Does Insurance Cover OEM Parts After A Crash?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

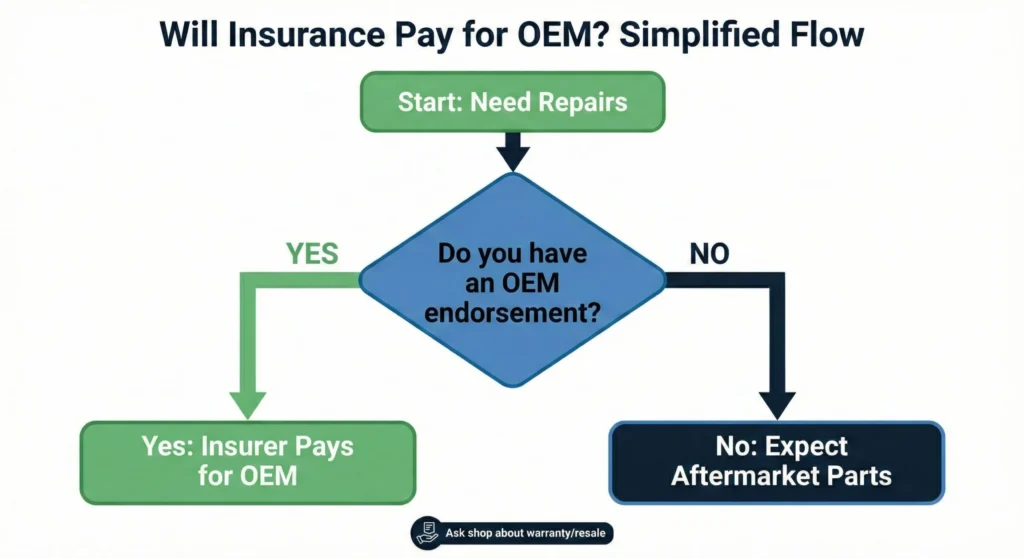

- Most Texas policies cover aftermarket parts in vehicle repairs unless you have an OEM endorsement or negotiate for factory parts.

- Without OEM coverage, you can request OEM parts, but you may need to pay the price difference.

- Parts choices can affect warranty concerns and diminished value claims, so document repairs and push back if the offer does not restore your vehicle properly.

Does Insurance Cover OEM Parts After A Crash?

You’re reviewing a repair estimate after a wreck on I-35, and the shop lists parts from manufacturers you don’t recognize. While you might demand the best for your car, your insurance might not be set up to give you that in the event of a collision. Most standard Texas auto insurance policies default to aftermarket parts unless your policy includes an OEM endorsement or you negotiate otherwise.

While some aftermarket parts may work okay, it’s perfectly reasonable to demand factory replacement parts so you know your car will work the same way it did previously. Not to mention that aftermarket repair parts can compromise your car’s warranty and potential resale value in the future. Knowing what your policy actually covers puts you in control of this important conversation with your claim adjuster.

What OEM & Aftermarket Parts Mean for Your Repair

“OEM” stands for “original equipment manufacturer, and is essentially a way of describing parts that are made by your vehicle’s original manufacturer. Aftermarket parts are made by third-party companies to fit the same specifications as OEM parts, but they may not be subject to the same material requirements or rigorous testing that guarantee the level of performance the original manufacturer intends.

OEM parts are generally held to a higher manufacturing standard, which in turn means they usually carry a higher price tag.

Aftermarket parts are not automatically inferior. Some are manufactured to meet or even exceed OEM standards. However, others do not fit as precisely or last as long because they are made with cheaper materials. This difference matters most for safety-critical components like airbag sensors, bumper reinforcements, and structural panels.

Insurers often prefer aftermarket parts because they cost less and generally perform the same function out of the box. A generic fender might run 30 to 50 percent cheaper than the version you purchase from Ford or Toyota. However, that difference could be important when it comes to safety systems and components.

