How Much Car Insurance Do I Need in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas requires 30/60/25 liability coverage, but those limits rarely cover a serious crash.

- Most Texas drivers should carry 100/300/100 liability, plus uninsured motorist coverage.

- Roughly one in seven Texas drivers is uninsured, which makes UM and UIM protection essential.

In the blink of an eye, even a small, low-speed car accident can rack up bills and expenses in the tens of thousands of dollars. Almost nobody has that kind of money sitting around, much less enough to cover the costs of any injuries that might be involved.

If you don’t want to get left exposed in the event of an accident, you might be wondering: how much car insurance do I need in Texas? There are some definitive, legally mandated answers, but that framework isn’t as straightforward as it might seem when applied to a real-world incident.

Texas Minimum Car Insurance Requirements

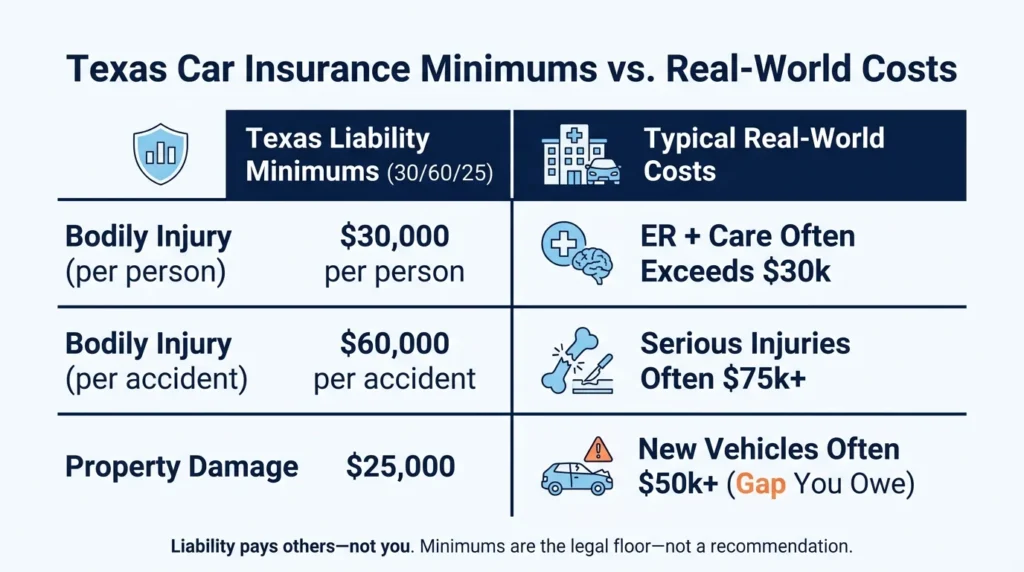

Texas law requires every driver to carry liability coverage of at least $30,000 per injured person, $60,000 per accident, and $25,000 for property damage. This is called 30/60/25 coverage. It is the legal floor, not a recommendation. The numbers reflect what you would owe the other driver if you caused a crash, not what your own policy would pay you.

The state’s financial responsibility rules are stated in Texas Transportation Code Section 601.072. Drivers who fail to carry proof of coverage face fines starting at $175 for the first offense, with steeper penalties and a possible license suspension for repeat violations, after which SR-22 filings are often required to get back on the road.

Remember, minimum coverage protects other drivers, not you. If another driver hits you and has no insurance, your 30/60/25 policy does nothing. If you cause a crash with damages above those limits, you owe the rest personally. This gap is where most drivers run into trouble after a serious car accident in Texas.

Why State Minimums Are Dangerous

State minimums were set decades ago and have not kept pace with modern medical and vehicle costs. A single ambulance ride and ER visit can blow past $30,000, and that’s before any surgery, imaging, or follow-up care. If you caused a crash, you are personally on the hook for everything above your limits.

Hospital bills are the first place minimums fail. A broken femur, a back injury, or a few days in the ICU routinely costs $75,000 or more. Texas insurers and the Texas Department of Insurance both warn consumers that minimum policies often run dry just hours after a serious crash.

