How Texas Auto Insurance Handles Multi-Vehicle Accidents

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas proportionate responsibility rules can split fault among multiple drivers. If you are more than 50% at fault, your recovery is restricted.

- Per-accident policy limits (often just $60,000 for injuries) must cover all claimants, frequently resulting in reduced offers when multiple people are injured.

- Managing multiple adjusters requires careful organization, consistent factual statements, and thorough documentation to protect your claim.

You were driving home on I-35E through Dallas yesterday when traffic suddenly slowed to a crawl. Before you could react, you felt an impact from behind, followed by another. Now, three insurance companies are calling, asking for your version of events. The driver who hit you has spoken to an adjuster, who is already hinting that you stopped too quickly.

Multi-vehicle accidents create a tangle of overlapping claims, limited coverage, and competing stories. Understanding how Texas insurers sort through these situations can help you protect your claim and avoid costly mistakes.

What Makes Multi-Vehicle Claims in Texas So Complicated?

Chain-reaction rear-ends on the DNT, pileups during icy conditions on I-30, and intersection collisions in Deep Ellum all share a common problem: multiple drivers means multiple versions of what happened.

Each driver’s insurer will investigate the situation independently. Each side will try to blame the other parties to reduce their fault percentage. This creates a domino effect of liability disputes that can drag on for months.

Two issues drive every multi-vehicle claim outcome: (1) who caused the crash (this responsibility is often shared among drivers), and (2) whether the at-fault parties have enough money to pay everyone who was injured. When five people are injured, and the responsible driver carries only the minimum coverage, it becomes difficult to split the payout fairly.

In these instances, you can expect longer timelines than a simple two-car crash. The Texas Department of Insurance outlines claim-handling deadlines, but multi-party investigations take more time. More adjusters need more statements. More injuries require more medical records. More disputed facts mean more back-and-forth.

Who Pays in a Multi-Car Accident in Texas?

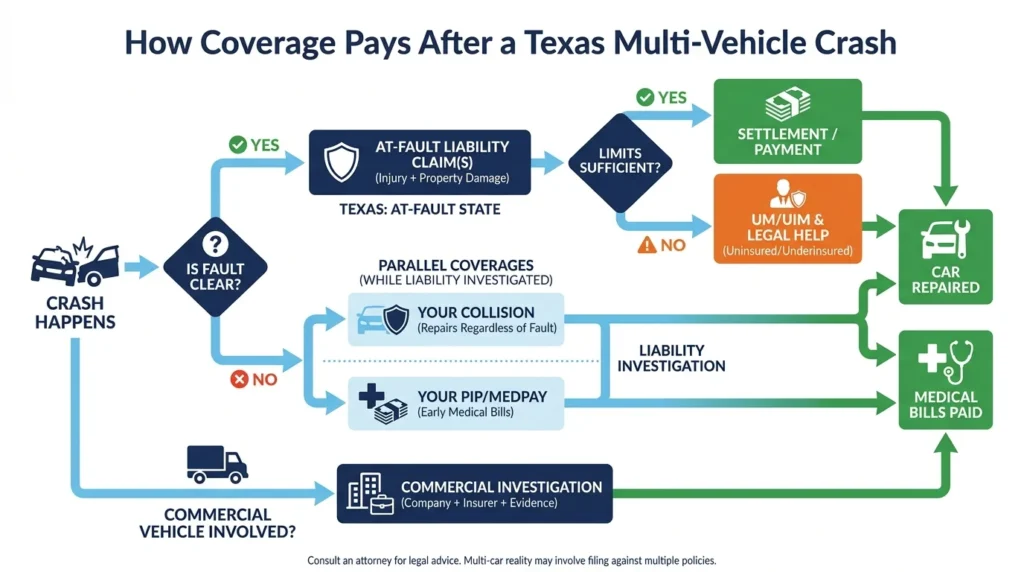

Texas follows an at-fault system. The driver who caused the crash (or their insurer) pays for the others’ damages, but multi-vehicle cases rarely involve just one responsible party.

Several coverage layers may apply to your situation:

- The at-fault driver’s liability insurance pays for your injuries and vehicle damage.

- Your collision coverage repairs your car, regardless of fault.

- Your PIP or MedPay covers immediate medical expenses.

- Your UM/UIM coverage helps pay for your losses when the at-fault driver is uninsured or underinsured.

When fault is split among three drivers, you may need to file claims against multiple liability policies at the same time. Each insurer will calculate their driver’s percentage of responsibility before making any offers.

