What Is UM/UIM Insurance Arbitration in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas auto policies include arbitration clauses letting you resolve UM and UIM disputes without a lawsuit.

- An arbitrator's binding award forces your insurer to pay, subject to the UIM offset under Texas Insurance Code § 1952.106.

- Arbitration often resolves Texas UM and UIM claims in months, while litigation can take several years.

You were rear-ended on I-35 heading toward Round Rock, and the at-fault driver had no insurance or far too little to cover your bills. You filed a claim with your own carrier under your UM or UIM coverage, expecting them to step in.

Now they’re dragging their feet or offering a number that doesn’t come close to what you actually lost. But there’s a tool built into your policy that can break the stalemate.

What Insurance Arbitration Is in Texas

Insurance arbitration is a formal dispute resolution process written into most Texas auto policies. It lets you bring an uninsured motorist (UM) or under-insured motorist (UIM) disagreement before a neutral arbitrator instead of filing a full lawsuit. Unlike mediation, the arbitrator’s decision is binding. Once the award is issued, your insurer must honor it.

The arbitration clause in your auto policy is a written contract right. You can exercise it when negotiations stall or your insurer undervalues your claim. Texas UM and UIM coverage is governed by Texas Insurance Code § 1952.101–110, which sets the requirements for what insurers must offer and how they calculate recovery.

When UM & UIM Arbitration Applies to Your Claim

Arbitration becomes relevant when the at-fault driver had no insurance or not enough to cover your damages, and your own insurer disputes the value of your claim. Most Texas auto policies include a mandatory arbitration clause for UM and UIM disputes. Typically, you activate this clause with a written demand if negotiations break down after being hit by an uninsured driver.

Texas Insurance Code § 1952.106 defines the recovery amount available under UIM coverage, including the offset rule. The offset is often where insurers push back hardest. Understanding how it’s calculated clarifies what’s actually at stake in your hearing.

There are some differences between UM and UIM claims, but both route through the same arbitration framework. The triggering event differs, but the process is substantially the same. You also don’t need to sue the at-fault driver first. Your right to demand arbitration runs directly from the policy contract with your own insurer.

How UIM Arbitration Works in Texas

Texas UIM arbitration follows a predictable four-step path: written demand, arbitrator selection, evidence submission, and binding award. The process is governed by your policy language and backed by state law that makes the agreement enforceable. Most cases move from demand to award in months, not years.

Step 1: Written Demand. You submit a written arbitration demand to your insurer. It cites the policy’s arbitration clause and states the disputed amount.

Step 2: Arbitrator Selection. Selection follows the policy. Common formats include each side choosing one arbitrator plus a neutral third, or a single agreed-upon neutral arbitrator. An arbitrator’s background can shape outcomes.

Step 3: Evidence Submission. Both sides submit medical records, wage loss documentation, accident reports, and expert opinions. The arbitrator reviews everything and may hold a hearing where each side presents its case.

Step 4: Binding Award. The arbitrator issues a written award. Your insurer is obligated to pay it, subject to any offset under § 1952.106.

The enforceability of the arbitration agreement itself comes from the Texas Civil Practice and Remedies Code (CPRC) § 171.001. That chapter also governs how you can confirm or challenge a final award in court. Because hearings are less formal than trials and timelines are tighter, arbitration is often the faster path to recovery once direct talks have failed. Understanding how PIP, MedPay, and UM/UIM coverage stack helps you find all possible sources of compensation.

