What if Your Car Is Totaled but You Still Owe Money? A Texas Gap Insurance & Loan-Payoff Guide

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Insurance pays the actual cash value of your vehicle to the lienholder first, and you may owe a deficiency balance if your loan exceeds the payout.

- Gap insurance can cover the shortfall, but caps and exclusions vary, so verify coverage through your policy or loan paperwork.

- Take smart steps after a total loss: gather documents, review the insurer valuation, file a gap claim, and explore payoff or legal options.

What if Your Car Is Totaled but You Still Owe Money?

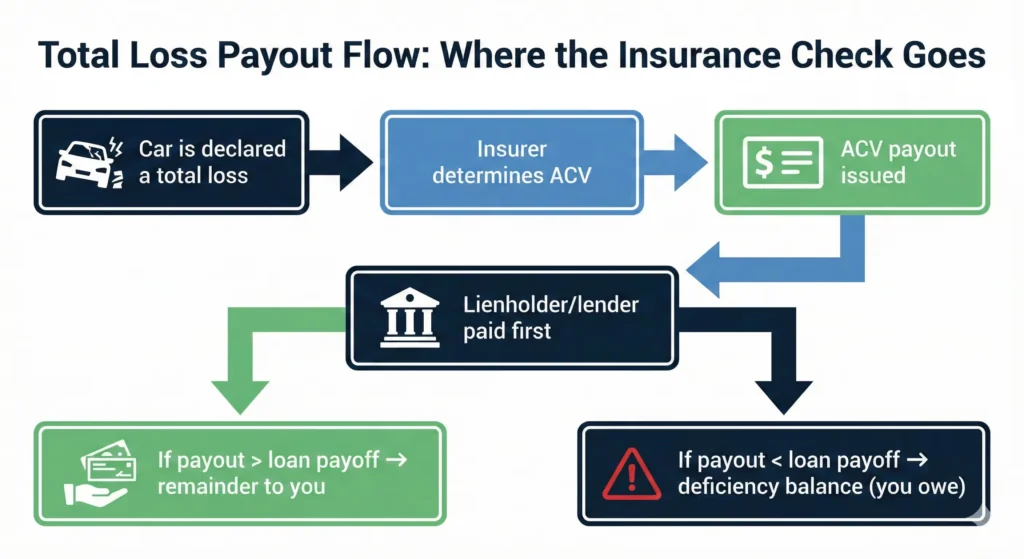

You just got the call that your still-very-new car is a total loss after a wreck on I-35. While insurance will cover the actual cash value (ACV) of your vehicle, your loan balance exceeds that value. That loan won’t disappear with the vehicle, leaving you on the hook for more money and still without a car. In Texas, the insurance payout from your accident goes to your lienholder first, and if that check doesn’t cover what you owe, you’re responsible for the difference.

That leftover amount is called a deficiency balance, and can range from a few hundred dollars to several thousand, depending on your loan terms and how much your car has depreciated. Gap insurance exists to cover that shortfall, but not everyone has it, and not every policy works the way you’d expect.

This guide walks you through how auto loans impact total-loss payouts in Texas, how to confirm whether you have gap coverage, and what steps to take if you’re facing a deficiency.

How Insurance Payouts for Totaled Vehicles Work

When the cost to repair your car exceeds its actual value, insurers will typically declare the vehicle as a “total loss.” When this is the case, they pay the actual cash value of the vehicle at the time of the wreck. That value is determined by what your car would have been worth on the open market, not what you paid for it or what you still owe.

If you financed or leased the vehicle, your lender holds a lien on the vehicle. When the insurer pays out for the value of your vehicle, the check goes to the lender first as the lienholder. Whatever remains after the loan payoff, if anything, comes to you.

What happens when the actual cash value of your vehicle is less than your loan balance? In short, you still owe the difference. This is common with newer vehicles, longer loan terms, or low down payments, where depreciation often outpaces your payoff schedule.

Gap Insurance in Texas

Gap insurance covers the difference between what your insurer pays for your vehicle and what you owe on your loan. For example, if your ACV payout is $15,000 but you still owe $19,500 on your loan, gap insurance covers the $4,500 difference. Without it, you’d owe that amount out of pocket while also needing to find another vehicle.

Gap coverage can come from your auto insurer, your lender, or even from a dealership add-on at the time of purchase. While they function essentially identically, the source of this coverage matters because terms, exclusions, and claims processes differ. Insurer-provided gap coverage is typically added to your auto policy for a monthly premium. Lender or dealer gap coverage is often a one-time fee rolled into your loan.

Some common exclusions in gap coverage policies to watch for include:

- Overdue loan payments or late fees at the time of loss.

- Amounts added to the loan for extended warranties, service contracts, or credit insurance.

- Vehicles used for commercial purposes if the policy excludes them.

- Losses that occur after the policy lapses or before it takes effect.

Some gap policies also cap the payout at a certain percentage of the ACV, such as 125% or 150%. If your deficiency exceeds that cap, you’re responsible for the rest.

Texas does not require gap insurance by law, but some lenders require it as a condition of financing, especially for leases or high loan-to-value ratios. If your lender didn’t require it and you didn’t add it, you may not have it.

