What Happens When a Trucking Company Goes Bankrupt After a Crash?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- The automatic stay pauses most lawsuit activity against a bankrupt trucking company, but it doesn't dismiss your case or eliminate insurance coverage.

- You may need to file a proof of claim by the bankruptcy bar date to preserve your right to any estate distribution.

- Texas's two-year statute of limitations for personal injury claims continues to run, so tracking both state and bankruptcy deadlines is critical.

You were seriously injured in a truck accident on I-35E near downtown Dallas last month. You filed a claim against the trucking company. Now you’ve received a notice in the mail: the company has filed for bankruptcy. Your first thought is that your case is over and you’ll never see a dime.

That fear is understandable, but it’s often not accurate. A trucking company bankruptcy changes how you pursue your injury case. It doesn’t necessarily mean you can’t recover compensation. The path forward requires understanding new rules, new deadlines, and new strategies.

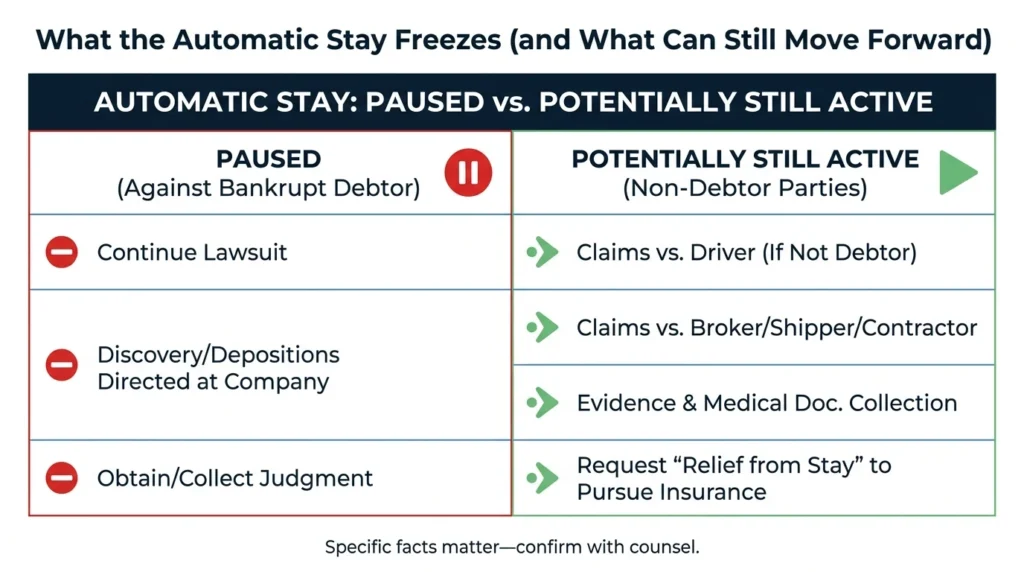

What the Automatic Stay Is & What It Immediately Stops

When a company files bankruptcy, federal law triggers something called the “automatic stay.” This is a court order that immediately pauses most legal actions against the company that filed.

The automatic stay typically prohibits:

- Continuing a lawsuit against the bankrupt trucking company

- Conducting discovery or depositions targeting the debtor

- Obtaining or collecting judgments against the company

This doesn’t mean your case is dismissed. It means certain actions are frozen until the bankruptcy court says otherwise. The underlying facts of your crash, your injuries, and the company’s liability still exist.

The legal process to address them has simply shifted to a different track.

One critical point to take note of is that the automatic stay generally applies to the company that filed bankruptcy. Claims against non-debtor parties may still move forward. If the truck driver, a freight broker, a maintenance contractor, or another carrier shares responsibility for your crash, those claims might continue in state court while the bankruptcy plays out.

How Your Injury Case Becomes a Bankruptcy “Claim”

Once a trucking company files bankruptcy, your right to compensation becomes what bankruptcy law calls a “claim.” You’re now considered a creditor of the company, similar to vendors, lenders, and others the company owes money.

This shift means you’ll receive official notices from the bankruptcy court. These notices contain critical information:

- The bankruptcy case number and court location

- Whether the company filed Chapter 7 (liquidation) or Chapter 11 (reorganization)

- The name of the trustee or claims agent handling the case

- Any deadlines for filing claims

The most important deadline to watch for is the “bar date.” This is the deadline for filing a proof of claim in the bankruptcy case. Miss this deadline, and you may lose your right to share in any distribution from the company’s remaining assets.

Chapter 7 and Chapter 11 bankruptcies work differently. In Chapter 7, the company is shutting down. A trustee sells off assets and distributes proceeds to creditors. In Chapter 11, the company attempts to reorganize and continue operating while addressing its debts. Either way, your injury claim must be handled through the bankruptcy process if you want any recovery from the company itself.