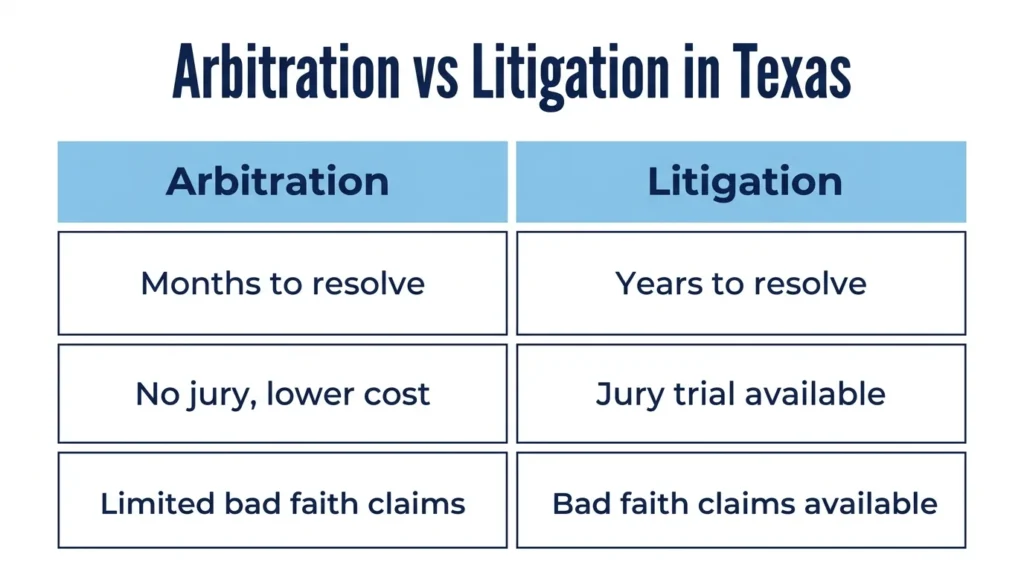

Arbitration vs. Litigation for Texas UM & UIM Claims

Arbitration and litigation are not the same tool. The procedural rules, timelines, costs, and strategic options diverge in ways that directly affect your decision. Choosing one over the other should be a deliberate call based on the size and complexity of your claim, not a default.

Arbitration

Arbitration starts with a written demand under your policy’s clause. No lawsuit, no court docket, so timelines are faster compared to civil litigation.

The arbitrator’s award is binding and enforceable. Your insurer cannot simply reject it, though narrow grounds for challenge exist under CPRC § 171. Costs and formality are lower. There is no jury, no extended discovery, and no traditional court filing fees. Demanding arbitration also creates pressure on the insurer to engage seriously instead of stalling.

Litigation

Litigation means filing a lawsuit against your insurer in Texas civil court for car accident claims. It opens up the full discovery process, depositions, and a jury trial if necessary.

Timelines are longer, and costs are higher. For large or complex claims, the extra tools can be worth it. Litigation may also let you pursue a bad faith claim against an insurer that mishandled your case, which is generally not available in arbitration. If you’re unhappy with an arbitration award, your ability to move to court is limited, and it’s important to understand that trade-off before you choose.

Get Legal Help for Your Texas UM/UIM Dispute

A UM or UIM dispute shouldn’t drag on while your medical bills pile up and your wages stay lost. Angel Reyes & Associates has handled Texas UM and UIM disputes and knows how to push insurers that refuse to acknowledge a fair claim. We work on contingency, meaning no fee unless we win, and offer free consultations in English or Spanish so you can get answers before committing to anything.

Our team of attorneys has recovered more than $1 billion for our clients. Contact us today to talk through your claim and decide whether arbitration is the right move for you.

Past results do not guarantee future outcomes.

UI/UIM Insurance Arbitration FAQs

Can an insurer in Texas refuse to participate in arbitration after I submit a written demand?

No. Once you properly invoke the arbitration clause in your policy, your insurer is contractually bound to participate. Texas courts can compel arbitration under CPRC Chapter 171 if the insurer refuses or delays.

Does the statute of limitations still apply if I plan to use arbitration for my Texas UIM claim?

Yes. Texas generally requires you to file a UIM claim within the statute of limitations period, even if you intend to arbitrate rather than litigate. Missing that deadline can bar your right to recover, so it’s important to time your demand before it passes.

Who pays the arbitrator's fees in a Texas UIM arbitration?

Your policy language sets cost allocation, but many Texas auto policies split arbitrator fees between the claimant and the insurer. Reviewing that provision before you demand arbitration helps you budget for the process.

Can the arbitrator award me more than my UIM policy limits?

No. The arbitrator’s award is capped at your policy’s UIM coverage limit, minus any offset for amounts already paid by the at-fault driver’s liability insurer under § 1952.106.

Does a Texas UIM arbitration award appear on any public record?

No. Arbitration proceedings and awards are private and generally not filed with any court unless one party seeks to confirm or vacate the award under CPRC Chapter 171.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...