Commercial vehicles complicate things even more. If a delivery van or 18-wheeler was involved, separate investigations and potentially higher coverage limits come into play. These cases often benefit from experienced legal guidance early in the process.

Chain-Reaction Rear-End Crashes: How Insurers Analyze Fault

The last car in a chain reaction doesn’t automatically pay for everything. Insurers examine each impact separately.

Consider a four-car pileup. The fourth driver rear-ended the third, who was pushed into the second, who hit the first. The fourth driver’s insurer will argue that their driver only caused the final impact. The third driver’s insurer may claim that their driver was a victim, too, as they were only pushed forward by force.

In this case, evidence is critical. Vehicle damage patterns show impact direction and force. Event data recorders capture speed and braking. Dashcam footage can prove whether a driver was already stopped or still moving when they were struck.

Common defenses include sudden stops, unsafe lane changes by other vehicles, mechanical failures, and weather conditions. Your statements about what happened can either support or weaken these arguments. Be sure to stick to the facts you actually observed.

Intersection Multi-Car Wrecks: Why Liability Gets Divided Quickly

Intersection crashes often involve disputes about signal timing and right-of-way. When a third or fourth vehicle gets pulled into the collision, it becomes even harder to figure out who caused the crash.

Insurers consider traffic signal timing, witness accounts, dashcam footage, and police reports. A driver who entered the intersection on a yellow light may share fault with someone who ran a red light. A secondary collision (where the first impact pushes a car into another lane and causes a second impact) creates separate questions about who caused each part of the accident.

Getting a traffic ticket can influence the case, but it doesn’t determine who is legally at fault in a civil claim. You can receive a ticket and still recover damages if the other driver was found to be more at fault.

How Fault Is Determined When Multiple Drivers Are Involved

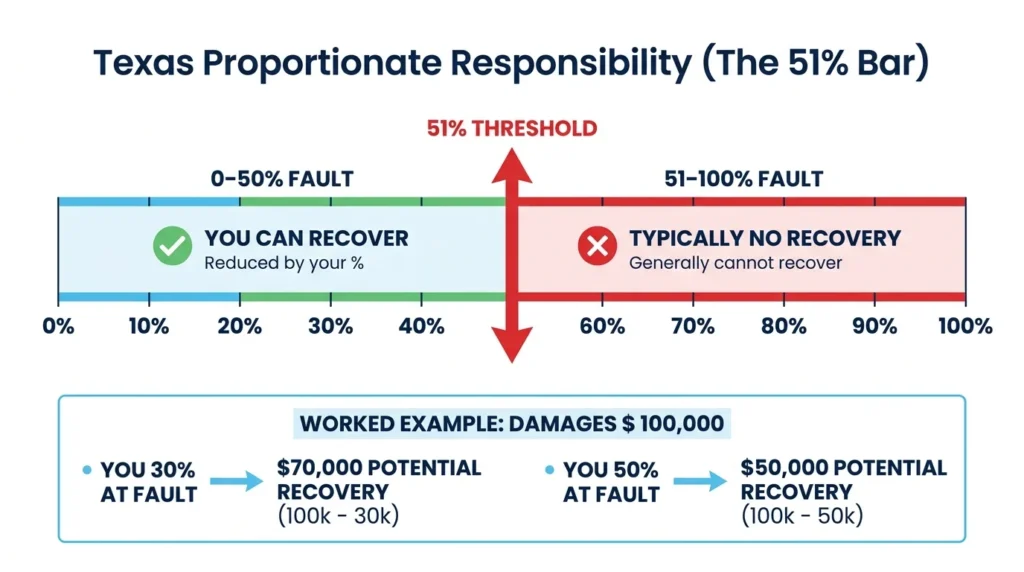

Texas uses proportionate responsibility under Texas Civil Practice and Remedies Code Chapter 33. This means that fault can be divided among all parties, including you.

The 51% bar is critical. This means if you’re found more than 50% responsible for the crash, you generally cannot recover damages from the other drivers. At 50% or below, your recovery is reduced by your fault percentage. If you’re 30% at fault, and your damages total $100,000, you can recover up to $70,000.

Insurers build fault arguments using the following:

- Vehicle damage patterns and measurements

- Event data recorder information

- Photos and video footage from the scene

- Witness statements

- Police crash reports

- Cell phone records (when ordered by the court)

Property damage and bodily injury claims often move at different speeds. Your car may be totaled and paid out within weeks, while injury negotiations may continue for months as your medical treatment progresses.

