Texas Minimum Car Insurance Requirements Explained

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas law requires 30/60/25 liability coverage: $30K/$60K for injuries, $25K for property damage.

- State minimums often fall short—a totaled truck alone can leave you owing $23,000+ out of pocket.

- UM/UIM and PIP protect you when the other driver has no insurance or not enough to cover your losses.

Texas Minimum Car Insurance Requirements Explained

You just renewed your registration at the Dallas County Tax Office and realized your liability limits haven’t changed since you bought your first car. That might be a problem if those limits are no longer compliant with Texas’s minimum insurance requirements.

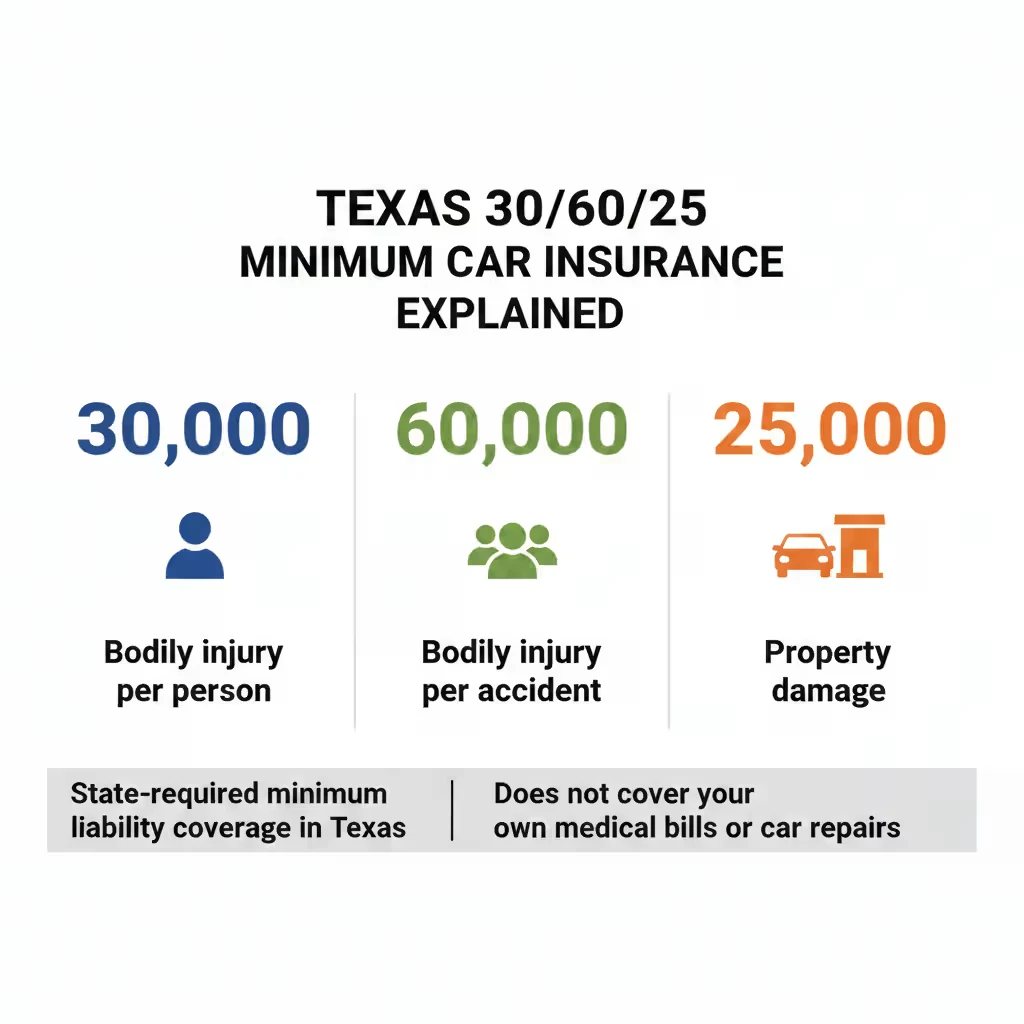

Texas law requires at least 30/60/25 liability coverage on every vehicle you drive. That shorthand might look confusing, but it’s pretty easy to understand when you know what each of these numbers represents. And that’s a good thing because each can have a significant impact on your case should you be involved in an accident.

