U-Haul and Rental Truck Accident Claims in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- In a rental truck crash, the renter is primarily liable; whether insurance covers that liability depends on what supplemental protection they purchased at the counter.

- Most personal auto policies and credit card rental protection exclude large moving trucks. If you were injured, you may need to rely on your own uninsured motorist coverage.

- The Graves Amendment limits vicarious liability suits against rental companies, but claims based on negligent maintenance or negligent entrustment are still viable in Texas.

You rented a U-Haul to move from East Austin to SoCo, and now you’re dealing with a crash and a rental agreement full of fine print. Or you were hit by someone else’s rental truck on I-35 and have no idea whether to call the rental company, the driver’s insurer, or your own provider.

The coverage chain for rental truck accidents in Texas is different from a standard crash, and knowing which link applies to your situation is the first step.

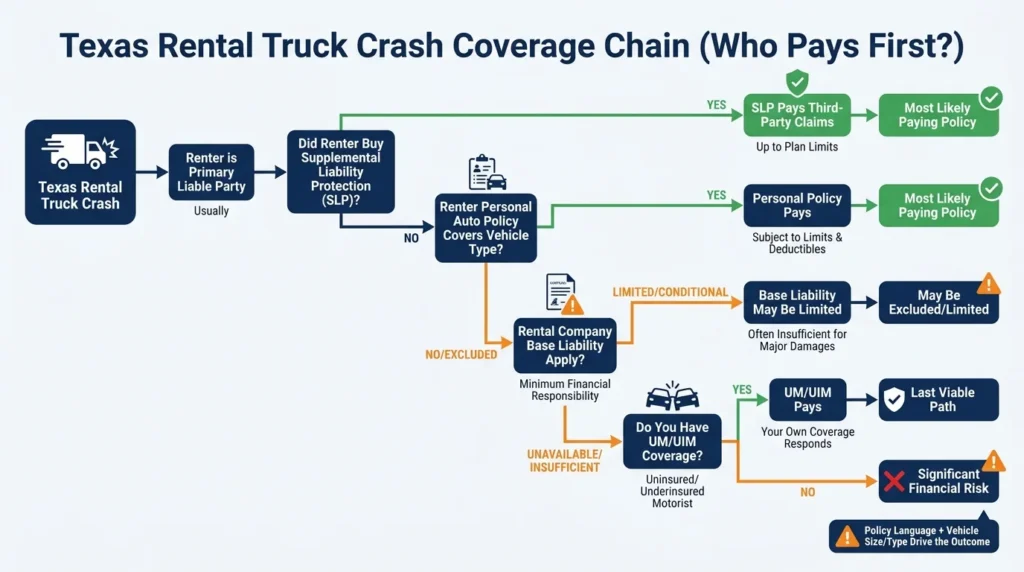

Who Pays After a Rental Truck Crash

In a rental truck crash in Texas, the renter is the primary liable party. Whether there’s insurance to pay that liability depends on three things:

- What supplemental protection the renter purchased from the rental company

- Whether the renter’s personal auto policy extends to the vehicle type

- Whether the rental company’s own base liability coverage applies

Car and truck accident claims are different, but when a rental truck driver causes a crash, they bear the same legal duty any negligent driver bears under Texas law. The question is not usually whether they are liable. The question is which insurance will actually pay the resulting claim.

If the renter bought supplemental liability protection at the counter, that coverage activates for third-party claims. If they declined it, the renter’s personal auto insurance becomes the fallback. When neither applies, the injured person’s own uninsured motorist coverage may be the only remaining option.

The Coverage Chain for Rental Trucks

Rental companies maintain liability insurance on their fleets, but that base coverage often functions as a last resort. Supplemental Liability Protection, which renters can purchase at the counter, provides the most direct path to coverage for third-party injuries. What the renter signed, and what they declined, determines which layer of coverage responds first.