How Texas Insurance Policies Handle Parts Coverage

Texas does not require insurers to cover OEM parts. Most standard collision and comprehensive policies include language allowing “like kind and quality” parts, which gives adjusters room to approve aftermarket components.

An OEM endorsement changes this. It’s an add-on you purchase that requires the insurer to cover the cost of original manufacturer parts. If you drive a newer vehicle or one still under warranty, this endorsement can protect your coverage and resale value. However, it does usually mean an increased premium by typically a few dollars per month.

If you aren’t sure if you have one of these clauses in your policy, check your declarations page or call your agent to confirm. If you don’t, you can often add it before your next renewal.

What Happens When You File a Claim Without OEM Coverage?

When your adjuster writes an estimate based on your policy terms, they will almost always default to aftermarket parts if you do not have an OEM endorsement. You can still request OEM parts, but you may have to pay the difference out of pocket. We recommend getting a written breakdown from the repair shop showing the cost gap between OEM and aftermarket options to help you decide whether the upgrade is worth it for your situation.

If the at-fault driver’s insurance is paying, you have less control over this choice. Their policy dictates what they’ll cover, but you can negotiate with them. This is especially important if you can document why OEM parts matter for your vehicle’s safety or warranty.

When Part Choices Affect Your Injury Claim

Vehicle repairs and injury claims are separate but connected. The parts used in your repair can influence the total value of your claim. If aftermarket parts reduce your car’s resale value, that loss is part of your damages. Texas allows you to claim your vehicle’s diminished value after a wreck caused by someone else.

Poor-quality replacement parts that fail later can also create new safety risks. Document everything: photos of parts, invoices, and any concerns the shop raises. If a defective part causes your vehicle or the other party’s vehicle to malfunction, resulting in a crash, then the part’s manufacturer could be held liable.

If you’re dealing with serious injuries alongside vehicle damage, the stakes are higher. An attorney can help you push back on lowball estimates and ensure your claim reflects the true cost of restoring your vehicle properly.

Steps to Protect Yourself Before and After a Crash

Review your current policy now. Look for the phrase “OEM endorsement” or “original equipment manufacturer coverage.”

If you don’t have it and want it, call your insurer. Ask for a quote to add the endorsement.

After a crash, take these steps:

- Request a written estimate that identifies each part as OEM or aftermarket

- Ask the shop whether aftermarket parts affect your vehicle’s warranty

- Get a second estimate if the first one seems low

- Keep all invoices and photos of replaced parts

If the insurer refuses to budge and you believe you’re owed more, you have options. Texas is a fault-based state, meaning you can pursue the at-fault driver directly for damages their insurance won’t cover.

If you’re concerned that your vehicle may not receive the repairs it deserves in addition to the other losses you have already sustained due to an accident, reach out to an attorney to review your options as soon as possible.

Angel Reyes & Associates has guided Texans through insurance disputes and injury claims for over 30 years. If you’re facing pushback from an adjuster or are unsure whether your claim reflects your true losses, we offer free consultations to help you understand your options. Contact us to learn more.

FAQs

Will using aftermarket parts void my car’s warranty?

The Magnuson-Moss Warranty Act is a federal law that prohibits manufacturers from voiding your warranty just because you used aftermarket parts. But if an aftermarket part causes a specific problem, the manufacturer can deny coverage for that repair.

Can I force the other driver’s insurance to pay for OEM parts?

No. Their policy controls what they pay. You can negotiate or pay the difference yourself. If their offer doesn’t cover your actual losses, you may be able to file a claim for the gap.

How do I know if an aftermarket part is safe?

Ask the repair shop for the part’s certification. Parts certified by CAPA (Certified Automotive Parts Association) meet industry standards. Uncertified parts carry more risk.

Does an OEM endorsement cost a lot?

Most drivers pay between $20 and $50 per year for this endorsement, depending on their vehicle and insurer.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Graham Griffin

Editor

Graham Griffin is the Web & Content Manager at Angel Reyes & Associates, where he oversees content strategy, AI-powered workflows, a...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...