What Happens When the At-Fault Driver’s Insurance Lapsed Before the Crash?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- A lapsed policy often makes the at-fault vehicle uninsured under the terms dictated by your uninsured motorist policy.

- Texas gives crash victims two years under CPRC § 16.003 to sue an uninsured at-fault driver.

- Your own UM coverage is usually the strongest recovery path after a lapsed-policy crash in Texas.

You were driving home from work on I-35 near downtown Austin when another driver rear-ended you at a red light. The crash report listed their insurance carrier, so you assumed the claim would be straightforward.

Then the insurer called back with a denial: the policy had lapsed weeks before the crash. Now you’re wondering whether you have any path to recovery at all.

What a Lapsed Policy Means for Texas Crash Victims

A lapsed car insurance policy means the at-fault driver stopped paying premiums and their carrier canceled coverage before the crash happened. No active policy means no third-party liability claim is available to you. This is different from an excluded driver, where the policy is active but a specific person is barred from coverage by endorsement.

Texas requires every driver to carry financial responsibility (such as insurance) under the Texas Transportation Code § 601.051. A lapsed policy is a legal violation by the at-fault driver. It does not shift any blame for the crash onto you.

The state minimum liability limits the at-fault driver was supposed to carry under Transportation Code § 601.072 are:

- $30,000 for bodily injury to one person

- $60,000 for bodily injury to two or more persons in one collision

- $25,000 for property damage in one collision

When the policy has lapsed, none of that protection exists for you. The carrier owes you nothing.

Confirm the lapse before you accept a claim denial. Ask the at-fault driver’s last known carrier to send written confirmation of the cancellation date. A coverage denial that turns out to be wrong can change your entire claim path.

How Texas UM Coverage Applies After a Policy Lapse

Your own uninsured motorist coverage becomes the primary recovery tool after a lapsed-policy crash. Texas insurers must include UM and UIM coverage in every automobile liability policy under Texas Insurance Code § 1952.101 — the coverage is part of your policy by default unless you reject it in writing.

When the at-fault driver had no active policy, their vehicle will typically qualify as an uninsured motor vehicle under the terms of your UM policy. The specific definition of what qualifies as “uninsured” is governed by your policy’s language and Texas Department of Insurance-approved forms.

UM is a first-party claim. You file it with your own insurer rather than the at-fault driver’s. You still have to prove the uninsured driver caused the crash and document the full scope of your damages, just as you would in any liability claim.

Expect your own insurer to push back. UM claims are still adversarial, and carriers have a financial reason to pay less. Keep every email, letter, and recorded statement, and save copies of all medical records from day one.

UM and PIP coverage are different. PIP, or personal injury protection, is another first-party source you may have. PIP pays medical bills and a portion of lost wages regardless of fault, which makes it useful while your insurer is processing your UM claim.

Suing the At-Fault Driver Directly in Texas

You have the legal right to sue the at-fault driver even when their insurance had lapsed. Winning a judgment establishes liability on paper. Collecting on that judgment is a separate problem, and often the harder one.

The Texas Civil Practice and Remedies Code (CPRC) § 16.003 gives you two years from the crash date to file. The clock does not pause because you learned about the lapse later. If you aren’t sure how long you have to sue a driver directly or file a UM claim with your insurer, a car accident attorney can help clarify the deadline.

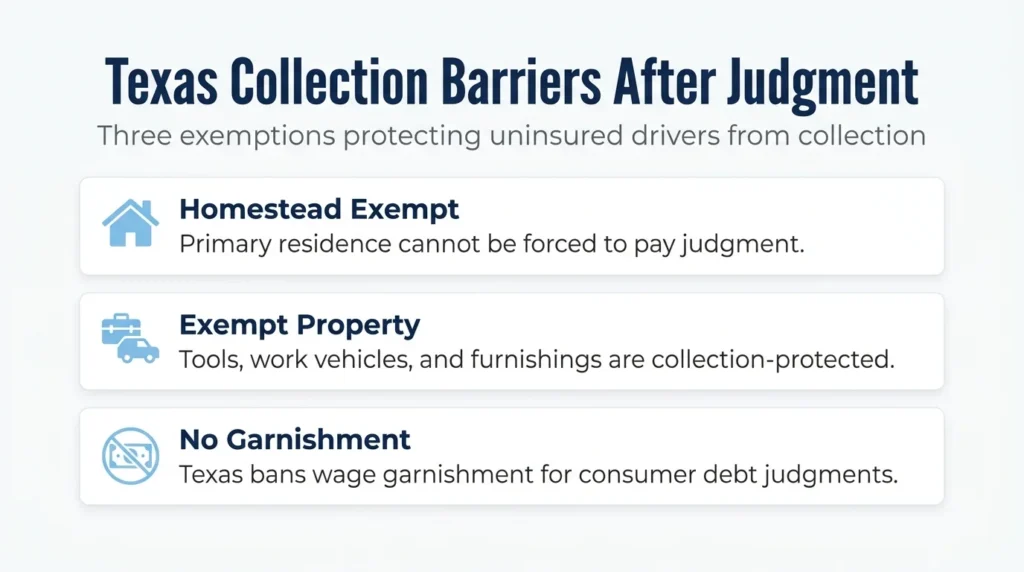

Collection is the central obstacle. Texas law shields a lot of assets from civil judgment creditors:

- The homestead exemption protects the driver’s primary residence from forced sale.

