How to Fight a Lowball Insurance Offer

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- A lowball offer is an opening position, not a final number, and you can reject and counter that offer in writing.

- Texas Insurance Code Chapter 542 adds an 18% annual interest penalty when insurers miss claim-handling deadlines on first-party claims.

- CPRC § 16.003 gives you two years from the injury date to file a Texas personal injury lawsuit.

You were rear-ended on I-35 heading north toward Round Rock, and the other driver’s insurer just sent you an offer that wouldn’t cover half of your ER bill. The number feels insulting. You’re trying to figure out whether to sign, push back, or leave the negotiating to a lawyer.

Before you do anything, you need to understand what just happened and what your real options are.

Why Insurers Make Lowball Offers

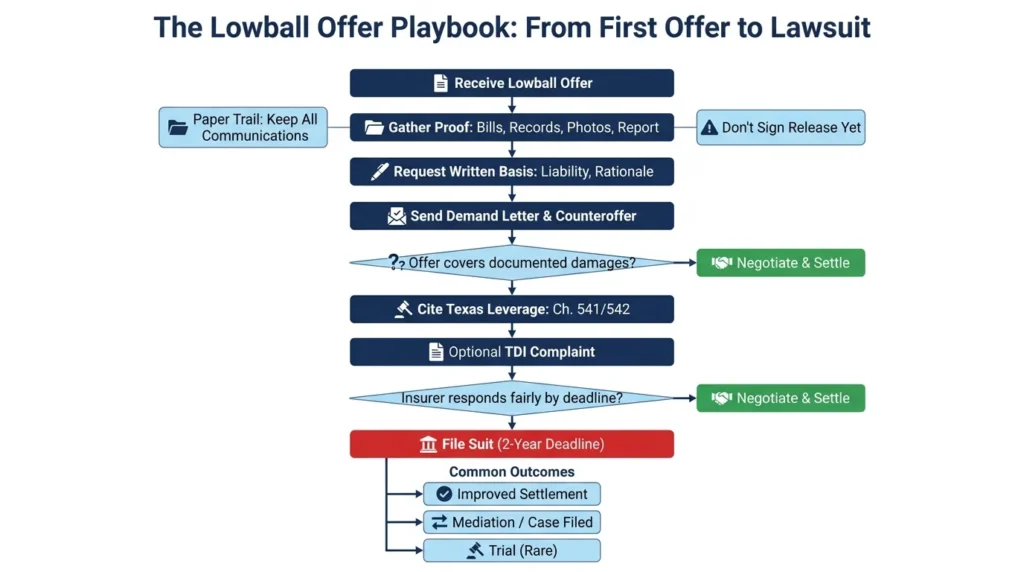

A lowball offer is a calculated opening position – intended to protect the insurer’s profit margin – not a fair valuation of your claim. Insurers send meager first offers because most claimants accept them without countering. You are under no obligation to accept it and may negotiate, counter, or walk away anytime before signing a release.

Insurance adjusters use a few standard tactics to reduce your payout:

- They dispute liability.

- They downplay injury severity.

- They apply a low multiplier to pain and suffering.

- They claim that you are partly at fault.

The right way to judge an offer is to compare it against your documented economic damages plus a fair estimate of non-economic damages (meaning factors like pain and suffering and emotional distress). Medical bills, future treatment costs, and lost wages all add up fast, and a fair settlement should reflect every dollar.

If you want a benchmark before drafting your response, our guide to average car accident settlements in Texas gives you a starting point. You can also read more about the risks of accepting an insurance settlement offer too quickly before you respond.

Build Your Case Before You Counter

Strong documentation is the foundation of every step that follows. Before you write a single word back to the adjuster, gather every record that proves the full extent of your damages. Skipping this step is how claimants end up settling for too little.

Pull together your medical records, hospital bills, prescription receipts, and any treatment plan your doctor signed. Add proof of lost wages: pay stubs, an employer verification letter, tax records, or a self-employment income summary covering the time you missed work.

Then ask the adjuster, in writing, to explain how they determined the offer. Which liability percentage did they apply? Which multiplier did they use for pain and suffering? Their answer creates a paper record and tells you exactly what to contest in your counteroffer.

Photos, the police report, witness statements, and any expert opinion you can collect strengthen the factual record.