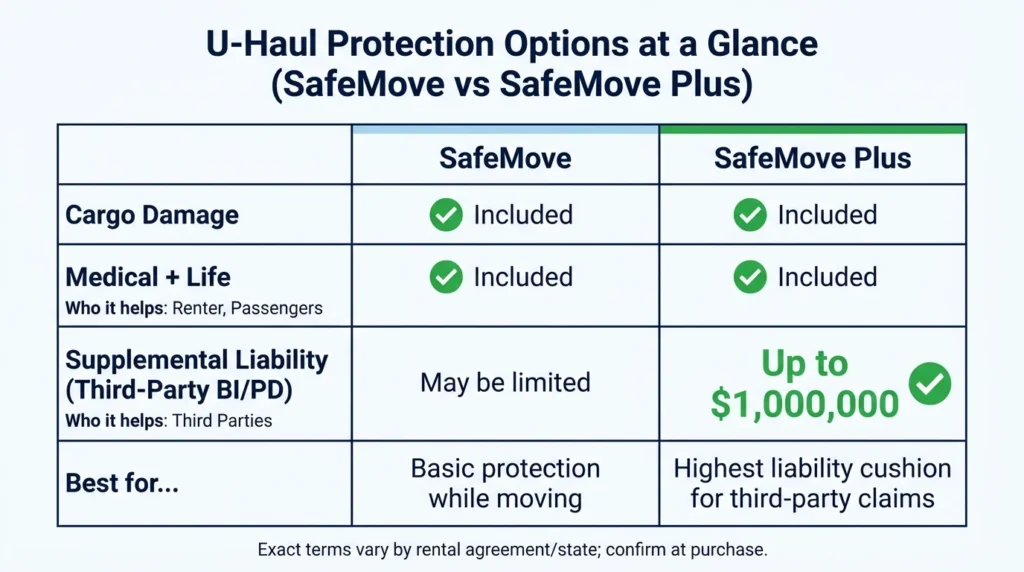

U-Haul’s SafeMove Plus plan is the most comprehensive option the company offers. It covers cargo damage, medical and life benefits for the renter, and supplemental liability coverage for third-party bodily injury and property damage. SafeMove Plus supplemental liability coverage can reach $1,000,000, making it the most significant coverage layer for injured third parties.

When the renter purchased only the basic SafeMove plan or no coverage at all, the injured person faces a thinner coverage stack. The rental company’s base fleet liability policy may provide some protection, but limits and conditions vary.

Texas requires all motor vehicles operated on public roads to meet minimum financial responsibility requirements under Texas Transportation Code § 601.072. Rental companies must comply with these minimums, but satisfying them does not guarantee coverage is available for a specific crash.

The step-by-step timeline of a Texas truck accident claim outlines how coverage questions like these typically surface during the claims process and when to expect answers.

When Personal Auto Insurance Falls Short

Most personal auto policies do not extend to large rental trucks. Policies that cover borrowed or rented vehicles typically apply to vehicles of a similar size to the insured’s personal car. A 26-foot moving truck is almost universally excluded, and even smaller moving vans often fall outside the policy’s coverage terms.

The exclusion matters in two scenarios:

- If you were the renter and caused the accident, your personal policy may refuse the claim.

- If you were hit by a renter with no supplemental coverage, their personal insurer may not cover your losses.

Credit card rental protection, which many people treat as a fallback, almost always excludes trucks, vans, and cargo vehicles. Most major card agreements specify that protection applies to passenger vehicles only.

When neither supplemental protection nor personal coverage applies, you may need to file under your own car accident coverage, specifically uninsured or underinsured motorist protection. Understanding how Texas truck accident claims work gives you a clearer picture of what to pursue and in what order when coverage layers are thin or missing.