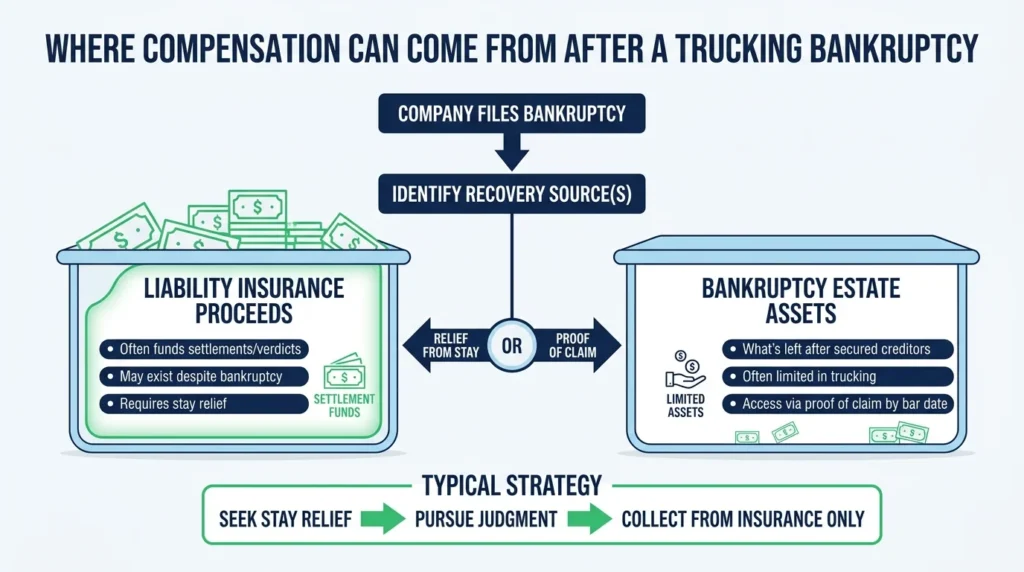

Insurance vs. Bankruptcy Estate Assets: Where Money May Still Come From

Here’s what many crash victims don’t realize: most truck accident settlements and verdicts are paid by liability insurance, not directly from the trucking company’s bank account. Bankruptcy can complicate the path to that insurance money, but it doesn’t automatically eliminate coverage.

Think of two separate “pots” of potential recovery:

Liability insurance proceeds: Commercial trucking policies often carry substantial coverage. These policy proceeds may still be available even if the trucking company has no other assets.

Bankruptcy estate assets: This is whatever value remains in the company after secured creditors are paid. For many bankrupt trucking companies, this pot is small or empty.

The practical goal in many cases is obtaining “relief from stay” from the bankruptcy court. This is permission to continue your lawsuit, but typically with a specific limitation: you can pursue a judgment to establish liability and damages, then collect only from available insurance proceeds rather than from the company directly.

This approach protects the bankruptcy estate while still allowing injured victims to access insurance coverage. Courts regularly grant this type of limited relief when insurance exists and the injured party isn’t trying to drain estate assets.

When You Might Need Both: Stay Relief & Proof of Claim

Some situations require pursuing insurance while also preserving your right to share in estate distributions. Consider filing a proof of claim if:

- Insurance coverage is disputed or uncertain

- Your damages may exceed available policy limits

- Multiple claimants are competing for limited insurance proceeds

- The trucking company had a self-insured retention

Filing a proof of claim reserves your place in the creditor process. It doesn’t guarantee payment, but it protects your position. Federal Rules of Bankruptcy Procedure Rule 3002 governs the timing requirements for these filings.

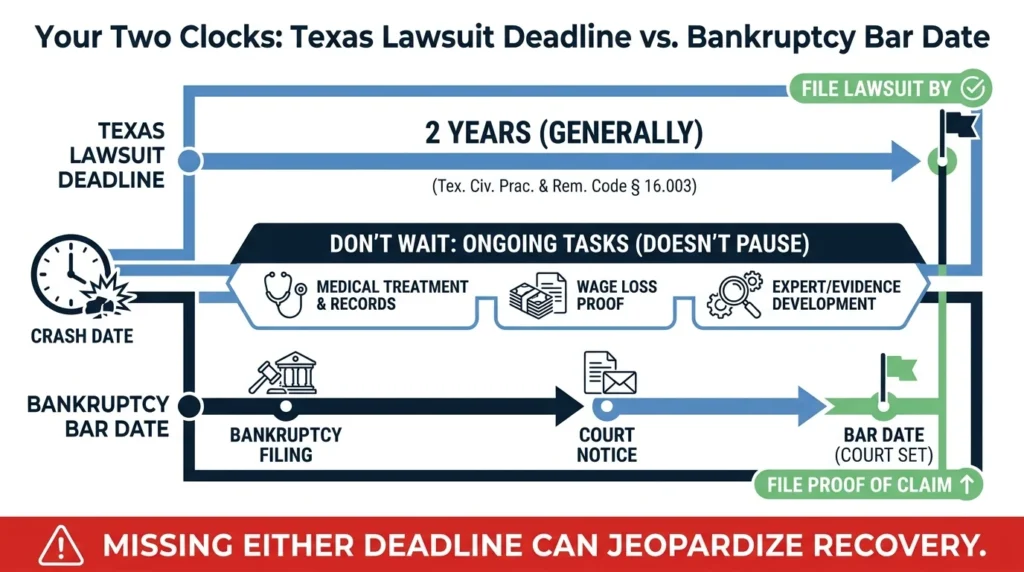

Important Deadlines in Texas

Bankruptcy can pause certain litigation actions, but it doesn’t protect you from all time limits. You need to track two separate clocks.