What Are the Texas Minimum Car Insurance Requirements?

Texas Transportation Code § 601.072 requires every driver to carry a minimum amount of liability insurance before operating a vehicle on public roads. As we stated earlier, this minimum is 30/60/25, which breaks down into three separate limits:

- $30,000 is the most your policy pays for bodily injury to one person in a crash you cause.

- $60,000 is the total your policy pays for bodily injury when multiple people are hurt in the same crash. If three people are injured, the combined payout caps at $60,000, regardless of individual claims.

$25,000 is the limit for property damage you cause. This covers the other driver’s vehicle, fences, buildings, or anything else you hit.

These limits apply only to the other party’s losses. Your own injuries and vehicle damage require separate coverage types.

| Coverage Type | Per Person | Per Accident |

|---|---|---|

| Bodily Injury | $30,000 | $60,000 |

| Property Damage | — | $25,000 |

Typical Scenarios Where Minimums Fall Short

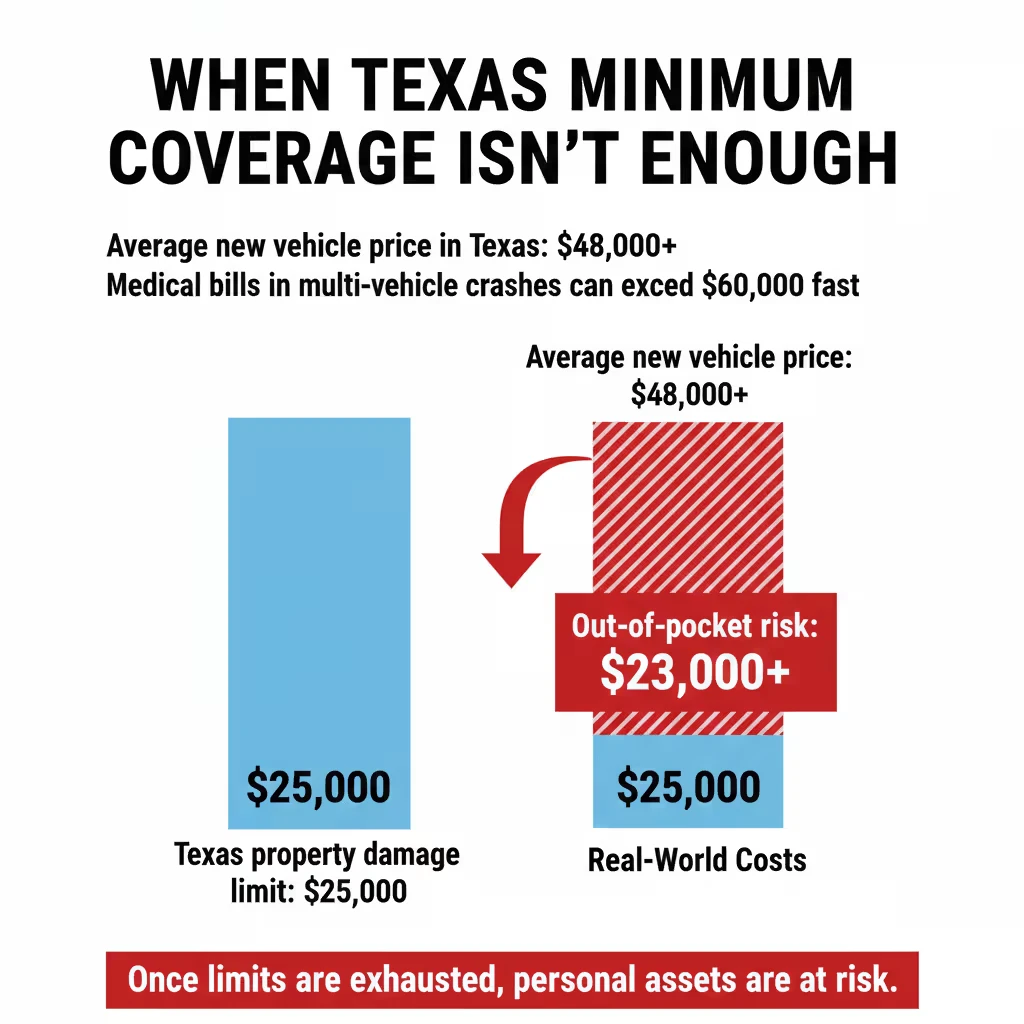

A rear-end collision on LBJ/635 during evening rush hour can involve multiple vehicles. If you cause a three-car pileup and two people need surgery, medical bills can exceed $60,000 before anyone leaves the hospital.

