Motor Carrier Insurance Requirements: Federal FMCSA vs Texas Intrastate Rules

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- FMCSA financial responsibility requirements apply to interstate carriers, while TxDMV rules govern Texas intrastate operations, and many fleets must comply with both.

- Minimum insurance requirements are compliance floors, not guarantees that a crash claim will be fully covered.

- Serious truck accident claims often involve layered coverages that require careful investigation to identify all available compensation sources.

You were hit by an 18-wheeler on I-10 near Katy last month. The trucking company’s adjuster mentioned something about “minimum coverage” and “FMCSA filings.” Now you’re wondering whether the insurance they carry will actually cover your medical bills and lost wages.

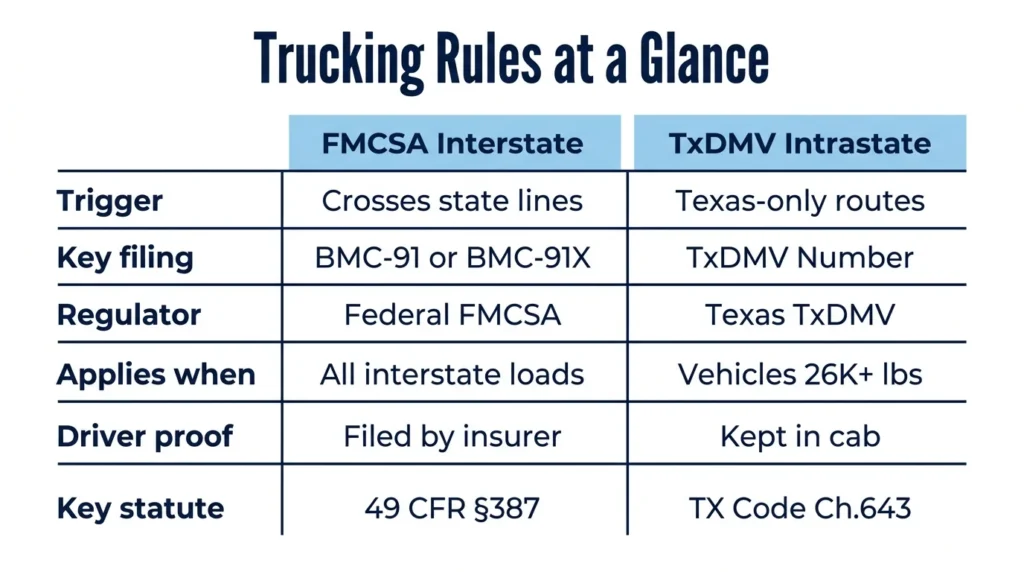

Texas trucking operations often fall under two separate regulatory systems. Federal rules from the FMCSA govern interstate carriers. Texas rules through TxDMV apply to intrastate operations. Some fleets answer to both. Understanding which requirements apply helps you know what coverage might be available after a serious crash.

Why Motor Carrier Insurance Rules Create Confusion

The phrase “minimum required insurance” misleads many people. A trucking company can meet every legal requirement and still carry coverage that falls short of what a catastrophic injury claim demands.

The “minimum required” amount is a compliance floor, not a guaranteed payout. Policies contain exclusions. Coverage can be disputed. Layered insurance programs involve multiple carriers with different responsibilities. Self-insured retentions can delay access to funds.

Two distinct regulatory buckets exist for Texas trucking operations:

- FMCSA financial responsibility requirements for interstate carriers, including specific filings and endorsements

- TxDMV intrastate minimums and proof-of-insurance mechanics for carriers operating only within Texas

Many Houston-area fleets hauling freight between the Port of Houston and distribution centers in Sugar Land or The Woodlands operate under both systems. A carrier registered with TxDMV might also hold federal operating authority for loads crossing into Louisiana or Oklahoma.

Determining Which Rules Apply to Your Situation

Before discussing dollar amounts or filing forms, you need to classify the operation correctly.

Interstate operations trigger FMCSA requirements. This generally means movement across state lines or transportation that is part of interstate commerce. The legal definitions can be fact-specific, and some movements that seem purely local may still qualify as interstate under federal law.

Intrastate operations in Texas require registration with TxDMV when certain thresholds are met. According to TxDMV, you need a TxDMV Number if you operate:

- A commercial motor vehicle weighing more than 26,000 pounds

- A vehicle transporting placarded hazardous materials

- A vehicle designed to carry more than 15 passengers

- A vehicle transporting household goods for compensation

Carriers based in Texas often do both. A San Antonio trucking company might haul construction materials locally on Loop 1604 while also running loads to New Mexico. That fleet needs to satisfy both TxDMV and FMCSA requirements.

Documents to Gather Before Calling Your Insurer or Attorney

If you’re investigating coverage after a crash or checking your own compliance, collect:

- MC number, USDOT number, and TxDMV number (these appear on cab doors and registration documents)

- Insurance policy declarations pages showing coverage limits and effective dates

- Any excess or umbrella policy schedules

- Self-insured retention documentation if applicable

- Information about cargo type, vehicle weight, and passenger capacity

Federal FMCSA Financial Responsibility Requirements

FMCSA requires interstate motor carriers to demonstrate “financial responsibility” as a condition of operating authority. This is a compliance requirement tied to your ability to legally operate. It is not a promise that every crash claim gets paid in full.

