risk gets factored into the entire policy. You might pay less per vehicle but more overall than if you kept that driver separate.

When Separate Policies Make Sense

Some Texas households split coverage across two insurers. This can happen when:

- One spouse has a classic car that needs specialized coverage

- A teen driver’s record would spike the premium for everyone

- One vehicle is financed through a lender that requires a specific insurer

Having two policies on the same car is legal in Texas, but it does add complications. “Double-dipping,” or collecting compensation twice for the same incident is illegal, and insurers share data to try and mitigate this. Duplicate coverage on one car creates problems like fraud claims or claim denials that you likely don’t want to deal with after a wreck.

UM/UIM Coverage Stacking on Multi-Car Policies

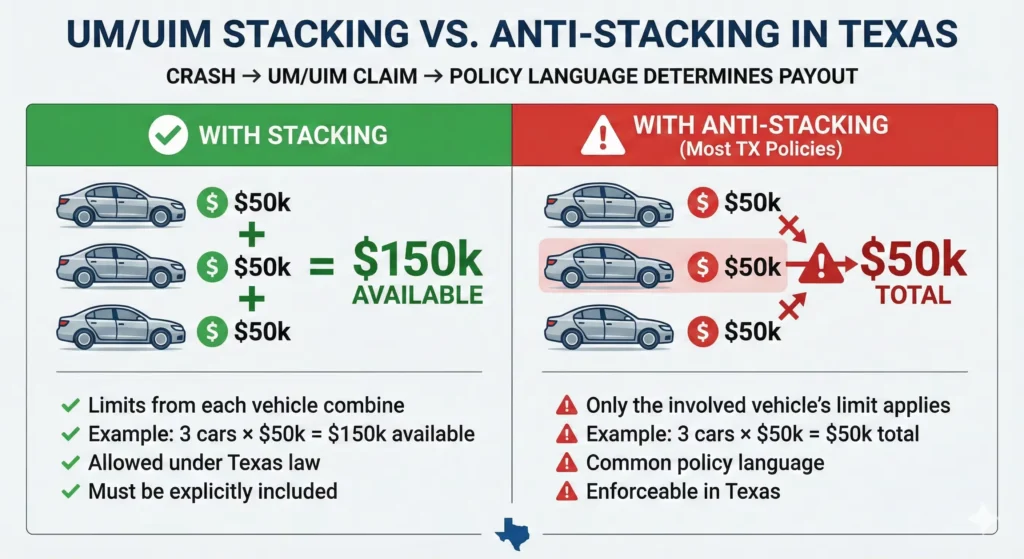

Uninsured and underinsured motorist coverage pays when the at-fault driver has no insurance or not enough to cover your injuries. In rare cases, some Texas policies allow for a practice called “stacking,” which lets you combine the UM/UIM limits from each vehicle on your policy for a single incident.

For example, say you have three cars with $50,000 in UM/UIM coverage each. With stacking, you could access up to $150,000 after a serious crash caused by an uninsured driver. That matters when you’re facing major medical bills.

However, most Texas policies include anti-stacking language. This limits your UM/UIM recovery to the amount on the single vehicle involved in the crash, no matter how many cars you insure.

Check your declarations page for phrases like “limits of liability are not increased” or “coverage applies only to the vehicle involved.” These clauses are enforceable in Texas, and most policies have them.

How to Get Stackable Coverage

If you want stackable UM/UIM coverage, ask your insurer directly. Some offer it for an additional premium. Others don’t offer it at all.

Get written confirmation of whether your current coverage stacks. If your insurer doesn’t offer stacking and you want it, you’ll need to shop around for other carriers.

