Commercial Policy Limits in Texas Truck Accidents

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Commercial truck policy limits in Texas depend on whether the carrier operates interstate or intrastate, plus the truck’s weight and cargo type.

- Serious truck accident damages can exceed minimum insurance limits, making excess coverage, umbrella policies, and other liable parties important.

- Trucking companies may not disclose all available coverage upfront, so FMCSA filings, Texas records, and litigation discovery can reveal additional policies.

When a commercial truck hits your car on I-35W near Fort Worth, the first question that follows the crash is not about fault but about money. Specifically, how much insurance the trucking company carries and whether that coverage is enough to pay for what you have lost.

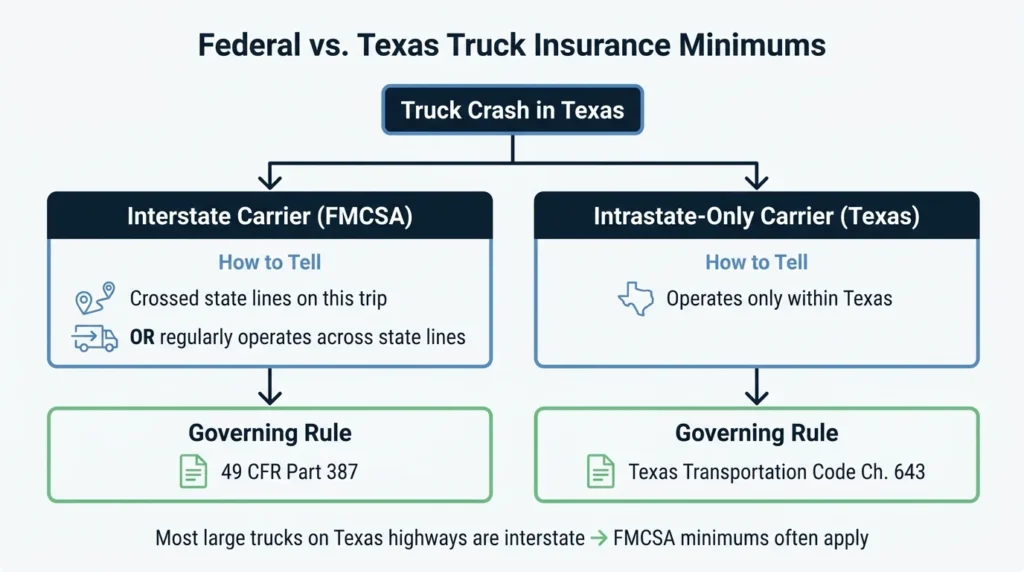

Federal vs. State Minimum Requirements

Commercial trucks in Texas operate under two overlapping sets of coverage rules: Federal Motor Carrier Safety Administration (FMCSA) requirements for interstate carriers and Texas requirements for carriers that operate only within the state. You need to know which set applies to determine the minimum coverage for your case.

Commercial trucks that cross state lines must comply with 49 CFR, Part 387, the federal regulation that defines the minimum financial responsibility for commercial motor carriers. Carriers that operate only within the state fall under Texas Transportation Code Chapter 643, which sets separate requirements tied to vehicle weight and cargo type.

In practice, most large commercial trucks on Texas highways are interstate carriers subject to federal minimum-coverage rules. If the truck that hit you crossed a state line during that trip or regularly operates across state lines, FMCSA minimums apply. For a complete explanation of how Texas-specific commercial truck insurance works, see our blog on Commercial Truck Insurance Requirements.