FMCSA minimums vary by operation type. Carriers hauling general freight face different requirements than those transporting hazardous materials or passengers. The specific minimum depends on what the carrier hauls and how many passengers they transport.

Meeting FMCSA financial responsibility is typically demonstrated through filings made by insurance companies or financial institutions. Carriers do not file these forms themselves. According to FMCSA guidance, insurers must submit proof of financial responsibility electronically.

This filing status is very important after a crash. Investigators can verify coverage, identify responsible insurers, and confirm whether the carrier’s authority was active at the time of the collision. The procedures for these filings are outlined in 49 CFR § 387.313.

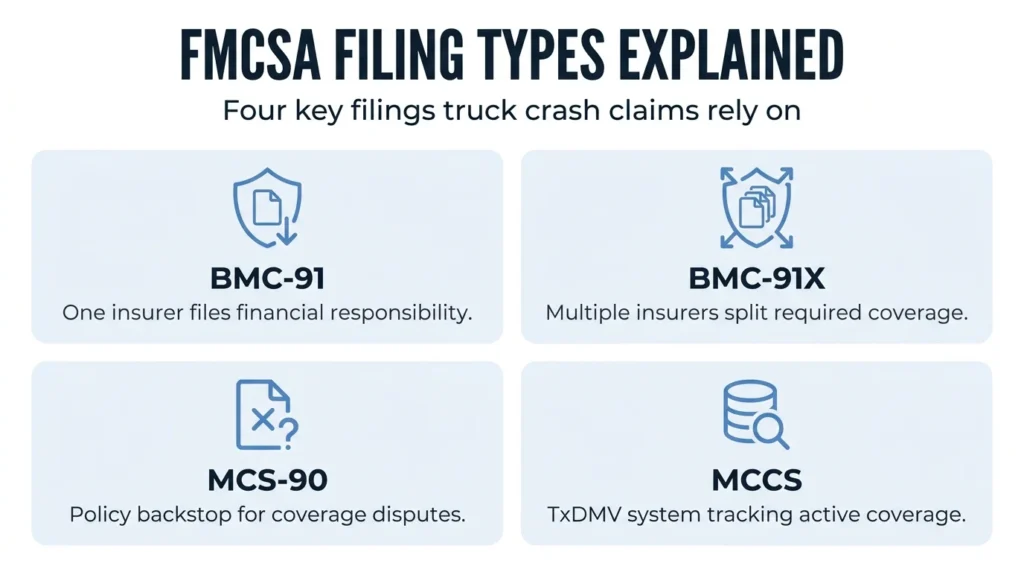

Understanding BMC-91, BMC-91X & MCS-90

These terms appear frequently in truck accident cases. Understanding what they mean helps clarify what coverage might exist.

BMC-91 and BMC-91X are FMCSA filing forms used to show proof of financial responsibility. They are not insurance policies themselves. The BMC-91 is typically used when a single insurer provides the required coverage. The BMC-91X applies when multiple insurers participate in providing the required coverage amount.

The MCS-90 is an endorsement attached to certain motor carrier policies. It functions as a financial responsibility backstop in specific situations. The MCS-90 can become relevant when a policy might otherwise deny coverage for a particular claim. Whether it applies depends on the specific facts of each case.

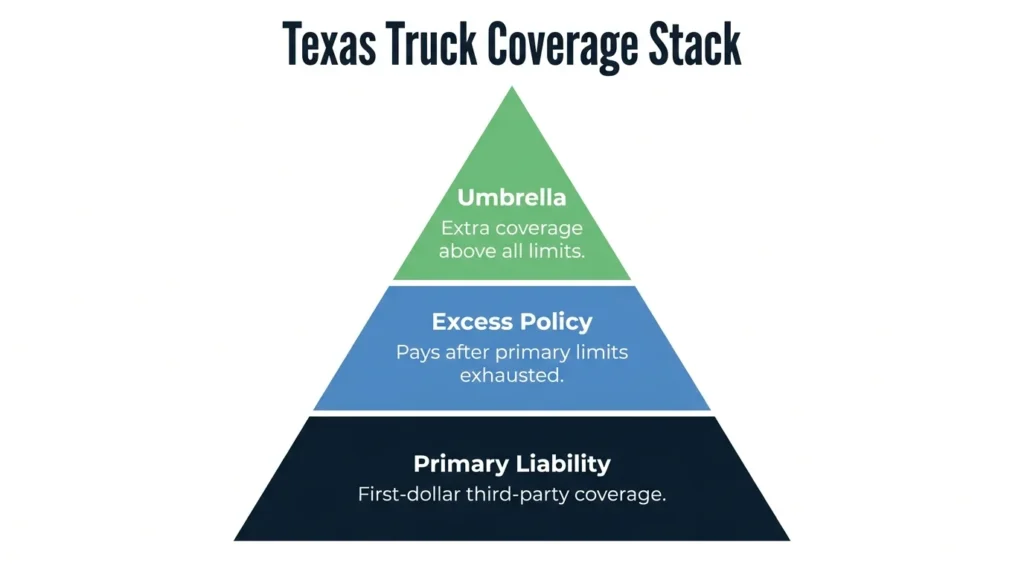

For fleets with layered insurance programs, a crash investigation may need to identify multiple policies. A carrier might have primary auto liability coverage, an excess policy, and an umbrella policy. Each layer may involve different insurers with different claim-handling procedures.