Why Multi-Car Cases Take Longer to Settle Than Two-Car Crashes

More parties means more waiting. Each insurer will want all statements and medical records before committing to fault percentages. This creates a problem where everyone is waiting for everyone else.

Common delays include disputes over the sequence of the impacts, questions about which collision caused which injuries, and coordination among multiple attorneys when serious injuries are involved. A car accident claim involving four vehicles and three injured parties can easily take twice as long as a straightforward two-car crash.

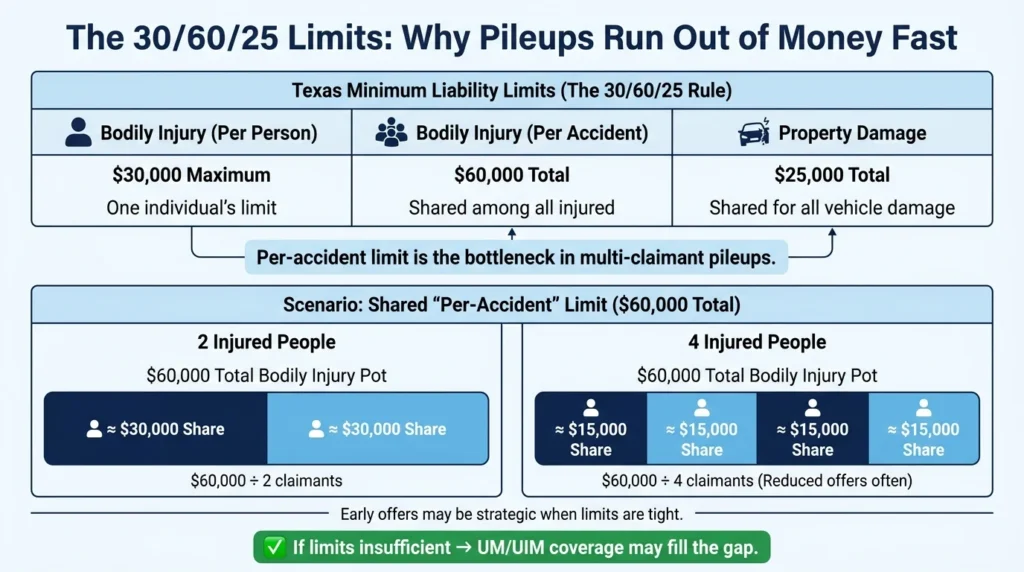

The 30/60/25 Problem: How Per-Accident Limits Cap Payouts

Texas requires minimum liability coverage of $30,000 per injured person, $60,000 per accident for all injuries, and $25,000 for property damage. The Texas Department of Insurance explains these requirements, and Texas Transportation Code Chapter 601 establishes the legal minimums.

The per-accident limit creates the biggest problem in multi-vehicle crashes. If four people are seriously injured, and the at-fault driver carries only minimum coverage, then $60,000 must cover everyone. In this case, even clearly injured claimants may receive reduced offers.

Property damage limits cause similar issues. Three totaled vehicles plus towing and storage fees can easily exceed $25,000. Understanding how towing costs factor into claims can help you track these expenses.

How Insurers Allocate Limited Policies Among Multiple Claimants

When coverage isn’t enough, insurers use different approaches. Some try to settle with claimants individually on a first-come-first-served basis. Others gather all claimants’ information and propose proportional distributions. Others collect information from all claimants and then divide the money fairly among them. Global settlements try to settle all claims at the same time.

Quick, early offers may be strategic. When there are multiple claimants and limited funds, an insurer may offer fast settlements before all injuries are fully understood. Signing too early can harm your claim if symptoms worsen or additional treatment becomes necessary.

When at-fault limits are insufficient, your own underinsured motorist coverage may fill the gap. Review your policy carefully.

UM/UIM Stacking in Texas

People often ask whether they can combine UM/UIM limits across multiple vehicles or policies. The answer depends entirely on your specific policy language.

Stacking means combining coverage limits from different vehicles on one policy or separate policies in the same household. Texas allows some stacking, but insurers often include anti-stacking provisions that limit it.

Request your full policy documents, including declarations pages and UM/UIM endorsements. Ask your adjuster to confirm in writing what limits apply to you. Don’t assume coverage exists unless you have confirmed it.

Managing Multiple Adjusters: A Practical Workflow

Organization can prevent mistakes when dealing with several insurance companies simultaneously.