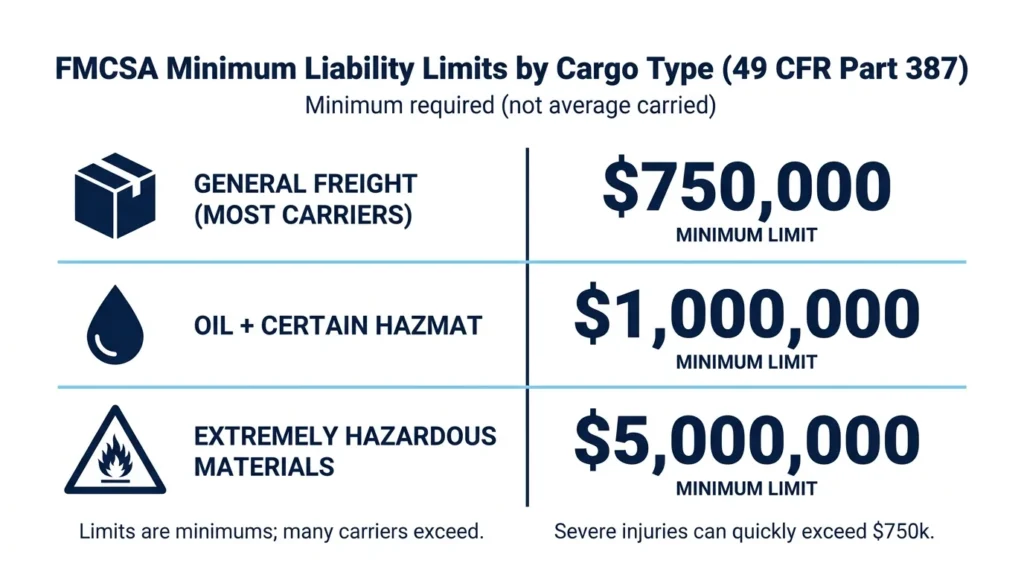

How Cargo Type Changes Policy Limits

Federal minimum limits are not a single number. Under 49 CFR, Part 387, the minimum required coverage rises with the risk of what a truck is hauling:

- $750,000 for most property carriers hauling general freight

- $1 million for carriers hauling oil and certain hazardous materials

- $5 million for carriers hauling certain extremely hazardous materials

Many carriers have significantly more liability coverage, particularly those operating under contracts with large shippers that require higher limits. A truck hauling a common load may carry only $750,000, but a tanker truck carrying petroleum products must carry at least $1 million.

This distinction matters because damages in serious truck accidents often reach or exceed the $750,000 minimum requirement. Broken bones, traumatic brain injuries, and spinal cord injuries quickly generate medical costs in the hundreds of thousands. Understanding the cargo-based limit gives you a starting point for evaluating how far the primary coverage can go. For a closer look at how truck accident claims differ from standard car accident claims, see our explainer of Truck vs. Car Accidents.

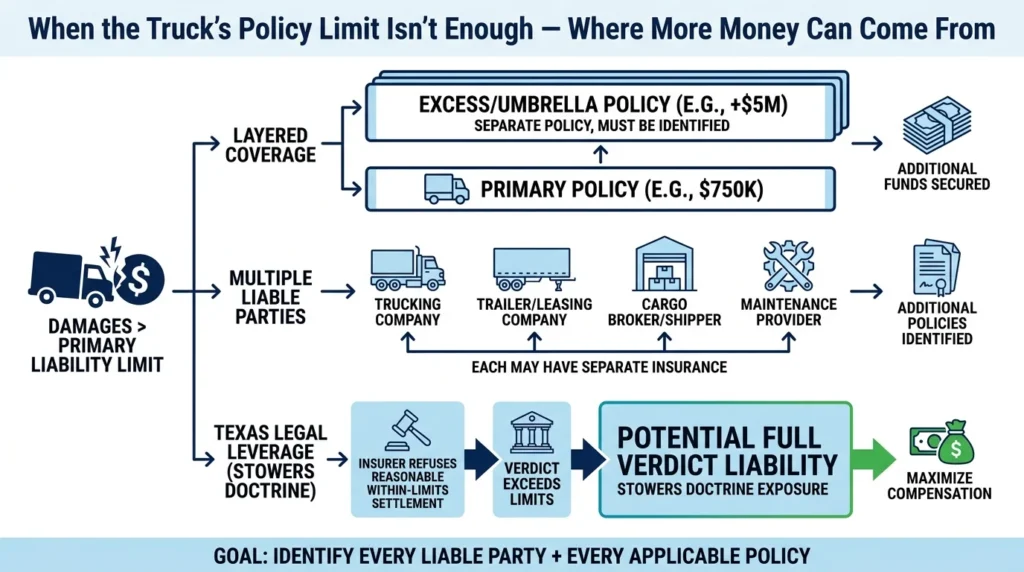

When Truck Policy Limits Fall Short

When your damages exceed the primary-policy limit, other coverage sources and parties may be available to compensate you for the shortfall.

