Why So Many Trucking Companies Use Shell Insurance Entities

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Large trucking companies use self-insured retentions, captive insurers, and layered coverage that can make resolving a case difficult.

- FMCSA filings show minimum compliance but rarely reveal the full "tower" of coverage available after a serious crash.

- Identifying all insurance layers and responsible parties early helps crash victims avoid gaps in recovery.

You were hit by an 18-wheeler on I-35W near downtown Fort Worth last week. The trucking company’s adjuster called within 48 hours. They mentioned an insurance company you’ve never heard of and made an offer that barely covers your medical bills so far. When you asked about the policy limits, the answer was vague.

This confusion isn’t accidental. Large trucking companies use sophisticated insurance structures that can make it difficult to identify who actually pays your claim. Understanding these arrangements helps you protect your rights and set realistic expectations for your case.

Why Trucking Insurance Can Feel Like a Shell Game

After a serious truck crash, the name on an insurance card rarely tells the whole story. Large carriers and fleets use risk-financing structures that separate “who is responsible” from “who is insured” from “who actually writes the check.”

A trucking company might be legally liable for your injuries. A captive insurance entity they own might handle the first layer of payment. A completely different excess insurer might cover damages above a certain threshold. Plus, a third-party administrator you’ve never heard of might be the one calling you.

These layered insurance programs exist because they save trucking companies money and give them more control over claims. For crash victims, they create obstacles to identifying coverage, responsible parties, and realistic settlement ranges.

The structures involved include self-insured retentions, layered “tower” coverage, captive insurance companies, fronting arrangements, and risk retention groups. Each affects how your claim gets handled and how long it takes to resolve.

The Baseline: Financial Responsibility Requirements

Before diving into complex structures, it helps to understand what trucking companies must prove to operate legally.

Federal law requires motor carriers to maintain minimum levels of financial responsibility. The FMCSA outlines these requirements and the forms used to demonstrate compliance. For most general freight carriers, the minimum is $750,000 in liability coverage. Carriers hauling hazardous materials may need $1 million or $5 million.

The specific requirements appear in 49 CFR § 387.7, which describes how carriers prove they can pay for injuries and damage they cause. Common proof mechanisms include the MCS-90 endorsement and Form BMC-91.

For trucks operating only within Texas, Texas Transportation Code Chapter 643 sets additional requirements for intrastate motor carriers.

Why Filings Don’t Show the Full Picture

FMCSA filings prove a carrier meets minimum requirements. They don’t reveal the complete insurance structure behind that compliance.

A filing might show a policy from a well-known insurer. What it won’t show is whether that insurer is merely “fronting” for a captive entity, whether there’s a $500,000 self-insured retention the trucking company pays first, or whether multiple excess layers exist above the primary policy.

Many large carriers maintain coverage far exceeding the minimum. A fleet hauling goods on I-30 between Dallas and Fort Worth might carry $5 million or more in total coverage across multiple layers. But early in your claim, you might only hear about one layer from one adjuster.

The person calling you might work for a third-party administrator, not the insurance company itself. They may have limited authority to settle and limited information about the full tower of coverage.

Self-Insured Retentions: The First Layer You’ll Encounter

A self-insured retention is an amount the trucking company pays out of pocket before any insurance dollars kick in. Think of it as a large deductible, but with a critical difference: the trucking company typically controls the claim during the SIR period.

If a carrier has a $250,000 SIR, they’re paying the first $250,000 of any claim themselves. They choose the defense attorneys. They decide investigation strategy. They control whether to settle early or fight.

This creates what attorneys call “claims friction.” When a company is spending its own money, it often:

- Investigates more aggressively

- Demands more documentation

- Makes lower initial offers

- Takes longer to negotiate

For someone recovering from serious injuries after a crash on Loop 820 or the Dallas North Tollway, this means the path to fair compensation may take longer than expected. Preserving evidence early and documenting all damages thoroughly becomes even more important.