- Exempt personal property covers tools of the trade, work vehicles, and household furnishings.

- Wage garnishment for consumer debts is not allowed in Texas.

A driver who chose to skip insurance is often judgment-proof by the time of trial. Contingency-fee attorneys frequently decline direct suits for this reason and focus on the UM path instead. You can pursue both simultaneously, but a UM recovery typically offsets what a direct judgment can yield. An attorney can help you sequence the two without losing leverage.

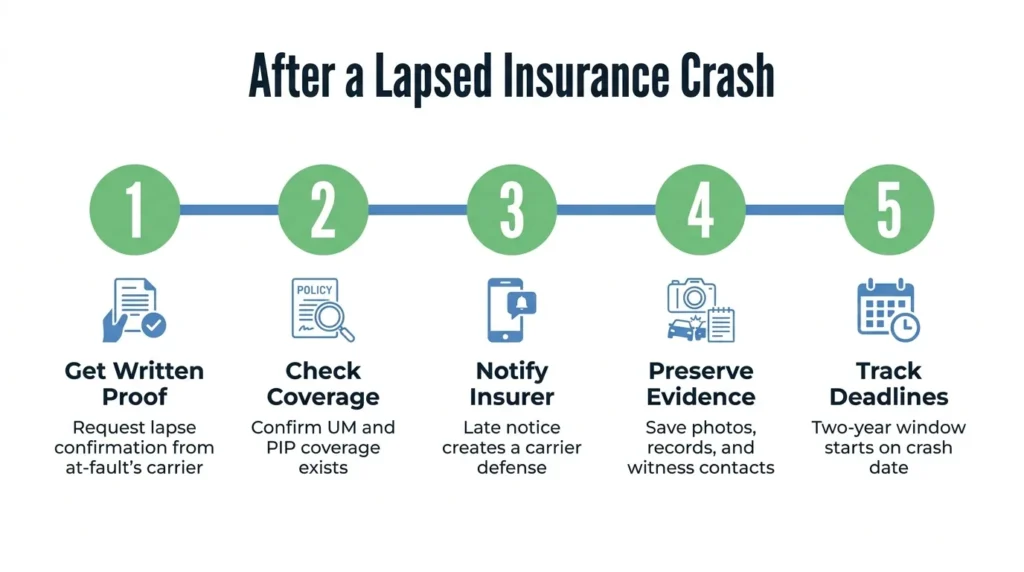

Steps to Take After a Lapsed-Insurance Crash

Move quickly once you learn the policy had lapsed. The actions you take in the first weeks after an accident with an uninsured driver shape what you can recover later. Five steps cover the early phase:

- Get the crash report and request written confirmation of the cancellation date from the at-fault driver’s last known carrier.

- Pull your own declarations page and confirm whether you carry UM and PIP coverage. If you don’t, check whether you signed a written rejection when you bought your policy, which Texas law requires.

- Notify your own insurer of a potential UM claim promptly. Late notice can give the carrier a coverage defense.

- Preserve evidence on your own: photos, witness contacts, medical records, pay stubs, and every message from the at-fault driver.

- Track the two-year filing deadline for both the UM claim and any direct suit. Policy deadlines and statutory deadlines are not always the same.

An attorney can also send preservation letters to insurers and tow yards before critical records are overwritten.

Talk to a Texas Attorney About Your Options

A lapsed-policy crash is one of the most frustrating situations a Texas driver can face, but it’s not the end of the road. Angel Reyes & Associates has over 30 years of experience handling Texas car accident claims, including UM disputes and direct suits against uninsured drivers. We have more than $1 billion recovered for clients, and our client testimonials reflect that work.

Consultations are free, and we work on contingency, meaning no fee unless we win. The two-year deadline is already running. Contact us today to talk through your options before that window closes.

Past results do not guarantee future outcomes.

Lapsed-Policy Accident FAQs

Does a lapsed policy on the at-fault driver's vehicle affect how property damage to my car is handled?

If you carry collision coverage on your own policy, you can file a collision claim for vehicle damage regardless of whether the at-fault driver had active insurance. A UM property damage claim is a separate option if you have that specific coverage and did not carry collision.

Will filing a UM claim after a lapsed-policy crash raise my own insurance rates in Texas?

Texas law does not prohibit insurers from considering a UM claim when setting rates, though many carriers treat first-party UM claims differently than at-fault collision claims. Reviewing your policy or asking your insurer directly before filing is the most reliable way to understand the rate impact.

Can a lapsed policy be reinstated retroactively to cover a crash that already happened?

Insurers do not reinstate lapsed policies to cover losses that occurred after the cancellation date. Retroactive reinstatement would require the carrier to assume liability for a known loss, which policy terms and Texas insurance law don’t permit.

What does it mean that the at-fault driver's vehicle must make "physical contact" for some UM claims in Texas?

Texas UM policies often require physical contact when the at-fault driver is unknown, such as in a hit-and-run. In a lapsed-policy crash where the driver is identified, the physical contact requirement typically does not apply because the responsible party is known.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...