First, many larger commercial trucking companies carry excess or umbrella insurance that kicks in after the primary policy is exhausted. A $750,000 primary policy with a $5 million umbrella provides a much larger pool of funds for damages. The umbrella policy is separate from the primary insurer and must be identified independently.

Second, truck accident liability frequently extends beyond the driver. The trucking company, a leasing company that owns the trailer, a cargo broker, and a maintenance provider all may carry their own policy, and each party may share blame. Every liable party brings their coverage into the equation.

Third, if a commercial carrier’s insurer refuses to settle a reasonable claim within policy limits and a jury later awards more money, then, under Texas’s Stowers Doctrine, the insurer may be ordered to pay the full verdict amount, even beyond the policy cap. Thus, state law gives insurers a strong incentive to settle reasonable claims within limits, but the claimant needs to apply pressure strategically.

One factor that complicates claims against trucking insurers is the speed and aggression of their defense. For a closer look at how trucking companies and insurers delay and deny serious claims see our article on How Trucking Companies and Insurers Delay and Deny Claims in Texas.

How to Find a Carrier’s Coverage

Trucking companies don’t always disclose their full insurance picture voluntarily. There are three ways to identify the available sources of money to fund your claim.

Interstate carriers are required to file proof of insurance with the FMCSA. Their insurance information is publicly accessible on the agency’s Safety and Fitness Electronic Records (SAFER) database, which can be searched by carrier name or USDOT number. The MCS-90 endorsement that appears on most interstate carrier policies is a federal government guarantee that the trucking company’s insurer will provide minimum coverage to pay injured victims even if the policy excludes the type of load or trip.

Texas intrastate carriers must file evidence of insurance with the Texas Department of Motor Vehicles. That filing is a matter of public record.

In litigation, during formal discovery, the trucking company must disclose all applicable policies, including excess and umbrella coverage. You can send a preservation letter to the company immediately after the crash directing officials to preserve any evidence, like maintenance logs and driver records, that could be used in litigation of your case.

For context on what settlements have looked like in truck accident cases similar to yours, check out the average payout for an 18-wheeler accident in Texas.

Work with a Texas Truck Accident Lawyer

Commercial truck accident claims involve federal regulations, layered insurance policies, and defense teams retained the moment a crash is reported. Angel Reyes & Associates has handled truck accident cases across Texas for over 30 years. The firm has recovered more than $1 billion for clients. Past results do not guarantee future outcomes.

We work on contingency, meaning we receive no fee unless we win, so it costs you nothing to have our attorneys review your case. If you were seriously hurt in a truck accident, our team of Texas injury attorneys can tell you whether the number on the table reflects what your case is actually worth. Contact us today for a free consultation before you sign anything.

Commercial Truck Accident FAQs

Does a truck owner-operator need their own insurance even if they lease to a carrier?

Owner-operators leased to a carrier and operating under the carrier’s USDOT authority are typically covered by the carrier’s policy while on a trip. When driving for personal use or between loads without the carrier’s authority, they need their own non-trucking liability coverage, which is also called bobtail insurance.

How long do I have to file a truck accident lawsuit in Texas?

Texas gives personal injury victims two years from the date of the crash to file a lawsuit. Claims against a government entity may have a shorter notice deadline. Missing the filing deadline typically eliminates your right to recover.

Does the trucking company’s cargo insurance cover my injuries?

Cargo insurance covers the goods the truck was hauling, not injury to other drivers. It is separate from the liability policy that compensates crash victims. Cargo insurance proceeds go to the shipper or cargo owner, not to injured motorists.

Can I make a claim directly against the trucking company’s insurer without going through my own insurance?

Yes. When a commercial truck is at fault, injured victims can file a third-party liability claim directly against the trucking company’s insurer without involving their own carrier. Your own insurer may still be notified of the accident, but you are not required to route your claim through your own policy first.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...