Common Pitfalls with Multi-Vehicle Coverage

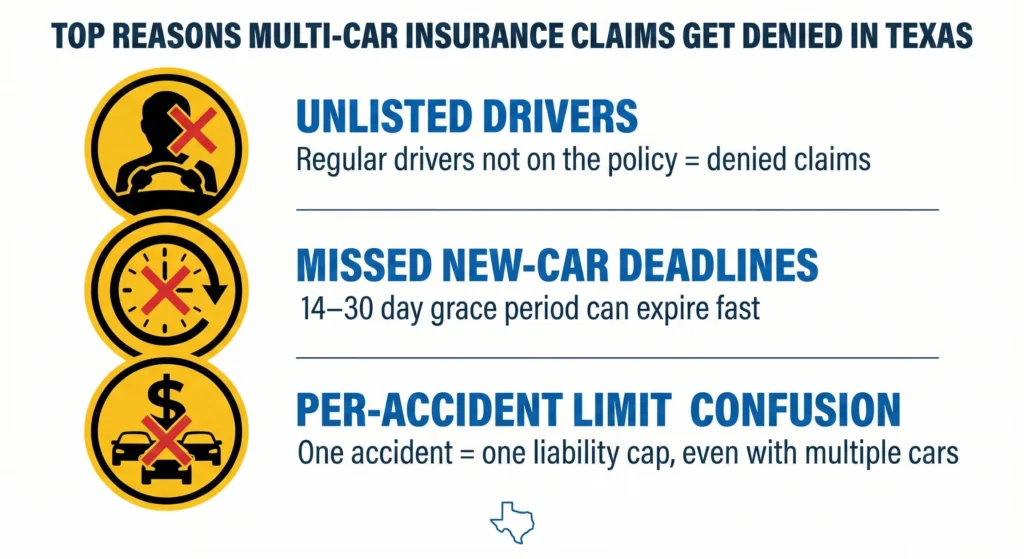

Three problems cause most of the multi-car coverage disputes in Texas. Knowing these ahead of time helps you avoid frustrating gaps.

Unlisted drivers cause claim denials. If your neighbor’s kid borrows your car regularly and isn’t on your policy, the insurer may refuse to pay after an accident. List everyone who drives your vehicles more than occasionally.

Coverage doesn’t automatically transfer to a new car. When you buy a vehicle, most policies give you a grace period of 14 to 30 days to add it. Miss that window, and you’re driving uninsured. Know your grace period before you walk onto a dealer’s lot.

Per-accident limits stay the same in multi-vehicle crashes. Say your policy has $60,000 in bodily injury liability per accident. If both your cars injure someone in the same collision, that $60,000 is the maximum for all injuries combined.

What to Review Before Renewal

Pull out your current policy and check:

- Are all household drivers listed, including teens and frequent borrowers?

- Does each vehicle have the coverage you expect?

- Is your UM/UIM coverage stackable or limited by anti-stacking language?

- Are your liability limits high enough for your assets?

- Do you know your grace period for adding a new vehicle?

If you’re unsure what your policy actually says, call your agent and ask for a plain-English explanation. Get it in writing.

Take Control of Your Coverage Now

Understanding how multi-car insurance works helps you make better decisions for your household and budget. Pull out your policy, check your declarations page, and confirm the details:

- Every driver is listed

- Every vehicle has the coverage you expect

- Every deductible is as expected

If something doesn’t look right, or you’ve been in a crash and your insurer is disputing your coverage despite your policy language, Angel Reyes & Associates can help. We’ve guided Texans through situations like this for over 30 years. Reach out to us for a free consultation to review your options.

Multi-Vehicle Policy FAQs

Can I insure cars at two different Texas addresses under one policy?

Insuring cars at two different addresses under one policy usually isn’t allowed, but there are some exceptions that we discussed here. Ask your insurer to confirm this in writing. A second home or a vehicle kept elsewhere usually needs its own policy.

What if I sell one of my cars mid-policy?

Contact your insurer to remove the vehicle immediately. You’ll typically get a prorated refund for the unused premium. However, you may lose access to certain discounts by dropping to a single-car policy.

Does my multi-car discount disappear if I drop to one vehicle?

Yes. Multi-car discounts require two or more vehicles on the policy. Expect your per-vehicle rate to increase when you remove cars. Always ask your insurer for a quote showing the new premium before you make changes.

Can I switch one car to a different insurer without affecting the others?

Yes. You can insure each vehicle separately if you prefer. Just keep in mind that having two policies on the same car, while technically legal, can lead to claim disputes and fraud accusations, so it’s best to avoid it.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...