Texas Auto Insurance Subrogation Rules Explained

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

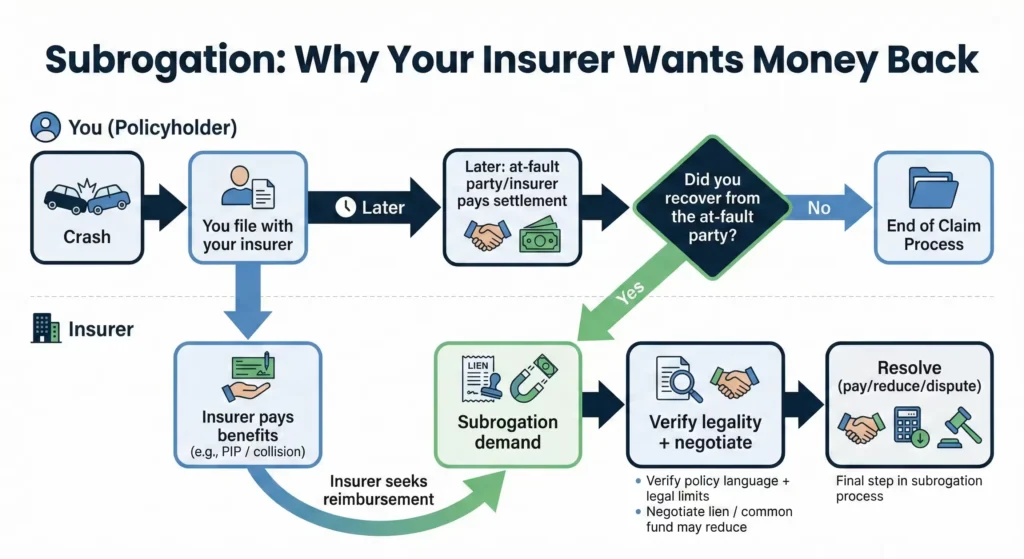

- Subrogation is when your insurer seeks reimbursement after paying your claim, typically once you recover money from the at-fault driver or their insurer.

- Texas limits PIP subrogation under Insurance Code §1952.155, and your policy must include clear subrogation language for a demand to be valid.

- Protect your settlement by requesting the full policy, identifying liens early, understanding your total damages, and negotiating subrogation demands before you sign.

Texas Auto Insurance Subrogation Rules Explained

You file a claim with your own insurer after a wreck on I-35, they cut you a check, and now, after some time has passed, they are demanding all or part of the money they paid you back. Why? The short answer: this is a process known as subrogation. Under Texas Insurance Code §1952.155, your insurer may have the right to recover what they paid you once you collect from the at-fault party in an accident.

For someone juggling work, medical appointments, and bills after a crash, this adds another layer of complexity. Knowing the rules helps you plan before you sign any settlement paperwork.

What Is Subrogation in Texas Auto Claims?

Subrogation is your insurer’s legal right to step into your shoes and seek reimbursement from whoever caused your accident. If you file a claim with your own insurance policy and they pay your claim in accordance with your policy limits, they can pursue the at-fault driver or their insurer to get that money back.

This matters because the money your insurance company pays you initially comes out of your eventual settlement later. For example, if you recover $50,000 from the other driver but your insurer paid $15,000 in PIP benefits before then, your insurer may claim part of what you collected.

How Texas Law Limits Subrogation

Texas law restricts when insurers can pursue subrogation for Personal Injury Protection benefits. PIP coverage pays your medical expenses and lost wages regardless of who caused the accident or any other insurance policies you may have (including health insurance).

Under Texas Insurance Code §1952.155, subrogation for PIP claims is only allowed when the other driver involved in the accident either does not have insurance or does not have proper documentation of their insurance at the time of the accident.

In other words, if you are involved in an accident with a driver who is uninsured or does not have proper insurance documentation, then you can still file a PIP claim with your insurer, but they may be able to recover what they paid you later through subrogation after you receive a settlement from the other party or their insurer.

Your policy must contain explicit subrogation language, and the insurer must follow the procedures outlined in the law. If your PIP policy lacks proper subrogation provisions, your insurer may have no right to recover those payments from your settlement.

Review your declarations page and policy terms before assuming your insurer can claim part of your recovery. Many Texans discover their insurer’s subrogation demand has no legal basis once the policy is examined.