The average new vehicle in Texas costs over $48,000. If you total someone’s truck with only $25,000 in coverage, you would owe the remaining $23,000+ out of pocket. Multi-vehicle crashes and severe injuries expose the vast gap between state minimums and real-world costs. When your policy maxes out, the injured party can pursue your personal assets for the remainder.

Should You Buy More Coverage?

Many Texas drivers carry only the state minimum for the simple reason that it costs less each month. However, these lower premiums come with higher risk if you cause a serious crash.

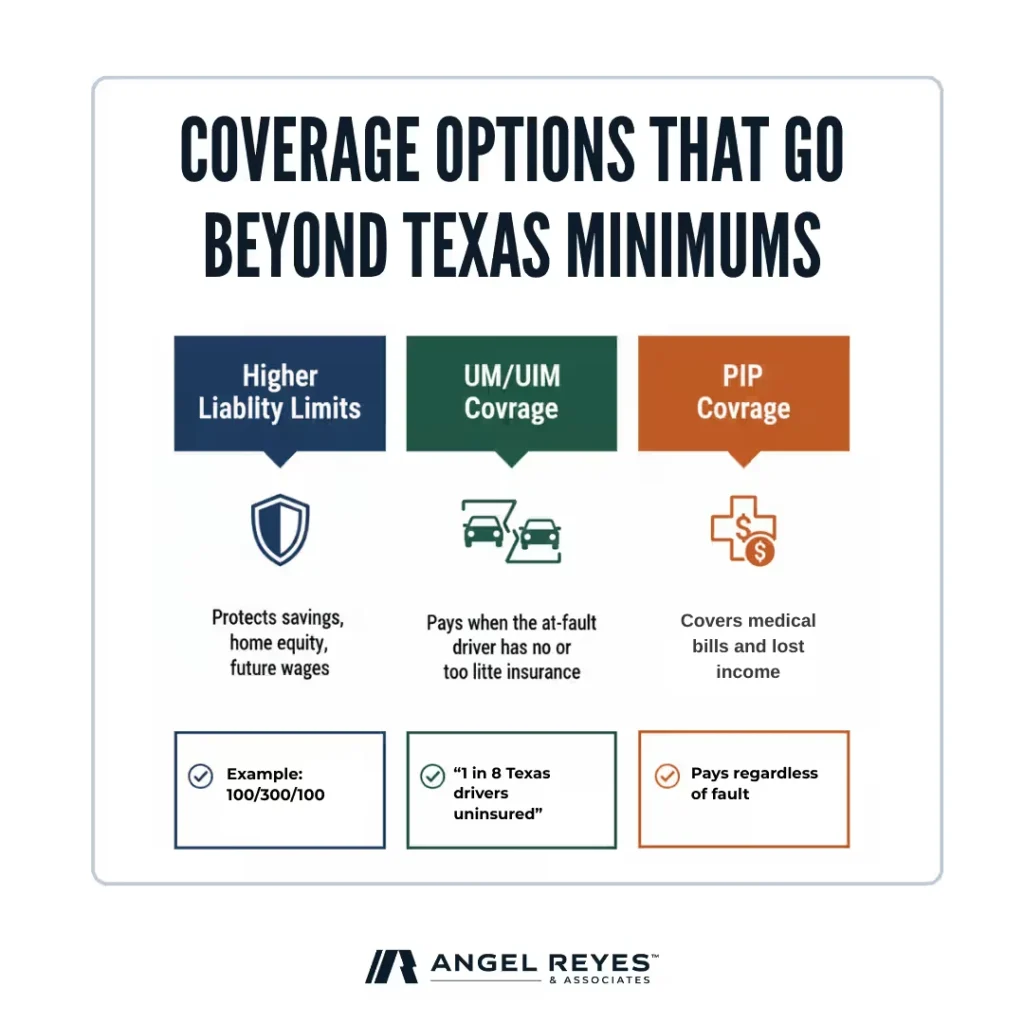

Higher liability limits protect your savings, home equity, and future wages from lawsuits. The cost difference between 30/60/25 liability limits and 100/300/100 is often less than $30 per month, depending on your driving record and location. If you own a home in the DFW area or have significant savings, minimum coverage may leave those assets vulnerable. A judgment against you can follow you for years.