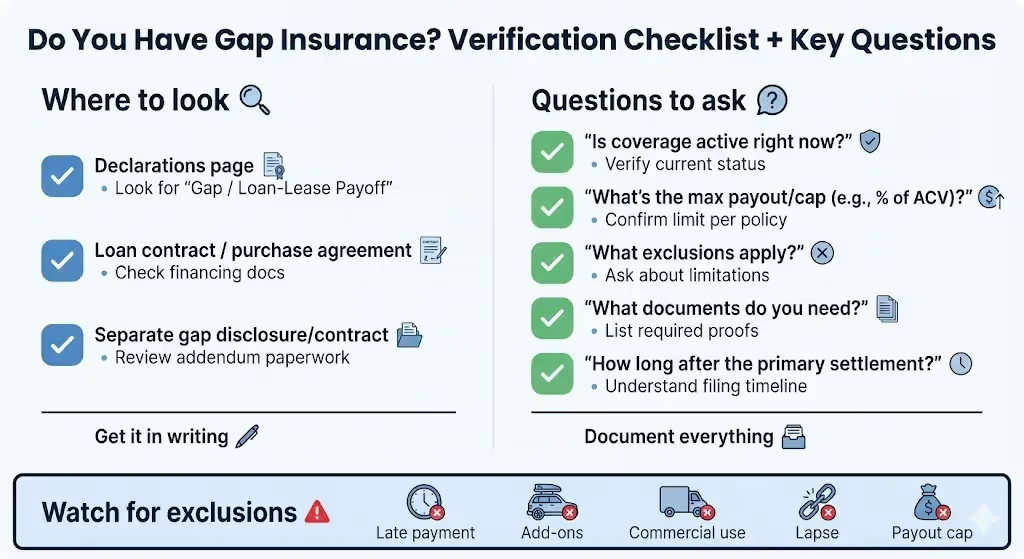

How to Verify Gap Coverage

Start with your auto insurance declarations page: look for a line item labeled “gap coverage,” “loan/lease payoff coverage,” or similar. If you don’t see it, call your insurer and ask directly.

If you purchased gap coverage through the dealership or lender, check your loan documents or the purchase agreement. There should be a separate disclosure or contract for the gap product.

If you have to reach out to your insurer or lender to verify, here are some questions to ask them:

- Is gap coverage currently active on my policy or loan?

- What is the maximum payout or cap on the gap coverage?

- Are there exclusions that could reduce or eliminate the payout?

- How do I file a gap claim, and what documentation is required?

- How long does the claim process take after the primary insurance settles?

Get answers in writing. If there’s a dispute later, documentation protects you.

Practical Steps After a Total Loss in Texas

Acting quickly after a total loss can help protect your credit and reduce the risk of a lingering deficiency. Here’s what to do.

1. Notify your insurer and lienholder promptly.

Report the accident to your auto insurer and your lender as soon as possible. The insurer will assign an adjuster to assess the damage and determine whether the vehicle is a total loss. Ask your lender for a payoff statement, which will tell you exactly how much you owe on a specific date, including accrued interest.

2. Gather your documents.

Pull together:

- Your auto insurance policy declarations page

- Your loan agreement and any gap insurance contract

- The payoff statement from your lender

- The accident report from the responding officer or your own documentation

- Photos of the vehicle and damage, if available

Having these ready speeds up the claims process and helps you spot discrepancies.

3. Review the insurer’s valuation.

When the insurer sends their payout offer, compare it to similar vehicles in your area. Check listings on dealer sites and private sales as well as vehicle value resources like Kelly Blue Book for cars with comparable year, make, model, mileage, and condition.

If the offer seems low, you can dispute it. Provide evidence of higher comparable sales. Texas insurers must consider your documentation, though they’re not required to match your number.

4. File your gap claim if you have coverage.

Once the primary insurance settlement is finalized, file your gap claim. The gap insurer will need:

- Proof of the primary insurance payout.

- The loan payoff statement.

- The gap policy or contract.

Gap claims can take a few weeks to process. Stay in contact with both the gap insurer and your lender during this time.

5. Evaluate your options.

If you don’t have gap insurance and the payout doesn’t cover your loan, you have a few paths:

- Pay the deficiency directly. If you can afford it, paying off the balance protects your credit and closes the loan.

- Negotiate with your lender. Some lenders will accept a reduced lump sum or set up a payment plan. This isn’t guaranteed, but it’s worth asking.

- Pursue a claim against the at-fault driver. If someone else caused the wreck, you may be able to recover the deficiency as part of a personal injury or property damage claim.

- Consult an attorney. If the insurer undervalued your car, the gap insurer denied your claim, or you’re facing a large deficiency with no clear path forward, legal guidance can help you understand your options.

How We Help

At Angel Reyes & Associates, we guide clients through car accident claims involving total-loss situations, loans, gap coverage, and lender disputes. For over 30 years, we have helped Texans seek compensation for losses suffered in car accidents.

If you’re facing a deficiency balance, a lowball ACV offer, or a denied gap claim, we can review your documents and explain your options. If someone else caused the wreck, we can help you pursue recovery for the full scope of your losses, including the deficiency.

Get a free consultation to review your situation. Every case is different. Past results do not guarantee future outcomes.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...