Severe Injuries and the SIR Layer

When injuries are catastrophic or multiple people are hurt, the SIR layer still shapes early claim dynamics.

The trucking company’s representatives may push hard for recorded statements, independent medical examinations, and surveillance during the SIR period. They’re trying to minimize what they pay from their own funds.

Discussions about “policy limits” can be premature until you’ve confirmed the full tower of coverage. A $750,000 primary policy might have $4 million in excess coverage above it. Understanding truck accident liability requires knowing all available coverage, not just the first layer mentioned.

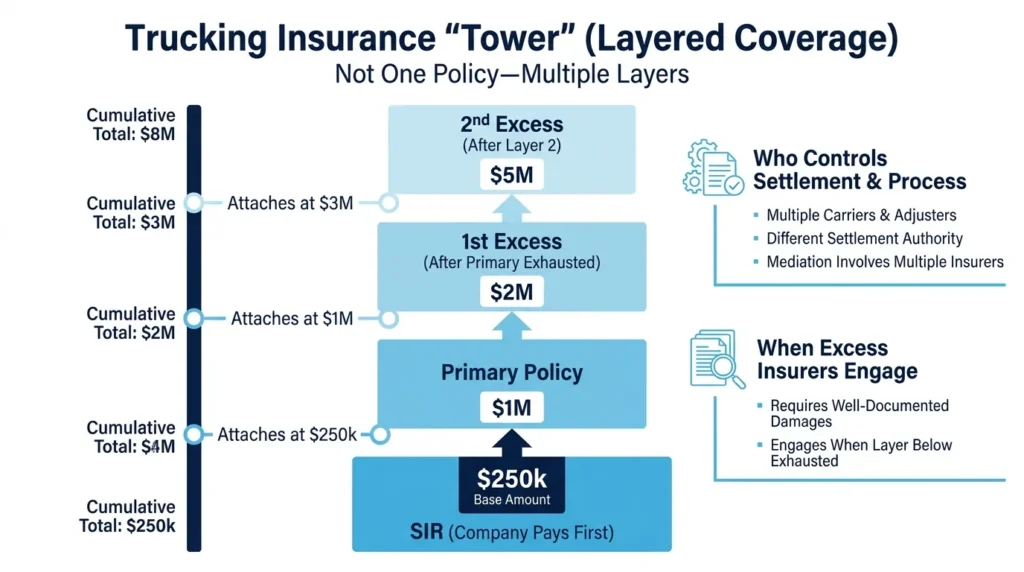

Layered Insurance Programs: The Coverage Tower

Large trucking operations typically buy insurance in layers. A primary policy covers the first portion of any claim. Excess policies stack above it, each “attaching” when the layer below is exhausted.

A simplified tower might look like this:

- Primary layer: $1 million (may include SIR)

- First excess: $2 million (attaches at $1 million)

- Second excess: $5 million (attaches at $3 million)

Each layer may involve a different insurance company with different claims personnel and different settlement authority.

For crash victims, this means:

- The adjuster you’re talking to may only control one layer

- Excess insurers often won’t engage until damages clearly exceed lower layers

- Settlement timing depends on when higher layers become involved

- Mediation may need to include representatives from multiple insurers

Identifying the full tower requires formal discovery in litigation. Requests for all policies, binders, declarations pages, and endorsements help reveal the complete picture.

Signs of Multiple Layers

Several factors suggest a trucking company has layered coverage beyond what you’ve been told:

- Catastrophic injuries with extensive medical treatment

- Large national or regional carrier

- Hazardous materials or specialized cargo operations

- Multiple victims in the same crash

- Complex corporate structure with affiliated entities

When a crash involves truck driver negligence causing serious harm, the full tower of coverage becomes essential to understanding potential recovery.

Captive Insurance: When the Trucking Company Is Its Own Insurer

A captive insurance company is an insurer created and owned by the business it covers. Large trucking fleets form captives to retain risk, control claims handling, and potentially access reinsurance markets.