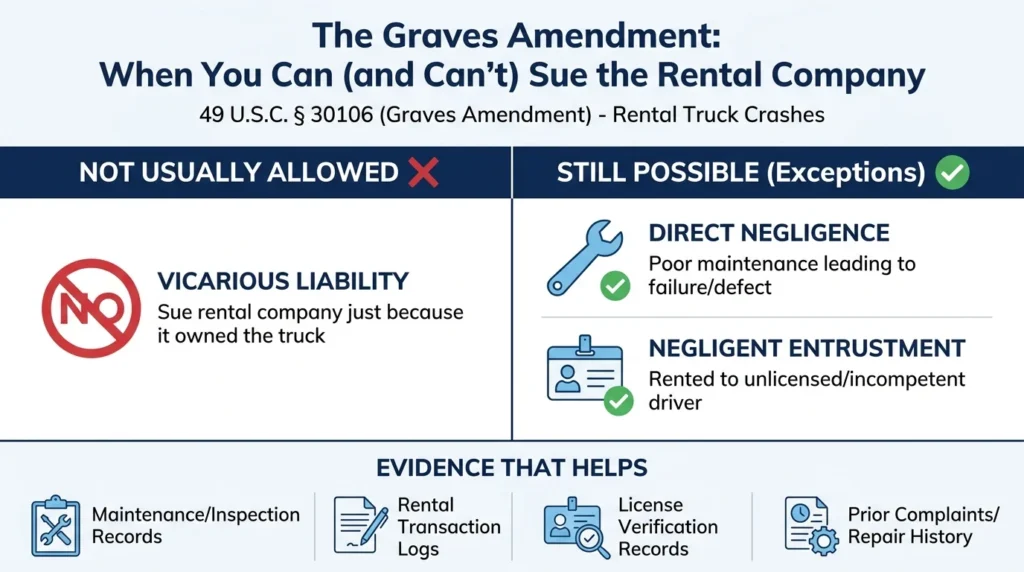

What the Graves Amendment Means for Your Claim

The Graves Amendment is a federal law that generally prevents injured parties from suing a rental company simply because it owned the truck involved in a crash. The law bars vicarious liability claims against rental companies in the business of renting vehicles. It does not bar claims based on the rental company’s own negligence.

The statute, 49 U.S.C. § 30106, was enacted in 2005 and preempts state laws that previously allowed injured parties to hold a rental company responsible solely by virtue of ownership.

Two exceptions remain:

- Direct negligence: If U-Haul improperly maintained the truck and a brake failure or mechanical defect contributed to the crash, the company remains liable for its own conduct.

- Negligent entrustment: If U-Haul rented a truck to a driver it knew or should have known was incompetent or unlicensed, it may face liability for that decision under Texas law.

Pursuing a direct claim against a rental company requires documentation that goes beyond the crash report. Maintenance records, rental transaction logs, license verification records, and the truck’s inspection history are all relevant to building your case.

When the rental company’s own conduct contributed to a crash, truck accident claims involving commercial vehicles follow the same investigative framework as other commercial crash cases.

Work with a Texas Injury Attorney

Rental truck accident claims involve a coverage chain that most adjusters will not explain in your favor. Angel Reyes & Associates has handled Texas vehicle accident claims for over 30 years. We’re available 24/7 and offer service in English and Spanish.

Our attorneys work on contingency: You pay no fee unless we win. Contact us for a free consultation to discuss the facts of your rental truck accident case.

Past results do not guarantee future outcomes.

Witness Statement FAQs

If I was a passenger in the rental truck, am I covered by the renter's supplemental protection?

U-Haul’s SafeMove and SafeMove Plus plans include medical and life coverage for the renter and passengers in the rented truck. If the renter didn’t purchase supplemental coverage, you must pursue compensation through the at-fault driver’s personal insurance, the rental company’s base policy, or your own medical coverage.

What if I rented the U-Haul and another driver hit me—does U-Haul's plan cover my injuries?

SafeMove Plus includes a medical and life protection component for you as the renter, which can apply when you’re injured, regardless of fault. If you declined supplemental coverage, your recovery typically depends on the at-fault driver’s insurance or your own personal auto policy’s medical payments coverage.

Are large U-Haul moving trucks subject to FMCSA commercial vehicle regulations?

U-Haul trucks used for personal household moves are generally not operated as commercial motor carriers under FMCSA rules, so federal hours-of-service and electronic logging device requirements don’t apply. However, if you use a rental truck for a commercial purpose in interstate commerce, FMCSA regulations may become relevant to how the crash is investigated.

How long do I have to file a personal injury claim after a rental truck accident in Texas?

Texas law gives you two years from the date of the crash to file a personal injury lawsuit under the Texas Civil Practice and Remedies Code § 16.003. Missing that deadline generally bars you from recovery, regardless of the strength of your claim.

What if cargo fell from the rental truck and damaged my vehicle or caused the crash?

Liability for unsecured cargo typically falls on the person who loaded and secured the truck, which is usually the renter. If the cargo restraint equipment U-Haul provided was defective, the rental company may bear responsibility for that failure under a negligent maintenance or product liability theory.

About the Authors

Spencer Browne

Writer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials across Texas. He focuses on car, truck, and wrongful death cases, with notable verdicts including a landmark win in the Choctaw Casino bus crash case. A recognized speaker and legal educator, Spencer is a member of the American Board of Trial Advocates and has been honored as a Texas Super Lawyer and one of D Magazine’s Best Lawyers in Dallas. He brings deep trial experience and relentless advocacy to every client he represents.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...