If you’ve been injured in a truck crash, identifying all potential coverage sources requires careful investigation. An experienced truck accident attorney can help trace these coverage layers.

Texas Intrastate Motor Carrier Minimums

Texas Transportation Code Chapter 643 establishes the framework for intrastate motor carrier registration and insurance requirements. Chapter 643 requires carriers to file evidence of insurance and maintain proof in the vehicle.

TxDMV publishes specific minimum insurance amounts based on carrier type. These vary depending on:

- Vehicle weight

- Whether the carrier transports hazardous materials

- Passenger capacity

- Whether the carrier moves household goods

The TxDMV motor carrier page provides the current minimum amounts and explains which forms insurers must file.

Keeping Coverage Active in the TxDMV System

Having a policy is not the same as having it properly filed and active. TxDMV requires that coverage remain active in their Motor Carrier Credentialing System (MCCS). If coverage lapses or filings are not updated, the carrier’s registration can become inactive.

Common compliance pitfalls include:

- Policy cancellation without replacement coverage being filed

- Mismatch between names on the policy and TxDMV registration

- Vehicle additions or changes not updated in the system

- Failure to maintain proof of insurance in the cab during operations

Enforcement officers on Texas highways can verify insurance status. Operating without proper coverage or proof can result in penalties and operational shutdowns.

How Minimums Affect Real Truck Crash Claims

Serious truck crashes often produce damages that exceed minimum coverage requirements. Medical bills, lost income, and long-term care needs can quickly surpass policy limits. This is where understanding coverage layers becomes critical.

The coverage stack concept explains how multiple policies may apply:

- Primary liability coverage pays first, up to its limits

- Excess coverage kicks in after primary limits are exhausted

- Umbrella policies may provide additional protection above underlying coverage

A self-insured retention (SIR) works differently than a deductible. With an SIR, the carrier pays claims out of pocket up to a certain amount before insurance responds. This can affect early claim negotiations and the timeline for accessing insurance funds.

Cargo coverage is separate from liability coverage. Liability coverage protects against claims from injured third parties. Cargo coverage protects the freight being hauled. If you were injured in a crash, cargo coverage is generally not relevant to your claim. If your goods were damaged during transport, cargo coverage may apply.

Coverage Questions to Ask After a Crash

After a truck collision on Westheimer Road or anywhere else in Texas, several coverage questions need immediate attention:

- Which entities might be responsible? (carrier, driver, broker, shipper, maintenance provider)

- What policies exist beyond the primary auto liability coverage?

- Are FMCSA and TxDMV filings current and accurate?

- Do the filings match the actual policy terms?

Preserving evidence quickly is essential. Leasing agreements, insurance certificates, and maintenance records can all become relevant. An attorney experienced with commercial truck crashes can help identify all potential sources of recovery.

Getting Help After a Texas Truck Accident

Navigating motor carrier insurance requirements is complicated. Federal and state rules overlap. Coverage is often layered across multiple policies. Insurance companies work to minimize payouts.

At Angel Reyes & Associates, we have over 30 years of experience handling serious truck accident cases across Texas. We’ve helped clients recover compensation from complex insurance arrangements involving multiple carriers and coverage layers. Our firm has recovered more than $1 billion for clients, and we offer free consultations with no fee unless we win.

If you or a family member was injured in a truck crash, understanding the insurance landscape is the first step toward fair compensation. Contact us today to discuss your situation and learn what coverage may be available for your claim.

Federal & Intrastate Insurance Requirement FAQs

Does a Texas intrastate carrier still need federal filings if it occasionally takes an out-of-state load?

Maybe. Even occasional interstate operations can trigger federal authority and FMCSA financial responsibility requirements, so the answer depends on how the carrier actually operates and what shipments are part of interstate commerce.

Is a certificate of insurance enough to prove a trucking company has the right coverage?

Not always. A certificate is only a summary and usually does not change the policy terms, so lawyers and insurers often need the actual policy, endorsements, and filed forms to confirm what coverage really applies.

Does cargo insurance pay for injuries after a truck accident?

Usually no. Cargo insurance is meant to protect the freight being hauled, while bodily injury and property damage claims are generally handled under liability coverage.

What happens if the trucking company’s policy was active, but the state or federal filing was missing or inactive?

That can create major disputes about compliance and coverage verification, but it does not automatically answer whether a specific claim will be paid. The policy language, endorsements, and the facts of the crash are still important.

Can more than one trucking company’s insurance apply to the same crash?

Yes. Depending on the lease arrangement, trip documents, and who controlled the load, coverage may involve the motor carrier, an owner-operator, or other companies tied to the shipment.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...