For crash victims, “captive” means the trucking company has even more control over your claim. The entity paying isn’t a traditional insurer with independent interests. It’s essentially the trucking company itself, wearing an insurance hat.

Captives offer trucking companies several advantages:

- Stable premiums regardless of market conditions

- Direct control over claims decisions

- Ability to retain profitable risk

- Access to reinsurance for catastrophic losses

The practical impact for claimants includes more sophisticated defense strategies, more paperwork, and potential disputes about which entity is actually responsible for payment.

Captives often buy excess insurance above their retained layer. So “captive” doesn’t mean “no real insurance.” It means the first layer is self-funded, with traditional coverage potentially available above it.

Fronting Arrangements: The Name on Paper vs. The Real Payer

“Fronting” occurs when a licensed, admitted insurer issues a policy to satisfy legal requirements, but the actual risk is transferred back to the insured or its captive through reinsurance.

You might see a major insurance company’s name on filings. That company issued the policy and appears on official documents. But through a fronting arrangement, the trucking company’s captive actually bears most or all of the risk.

Why is this important? The decision-makers may not be who you expect. Settlement authority might rest with the captive, not the fronting carrier. Multiple stakeholders (fronting insurer, captive, reinsurers, coverage counsel) may need to approve any resolution.

This can mean:

- Slower response times

- More coverage-position letters

- Additional layers of approval for settlements

- Confusion about who to negotiate with

To confirm whether fronting is involved, your attorney can request the full policy including all endorsements, identify who handles claims day-to-day, and determine whether separate coverage exists for affiliated entities like leasing companies or owner-operator management firms.

Risk Retention Groups in Trucking

A risk retention group is a specific type of insurer owned by its members, created under the federal Liability Risk Retention Act. RRGs can write liability coverage across all states while being regulated primarily in their state of domicile.

For a Texas crash victim, this means the insurer might be based in Vermont or South Carolina, even though your crash happened in Tarrant County. Claims handling may feel less local. The insurer name might be completely unfamiliar.

Don’t assume an unknown insurer name means inadequate coverage. It may simply be an RRG layer in a larger tower. The key is confirming all coverage through proper investigation and discovery.

RRG and captive structures often involve more coverage-position letters and narrower policy interpretations. Early confirmation of all insureds and all layers prevents surprise gaps later, especially in severe injury cases.

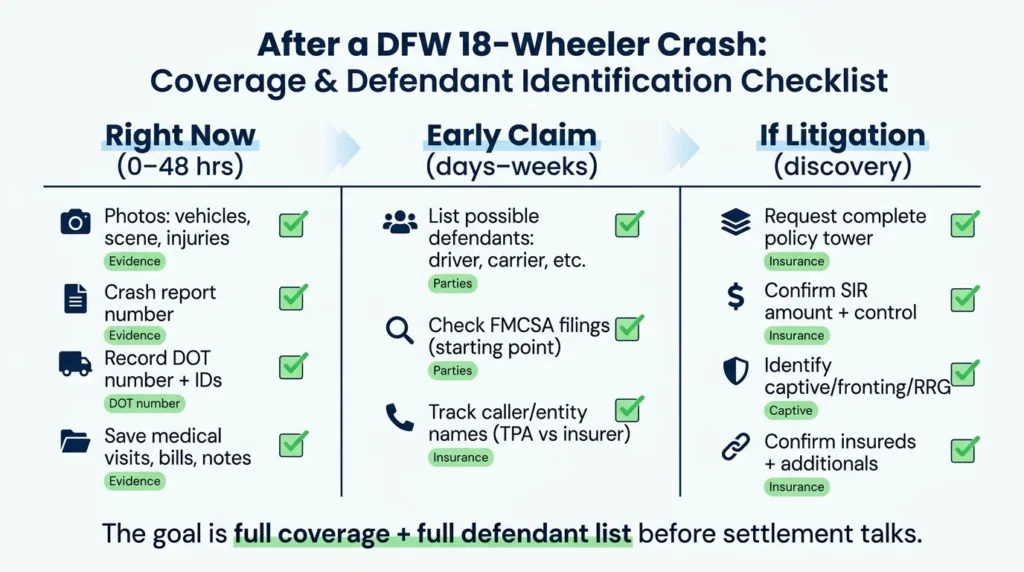

Identifying Coverage and Responsible Parties After a Crash

Taking systematic steps helps cut through insurance complexity:

Preserve evidence immediately. Photograph the scene, vehicles, and any visible injuries. Get the crash report number. Note DOT numbers from the truck’s cab and door. Record trailer identification numbers.

Identify all potential defendants. Beyond the driver, consider the motor carrier, owner-operator, trailer owner, shipper, broker, maintenance provider, and any leasing entities. Each may have separate insurance.

Check public filings. FMCSA’s database shows compliance filings, though not the full coverage picture. This provides a starting point for identifying the carrier and their registered insurance.

Request full disclosure. Through formal discovery in litigation, demand complete policy tower details, SIR amounts, all additional insureds, and any captive or fronting arrangements.

Realistic Settlement Expectations

Understanding the insurance structure helps set realistic expectations for timing and negotiation.

Early offers are often conservative when the trucking company is paying through an SIR. Strong evidence of liability and well-documented damages can change that calculus.

Excess insurers typically engage once documentation shows the claim may exceed underlying layers. This often happens after medical treatment stabilizes and the full extent of damages becomes clear.

Mediation timing is important in complex towers. All relevant insurers need to participate for meaningful settlement discussions. A structured demand package with clear damages documentation helps move all layers toward resolution.

When to Contact a Truck Accident Attorney

Certain situations call for legal help sooner rather than later:

- Fatality or ICU-level injuries

- Multiple vehicles or victims involved

- Commercial fleet with complex corporate structure

- Quick contact from multiple adjusters or defense attorneys

- Confusing insurer names or entities

- Any indication of captive, RRG, or layered coverage

Bring to your first consultation: the crash report number, photos from the scene, your medical provider list, wage and income documentation, any letters or emails from insurers, and a timeline of events.

How Angel Reyes & Associates Can Help

Trucking insurance structures are designed to protect carriers, not crash victims. Identifying all coverage, all responsible parties, and realistic settlement ranges requires experience with these complex arrangements.

At Angel Reyes & Associates, our firm has spent over 30 years handling truck accident cases across Texas. We’ve recovered more than $1 billion for clients and understand how captives, SIRs, layered programs, and fronting arrangements affect claims.

We offer free consultations and work on contingency, meaning no fee unless we win. Our team can investigate the full insurance picture, identify all defendants, and fight for fair compensation through the entire tower of coverage.

If you’ve been hurt in a truck crash in Dallas, Fort Worth, or anywhere in Texas, contact us to discuss your situation.

Past results do not guarantee future outcomes.

Shell Insurance Entity FAQs

Does an MCS-90 guarantee the trucking company has extra insurance money available for my claim?

Not necessarily. An MCS-90 is a financial responsibility endorsement that can protect the public in some situations, but it is not the same thing as a full liability policy and does not automatically reveal the carrier’s total available coverage.

Can more than one insurance policy apply to the same truck crash?

Yes. Depending on the facts, separate coverage may exist for the motor carrier, trailer owner, owner-operator, leasing company, or other businesses involved in the trip.

What if the trucking company says it is “self-insured”?

That does not always mean there is no insurance at all. A carrier may retain part of the risk itself and still have excess or backup coverage above that amount.

Are risk retention groups backed by a state guaranty fund if the insurer fails?

Usually no. RRGs are generally not protected by state insurance guaranty funds, which is one reason it is important to identify the exact insurer and policy structure early.

Is it important whether the truck was operating in Texas only or crossing state lines?

Yes. Interstate and intrastate operations can involve different filing and financial responsibility rules, so the trip details can affect which requirements apply after a crash.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...