Property damage limits fall short just as fast. The average new vehicle in Texas now sells for over $50,000. If you total a single late-model truck or SUV with $25,000 in coverage, then you’ll owe the difference. In multiple-vehicle pileups on Texas freeways, that financial vulnerability can add up quickly.

When your policy stops paying, the other driver can come after your wages, savings, and home equity. It’s important to understand your financial vulnerability and learn what to do after a Texas car accident before you experience this situation firsthand.

Recommended Coverage Levels for Texas Drivers

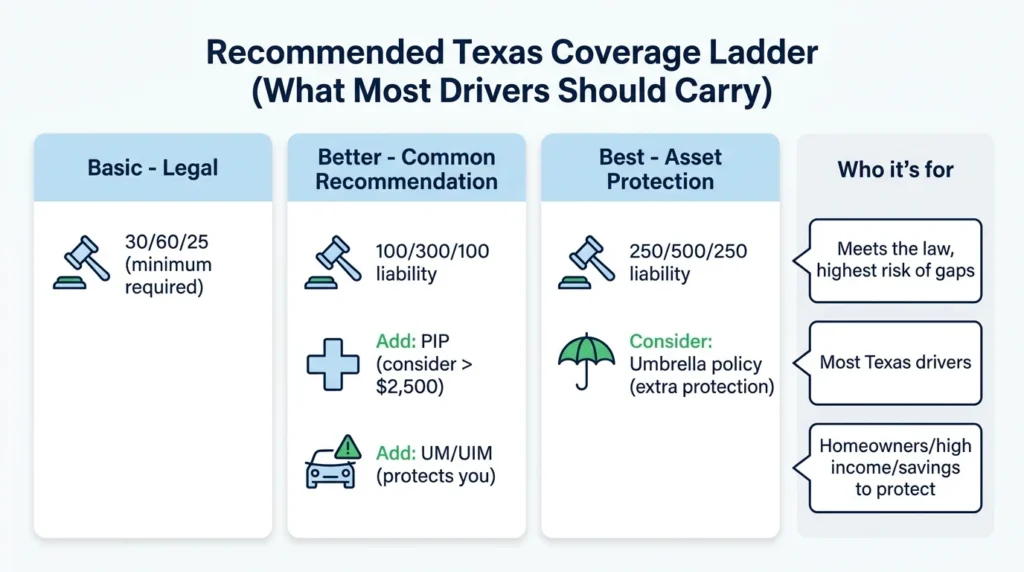

For most Texas drivers, 100/300/100 is a sensible target: $100,000 per person, $300,000 per accident, and $100,000 in property damage. Drivers with homes, retirement accounts, or higher incomes should consider 250/500/250 or an umbrella policy on top. The right number depends on what you would lose in a lawsuit.

Two add-ons are just as important as raising your liability limits. Personal injury protection (PIP) pays your medical bills and a portion of lost wages, no matter who caused the crash. Texas insurers must offer at least $2,500 in PIP, and you can decline it only in writing. Most drivers should keep it and even consider raising it.

According to recent data, Texas has one of the highest uninsured driver rates in the country. That single statistic is the strongest argument for buying more than the minimum. Match your liability limits to your assets, then add coverage that pays you when the other driver cannot.

Uninsured & Underinsured Motorist Coverage

Uninsured motorist (UM) coverage pays your medical bills and damages if an at-fault driver has no insurance or flees the scene. Underinsured motorist (UIM) coverage kicks in if the other driver has insurance but not enough to cover your injuries. Both are offered alongside every Texas auto policy and can be rejected only in writing.

Skipping these coverages is a common mistake. With roughly one in seven Texas drivers uninsured, the odds of being hit by someone who cannot pay are high. UM and UIM are usually inexpensive, compared to the protection they provide for serious uninsured and underinsured motorist accidents.