When Insurers Can and Cannot Pursue Reimbursement

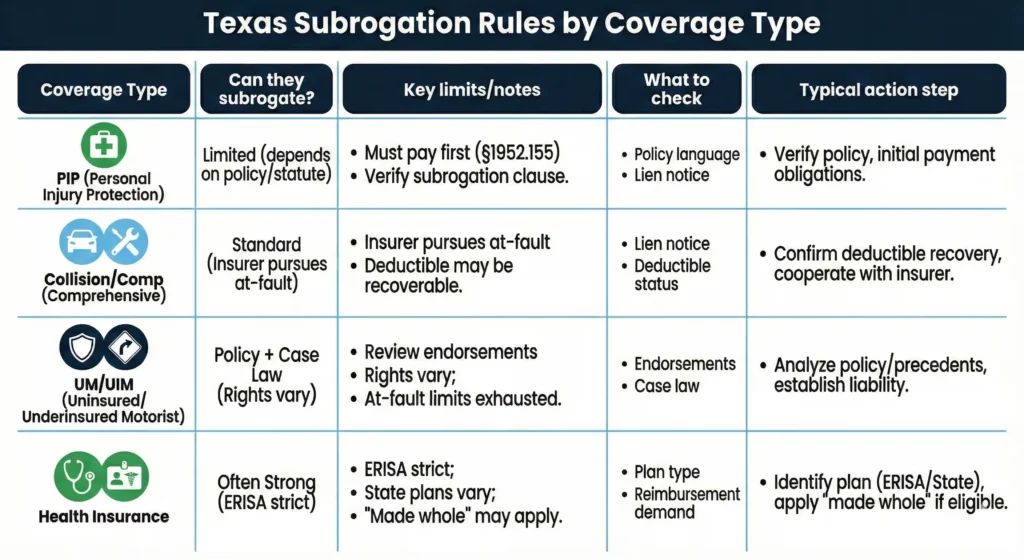

Texas subrogation rules vary by coverage type:

Personal Injury Protection:

- Subrogation allowed only if policy explicitly permits it

- Must comply with §1952.155 requirements

- Cannot reduce benefits based on other insurance you carry

- Collision and Comprehensive Coverage:*

- Standard subrogation rights typically apply

- Insurer can pursue at-fault party after paying your vehicle damage claim

- Your deductible may be recovered if subrogation succeeds

Uninsured/Underinsured Motorist Coverage:

- Subrogation rules are more complex

- UM/UIM claims involve your own insurer paying when the other driver lacks adequate coverage

- Policy language and Texas case law govern recovery rights

Health Insurance Paying Auto Accident Bills:

- ERISA-governed plans often have strong subrogation rights

- Texas state-regulated health plans face more restrictions

- The “made whole” doctrine may limit recovery until you are fully compensated

Each situation requires examining your specific policy and the circumstances of your accident.

Protecting Your Settlement from Subrogation Claims

Take these steps before finalizing any settlement:

- Request your full policy. Get a complete policy document, not just the declarations page. Subrogation clauses are often buried in the fine print.

- Identify all liens early. Ask your attorney to run a lien search. Insurers, medical providers, and government programs may all claim part of your recovery.

- Calculate your total damages. Know what full compensation for your losses looks like before accepting any offer. Subrogation claims will reduce what you keep.

- Negotiate the lien. Many insurers will accept less than the full amount, especially when your recovery does not fully cover your losses.

- Document everything. Keep records of all payments made on your behalf and all communications about reimbursement.

Settling a claim too quickly could mean discovering subrogation claims after the money is gone. A demand letter arriving three months after you deposited your settlement check creates problems that proper planning can help prevent.

When to Get Legal Help with Subrogation Issues

Subrogation disputes can significantly reduce what you take home from a settlement. An attorney can review your policy language, identify invalid claims, and negotiate reductions.

Consider consulting an attorney when:

- Your insurer demands more than seems reasonable

- Multiple parties claim portions of your settlement

- You have ERISA health coverage involved in your accident

- The at-fault driver’s policy limits are low

- You are unsure whether subrogation applies to your PIP benefits

Our attorneys at Angel Reyes & Associates have guided Texans through situations like this for over 30 years. We offer free consultations that can clarify your options and help you understand what you should actually owe. Contact us today to learn more about your options. Past results do not guarantee future outcomes.

Subrogation FAQs

Can my insurer take my entire settlement through subrogation?

Texas law and most policies limit subrogation to the amount the insurer actually paid. They cannot claim more than they spent on your behalf. Attorney fees and costs may also reduce the subrogation amount under the “common fund” doctrine.

What happens if I ignore a subrogation demand?

Ignoring valid subrogation claims can lead to lawsuits, damaged credit, or complications with future insurance coverage. Address demands promptly, but always verify they are legally valid before paying.

Does the "made whole" doctrine apply in Texas auto cases?

Texas recognizes the made whole doctrine in some contexts, meaning your insurer may need to wait until you are fully compensated before recovering. However, ERISA plans and specific policy language can override this protection. Request a consultation for information specific to your situation.

How do recent law changes affect my subrogation rights?

Legislative updates, including amendments effective in recent years, have clarified insurer obligations and policyholder protections. The specific impact depends on your policy’s effective date and the coverage type involved. An attorney can review how current law applies to your claim.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...