Texas’s two-year deadline: Under Texas Civil Practice and Remedies Code § 16.003, you generally have two years from the date of injury to file a personal injury lawsuit. This deadline doesn’t automatically stop running just because the defendant filed bankruptcy. While there may be arguments for tolling in certain circumstances, the safest approach is to plan around this deadline.

Bankruptcy bar dates: The bankruptcy court sets its own deadlines for filing proofs of claim. These can arrive quickly, sometimes within 90 days of the bankruptcy filing. The deadline is announced in official notices mailed to known creditors.

Missing either deadline can be devastating. The Texas deadline could bar your lawsuit entirely. The bankruptcy bar date could eliminate your right to any estate distribution.

Meanwhile, keep your medical treatment and documentation moving forward. Evidence doesn’t pause during bankruptcy proceedings. Medical records, wage loss documentation, and expert opinions all take time to develop. Waiting until the bankruptcy resolves could leave you scrambling to build your case. Review what to do after a truck accident to make sure you’re preserving critical evidence.

What to Do This Week If You Get a Bankruptcy Notice

If you’ve received a bankruptcy notice after a truck crash in the Dallas–Fort Worth area, take these steps immediately:

Save the notice and identify key information. Note the debtor’s exact legal name, the bankruptcy case number, the chapter filed, and the court handling the case. Calendar any dates shown, especially any bar date for filing claims.

Gather your documentation. Collect your crash report, medical bills and records, proof of lost wages, any insurance correspondence, and any prior lawsuit filings or demand letters. Having these ready allows your legal team to act quickly.

Identify all potentially responsible parties. The bankrupt trucking company may not be the only defendant. The truck driver, freight brokers, cargo loaders, maintenance contractors, and other carriers may share liability. Pursuing these non-debtor parties can reduce your reliance on the bankruptcy estate. Understanding how trucking companies and insurers delay and deny claims helps you anticipate obstacles.

Consult with an attorney experienced in both trucking cases and bankruptcy procedure. These cases involve overlapping legal systems with different rules, different courts, and different deadlines. A lawyer can evaluate whether to seek stay relief, whether to file a proof of claim, and how to pursue non-debtor defendants.

How Angel Reyes & Associates Can Help

A trucking company bankruptcy adds complexity to an already difficult situation. You’re dealing with serious injuries, mounting medical bills, and lost income. Now you’re also navigating federal bankruptcy court while trying to preserve your rights under Texas law.

At Angel Reyes & Associates, we have over 30 years of experience handling complex truck accident cases across Texas. We understand how commercial trucking insurance works, how to identify all responsible parties, and how to protect your claim when a defendant files bankruptcy. Our firm has recovered more than $1 billion for clients, and we offer free consultations with no fee unless we win.

We have more than 20 office locations across Texas, including offices serving the Dallas–Fort Worth metroplex. We’re available 24/7 and can handle most of your case remotely.

If you’ve been injured in a truck crash and the at-fault company has filed bankruptcy, don’t assume your case is over. Contact us today to discuss your options and protect your right to compensation.

Past results do not guarantee future success.

Trucking Company Bankruptcy FAQs

What if I was hurt before the bankruptcy filing, but I had not filed a lawsuit yet?

You may still have a bankruptcy claim even if no lawsuit was on file when the company filed bankruptcy. The deciding factor here is usually when the crash happened, not whether you had already sued.

Will bankruptcy erase the trucking company’s insurance policy?

Usually, no. Bankruptcy does not automatically cancel a liability policy that was already in place. Coverage can still depend on the policy terms, notice requirements, exclusions, and whether the policy was active for the date of the crash.

What is a self-insured retention, and how does it effect a truck crash case?

A self-insured retention is an amount the trucking company may have to pay before the insurer starts paying. If the company is bankrupt, that gap can make settlement and insurance recovery more complicated.

Can a bankruptcy trustee challenge the amount of my injury claim?

Yes. Even if your claim is valid, the trustee or another party in the bankruptcy case may object to the amount, supporting documents, or how the claim was filed.

Do I need to keep saving medical records and lost-income proof if the bankruptcy case slows everything down?

Yes. Treatment records, bills, pay stubs, and employer letters can still be important later for insurance negotiations, bankruptcy filings, or any request to value your damages.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...