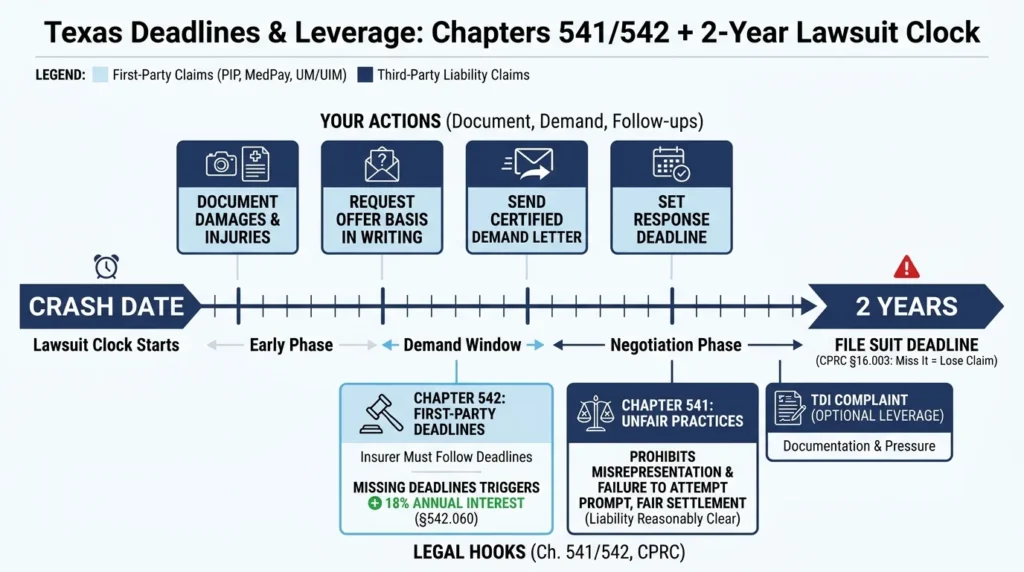

Texas law also gives you independent power over the timing of the insurer’s response. Under Texas Insurance Code Chapter 542, insurers must acknowledge, investigate, and accept or reject your claim by set deadlines. If they stall, you can cite that delay later.

For a closer look at those deadlines, see our breakdown of the Texas insurance settlement timeline.

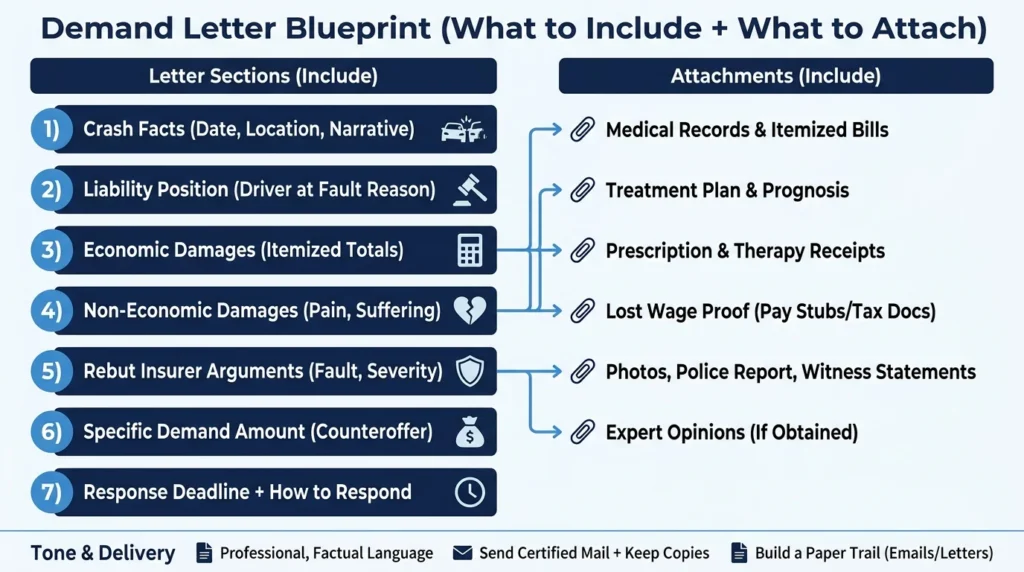

Write an Effective Demand Letter

In a demand letter, you reject the lowball offer, lay out your full damages, and propose a different amount. Send this document by certified mail to create a time-stamped record. This is the first formal step in the escalation ladder, and it sets the tone for everything that follows.

Here is how to create a clear, effective demand letter.

- Open with a factual summary of the crash.

- List your economic damages, with documents attached.

- Explain your non-economic damages and the multiplier you used.

- Rebut any liability or fault arguments the adjuster raised.

- End with a specific counteroffer figure and a response deadline.