The Real Cost of Being Underinsured

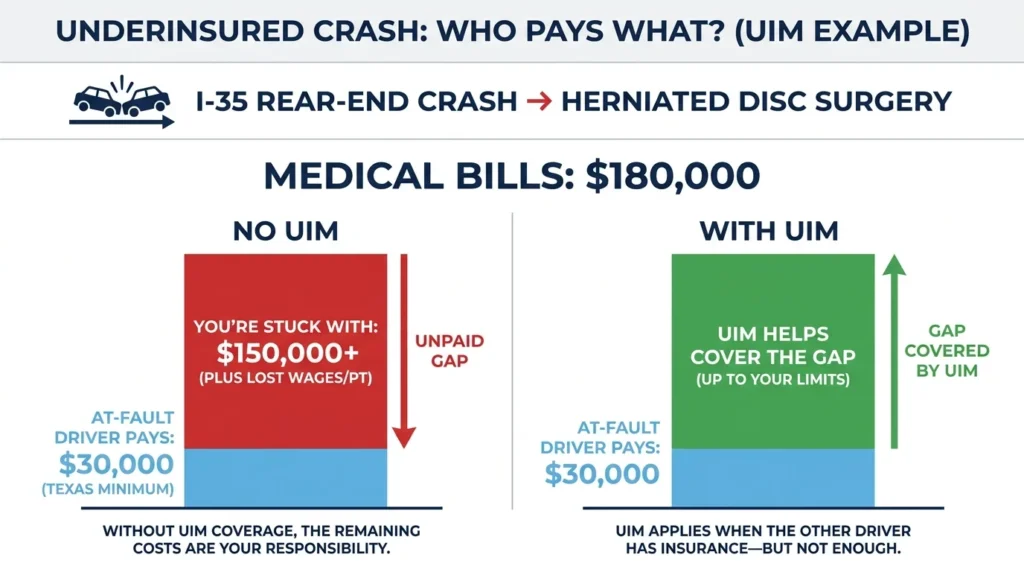

Imagine you’re in a rear-end crash on the I-35 corridor that causes a herniated disc requiring surgery. Your medical bills total $180,000. The at-fault driver only carries the minimum insurance coverage required by Texas law. Their insurer pays $30,000 and closes the file. Without UIM coverage, you must absorb the remaining $150,000, plus lost wages and future physical therapy.

This is not a worst-case scenario. It is a routine outcome of two drivers carrying state minimums in a moderately serious crash. Multiply this injury across a family vehicle, and the numbers climb even higher. If you’ve been hit by an underinsured driver, knowing your options under Texas car accident laws can change the outcome of your case.

The long-term damage is financial, as well as physical. Drivers with minimal coverage who cause major crashes face wage garnishment, liens on property, and, in some cases, bankruptcy. Drivers who are hit by underinsured motorists without UIM protection can face similar financial strain from unpaid losses. Adequate coverage on both sides of your policy is the single best protection against either outcome.

If you’re unsure how your insurance policy might hold up in a serious accident, we have an insurance grading interactive tool available that assigns a letter grade to your policy based on what’s included and how protected you might be.

Talk With Angel Reyes & Associates About Your Accident

If you were injured by a driver whose insurance falls short, the gap between their limits and your real costs is exactly the kind of problem we can solve. Angel Reyes & Associates has more than 30 years of experience handling Texas auto claims and has recovered more than $1 billion recovered for clients.

We offer free consultations and work on contingency, which means you pay no fee unless we win. We serve drivers across Texas in English and Spanish. See how we have helped other clients and what they have to say about our work. Call or contact us online any time. We are available 24/7.

Past results do not guarantee future outcomes.

Insurance Requirement FAQs

Can I buy car insurance after an accident in Texas?

You cannot buy coverage for an accident that has already happened, but you can purchase a new policy for future protection if your current coverage is cancelled or expired.

What happens if both drivers only have minimum insurance in a serious crash?

Each driver’s policy pays up to their limits, but any costs above those amounts become personal debt that can lead to wage garnishment or asset seizure.

Does comprehensive and collision coverage affect how much liability insurance I need?

Comprehensive and collision coverage protect your own vehicle, while liability protects other drivers in the event that you cause a crash, so both types serve different purposes and should be evaluated separately.

How much does it cost to increase from minimum to recommended coverage in Texas?

Upgrading from 30/60/25 to 100/300/100 typically adds $300 to $600 annually, depending on your driving record and location. Our car insurance buying guide can help you visualize this change with a handy interactive tool.

Can I be sued personally if my insurance limits are too low?

Yes, if you cause damages that exceed your policy limits, the injured party can sue you personally for the remaining amount and pursue your assets to collect payment.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...