Create a simple tracking system with claim numbers, adjuster names and contact information, dates of all communications, documents sent, and follow-up dates. This will be your reference guide when adjusters ask conflicting questions or claim that they never received something from you.

Recorded statements require caution. You will likely have to cooperate with your own insurer under your policy, but you are not obligated to speculate or guess for any adjuster. Stick to the facts, such as the direction you were traveling in, what lane you were in, what you observed, and what happened immediately after impact.

Send documentation early to reduce disputes. Make sure to include photos of the scene, dashcam footage, witness contact information, emergency room discharge papers, initial diagnoses, repair estimates, and towing receipts.

What to Say When Fault Is Still Being Investigated

How you phrase things can shape cases in which liability is shared. Avoid apologizing, guessing at speeds or distances, saying “I didn’t see them,” or agreeing to narratives you’re uncertain about.

Keep a symptom log if your pain develops or changes over the first few days. Don’t downplay your injuries during early conversations. What feels minor today may require significant treatment next month.

Texas Claim Timelines & Deadlines

Texas Insurance Code Chapter 542 establishes prompt payment requirements, primarily for first-party coverages like PIP, UM/UIM, and collision. Third-party liability claims (against the other driver’s insurance) follow different timelines.

Multi-party investigations take longer, but you can still track progress. Confirm requests in writing. Document what each adjuster says they need. Follow up politely but persistently when things seem to be taking too long.

Settlement Pitfalls in Texas Pileups

Early offers in multi-claimant cases are often low. Insurers trying to resolve claims within per-accident limits may pressure quick settlements before the full picture emerges.

Money you owe to health insurers and medical providers (called “medical liens”) can reduce how much settlement money you get to keep. A $50,000 settlement could end up being much less after these payments are taken out. It’s important that you understand these deductions before accepting any offer.

Be cautious about signing broad release forms. Settling property damage separately from injury claims can affect your ability to negotiate and prove your case. Each situation is different, but understanding what you are signing can help protect your interests.

What to Do If the At-Fault Driver’s Insurance Isn’t Enough

When the at-fault driver’s limits are too low, you should explore other options, such as:

- Other at-fault drivers’ liability policies (if fault is shared)

- Your own UM/UIM coverage

- Your collision coverage for vehicle repairs

- Other potentially responsible parties (such as commercial vehicle owners and employers)

The percentage of fault assigned to each claimant affects how much money can be recovered from each insurance source. Detailed documentation of medical treatment, lost wages, and the timeline of how your injuries have affected you can strengthen your claim.

When to Talk to a Lawyer

Not every fender-bender requires legal help, but multi-vehicle crashes often involve complications that will be easier to handle with an organized, coordinated approach.

Consider consulting an attorney if you’re dealing with serious injuries, multiple injured parties, disputed fault, problems with policy limits, UM/UIM disputes, commercial vehicles, or inconsistent messages from adjusters.

An attorney can help gather and protect evidence, manage communication with multiple insurers, argue how fault should be divided, and figure out the best strategy to work within insurance policy limits. With over 30 years of experience and more than $1 billion recovered for clients, Angel Reyes & Associates handles these complex situations regularly.

We offer free consultations, work on contingency (meaning you pay no fee unless we win), and can manage the majority of your case remotely.

Contact us today to discuss your multi-vehicle accident claim.

Multi-Vehicle Accident FAQs

Can you use PIP benefits in Texas even if another driver caused the pileup?

Yes. Personal Injury Protection (PIP) is no-fault coverage, so if you have it, it can usually help pay covered medical bills and some lost income, regardless of who caused the crash.

What if the police report gets the chain of events wrong?

A crash report can influence the claim, but it is not the final word on who is at fault. Photos, dashcam video footage, witness statements, and vehicle damage can still change how insurers evaluate a multi-car wreck.

Can passengers make claims after a multi-vehicle accident in Texas?

Usually, yes. Passengers are often able to bring injury claims against one or more at-fault drivers, depending on how the crash happened, and how fault is divided.

Will a multi-car accident go on your insurance record if you were not at fault?

Yes, it may still appear in your claim history if the crash was reported to insurers. Whether it affects your premium can depend on your insurer’s rules, your driving history, and the facts of the case.

Is there a deadline to file a lawsuit after a Texas multi-vehicle crash?

Yes. In many Texas injury and property-damage cases, the general deadline is two years from the accident date, but exceptions can apply. Waiting too long can also make evidence harder to preserve in a complex multi-vehicle accident.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...