Set your counteroffer above the number you would actually accept. Leaving room to negotiate down is standard practice, not a weakness. Adjusters expect it.

Make sure to keep the tone professional and factual, since emotional language gives the adjuster an excuse to dismiss your letter instead of responding to its content. Save copies of every email, letter, and voicemail. The paper trail matters if negotiations stall.

An attorney can also help you calculate non-economic damages like anxiety, depression, and physical pain resulting from a car accident before you commit to a number on paper.

Use Bad Faith Exposure as a Negotiating Lever

Texas law puts real pressure on insurers who handle claims unfairly, and you can use that pressure as a negotiating tool. By citing the rules in your demand letter, you show that you know what the insurer is required to do.

Texas Insurance Code Chapter 541 prohibits insurers from misrepresenting claim value, failing to attempt a prompt and fair settlement when liability is reasonably clear, and using other deceptive claims-handling practices. Referencing Chapter 541 in writing tells the adjuster you are paying attention.

Chapter 542 sets the timing rules. When an insurer misses those deadlines on a first-party claim – such as your own PIP, MedPay, or uninsured motorist coverage – statutory interest of 18 percent per year can be tacked on to the unpaid amount under Section 542.060. That creates real financial exposure for the insurer and meaningful leverage for you.

You also have the option of filing a complaint with the Texas Department of Insurance. This costs nothing, and the complaint goes on the insurer’s regulatory record. While this action will not force a settlement on its own, it documents the insurer’s conduct and will support a future bad faith claim if talks break down.

When to Escalate to Litigation

Filing suit is the right move when the insurer ignores your demand letter, comes back with another inadequate offer, or denies the claim outright after you have documented liability and damages. Litigation is the final rung of the escalation ladder, and timing matters because the clock is already running on your right to sue.

Texas gives you a hard deadline. Under Texas Civil Practice and Remedies Code (CPRC) § 16.003, you have two years from the date of injury to file a personal injury lawsuit. The clock runs from the crash date, not from the date you got the lowball offer. Miss it and you lose your right to sue entirely.

Filing suit does not mean you are headed to trial. Most cases are settled after a claimant files a lawsuit, because the insurer’s risk rises once a judge is involved.

The Stowers doctrine adds another layer of pressure in Texas. According to this principle, the insurance company of the at-fault driver must act in good faith when settling a liability claim. So if you make a policy-limits demand that meets Stowers requirements and the insurer refuses, the insurer may be on the hook for any verdict above policy limits.

A contingency fee attorney charges nothing up front and is paid only if you recover damages. This arrangement eliminates the cost barrier that pushes many claimants into accepting an unfair offer. Our recent case results show how accident victims have benefited from getting professional help.

If your claim involves a commercial vehicle or multiple insurers, the policy-limits dynamics in truck accident cases can shift the escalation strategy meaningfully.

Talk to a Texas Injury Attorney Before You Settle

Angel Reyes & Associates has handled insurance disputes across Texas for decades and has a track record of significant recoveries for clients. We work on contingency, meaning we receive no fee unless we win, so it costs you nothing to have our attorneys review your settlement offer. Contact us today for a free consultation before you sign anything.

Past results do not guarantee future outcomes.

Lowball Offer FAQs

Can an insurer legally withdraw a settlement offer after I reject it?

Yes. In Texas, a settlement offer can be revoked anytime before you accept it, because it is not a binding contract until both sides agree. This is one reason to counter promptly once you decide to push back.

Does comparative fault affect how much I can recover if I share some blame for the crash?

Texas follows a modified comparative fault rule under Civil Practice and Remedies Code § 33.001. You can still recover damages if you are less than 51 percent at fault, but your award is reduced by your percentage of fault.

What happens to my claim if the at-fault driver's insurance policy limits are too low to cover my damages?

You may be able to seek the remaining amount through your own underinsured motorist coverage if your policy includes it. Texas does not require insurers to offer underinsured motorist coverage, but they must offer it in writing, and many drivers carry it.

Can I reopen a claim after I have already signed a settlement release?

Generally no. A signed release in Texas is treated as a final resolution of the claim, which is why reviewing any offer before signing matters. Courts rarely set aside a signed release unless you can show fraud, duress, or mutual mistake.

Will my medical bills keep accruing interest while I negotiate, and can I recover that interest in a settlement?

Medical providers can charge interest on unpaid balances under Texas Finance Code § 304.003, but that interest is typically part of your total economic damages, rather than a separate recovery category. Including projected interest in your demand letter helps ensure that your counteroffer reflects the full cost.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...