UM/UIM and PIP Coverage

Higher liability limits protect you from lawsuits when you’re at fault. But what happens when the other driver is the one without enough coverage? Uninsured/Underinsured Motorist (UM/UIM) coverage pays your medical bills and lost wages when the at-fault driver has no insurance or not enough to cover your losses.

Texas insurers must offer UM/UIM, but you can reject it in writing. Before you decline, consider that roughly one in eight Texas drivers is uninsured, according to the Insurance Research Council (2023).

Personal Injury Protection (PIP) covers your medical expenses and lost income regardless of who caused the crash. It pays quickly, often before fault is determined, which helps if you need treatment right away.

PIP is also offered by default in Texas. You can reject it, but doing so means relying entirely on health insurance or the other driver’s policy for your medical care after a crash.

Learn more about going beyond the minimums to understand how these coverages work together.

TexasSure and Proof of Insurance Basics

Texas uses the TexasSure system to allow insurers to automatically report and verify proper coverage to the state. You still need to carry proof of insurance when you drive, either in the form of a digital copy on your phone or a traditional paper card.

Choosing the Right Limits for You

Your coverage decision should depend on what you own, what you earn, and how much risk you’re comfortable carrying. If you have a mortgage, retirement savings, or a steady income, a lawsuit judgment could reach those assets. Higher limits create a greater buffer between your policy and your personal finances.

Practical Steps to Adjust Coverage

- Review your assets. Add up your home equity, savings, and investments. If the total exceeds your liability limits, you’re exposed.

- Compare premium costs. Request quotes for 50/100/50 and 100/300/100 limits. The monthly difference is often smaller than expected.

- Check lender requirements. Financed or leased vehicles typically require collision and comprehensive coverage, plus higher liability limits than the state minimum. Check your loan or lease agreement before assuming 30/60/25 is enough.

- Consider an umbrella policy. If you have significant assets, an umbrella policy adds another layer of liability protection beyond your auto policy limits.

Need Help After a Crash?

If you’ve been in an accident and aren’t sure whether your coverage is enough, or if the other driver was uninsured, our team at Angel Reyes & Associates can help you understand your options. We’ve guided Texans through insurance and injury claims for over 30 years. Contact us for a free consultation to review your situation.

Proof of Insurance FAQs

Can you be cited for not having proof of insurance, even if you’re insured?

Yes, you can receive a citation for failure to show acceptable proof. If you provide valid documentation to the court, the charge is typically dismissed, but you may still owe court costs.

What happens if TexasSure shows a lapse?

TexasSure tracks whether your policy is active, not just whether you have a card. The Texas Department of Public Safety may send a verification letter if coverage drops. If you can’t prove continuous coverage, you could face fines, license suspension, or vehicle registration holds.

Do I need UM/UIM or PIP in Texas?

UM/UIM and PIP aren’t legally required, but Texas insurers must offer both. You can reject them in writing. See UM, UIM, and PIP Insurance Coverage Explained for details.

Will my lender require higher coverage?

Most lenders and leasing companies do require liability coverage above the state minimum in addition to collision and comprehensive coverage. Check your financing or lease agreement for specifics.

How can I verify my coverage in Texas?

You can verify your coverage by reviewing your declarations page, which lists your current limits. The state uses TexasSure to verify coverage electronically, but you should keep a copy of your insurance card accessible.

What happens if I drive uninsured in Texas?

First offense fines range from $175 to $350. Repeat violations can result in higher fines, license suspension, vehicle impoundment, and SR-22 filing requirements. You’re also personally liable for any damages you cause.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...