Stacking UM/UIM Policies in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas allows inter-policy UM/UIM stacking but prohibits multiplying limits within a single policy.

- Anti-stacking clauses are only binding when the policy wording is clear.

- Household members may stack a second UM/UIM policy if they qualify as a covered person.

You were driving home on I-35 near Round Rock when a driver drifted across the line and clipped your front quarter panel. The other driver carried the state minimum coverage, and the offer from their insurer barely covers your ER bill. Your own policy has UM/UIM coverage, and so does your spouse’s. Can you combine them?

What Stacking UM/UIM Policies Means

Stacking means combining the coverage limits of two or more separate UM/UIM policies, so the total available benefits exceed what any single policy would pay alone. It comes into play when the at-fault driver has no insurance or not enough insurance, and one UM/UIM policy cannot cover the difference between the settlement offer and your actual losses.

Texas auto insurers must provide UM/UIM coverage on every auto liability policy issued in the state under Texas Insurance Code § 1952.101 unless the named insured rejects the coverage in writing. That means most drivers already have at least one UM/UIM policy to rely on after a crash.

Whether you can stack a second policy on top of the first hinges on two questions:

- The type of stacking

- What your policy language says

The underlying problem is common. Uninsured and underinsured drivers crowd Texas roads, and according to the Insurance Information Institute, industry data on uninsured motorists shows that roughly one in seven U.S. drivers carries no coverage at all. Stacking insurance coverage is often the only way to cover the difference between a small liability payout and the bill for a serious injury. Our guide to uninsured motorist accidents explains the entire claim process.

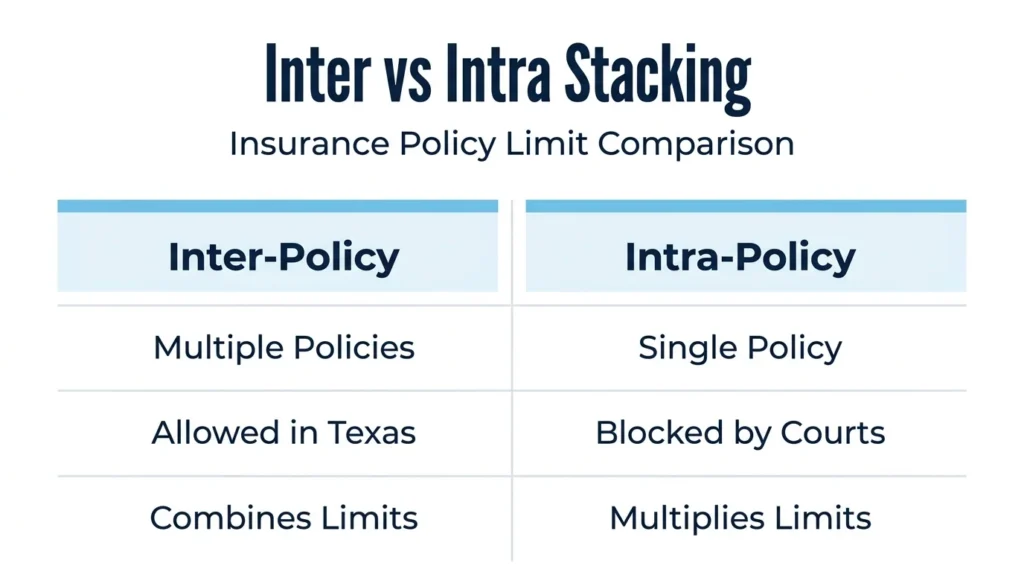

Inter-Policy vs. Intra-Policy Stacking in Texas

Texas treats these two forms of stacking very differently. Inter-policy stacking combines limits across separate policies and is generally allowed. Intra-policy stacking tries to increase insurance limits within one policy based on the number of insured vehicles, but this is not allowed.

Inter-Policy Stacking

Inter-policy stacking combines limits from two or more separate and distinct policies. If you have a $30,000 UM/UIM policy, and you also qualify as a covered person under a household member’s $30,000 UM/UIM policy, then you may be able to access up to $60,000 in combined limits. Texas courts have allowed this approach when the policy does not contain valid anti-stacking language.

Inter-policy stacking is not automatic. You must identify each applicable policy and file a claim under each one. Passengers injured in a crash often have access to more policies than they realize.

Intra-Policy Stacking

Intra-policy stacking tries to increase insurance limits within one policy based on the number of insured vehicles, but this is not allowed in Texas courts.

Having a single policy that covers three vehicles does not give you three separate coverage limits stacked together. The per-person and per-occurrence limits apply only once per accident. This rule is not directly stated in Chapter 1952 of the Insurance Code; instead, it comes from how Texas courts interpret the policy terms. The difference is small but important. Texas restricts your ability to multiply the limits within one insurance policy, but it does not block you from combining limits across several separate policies.

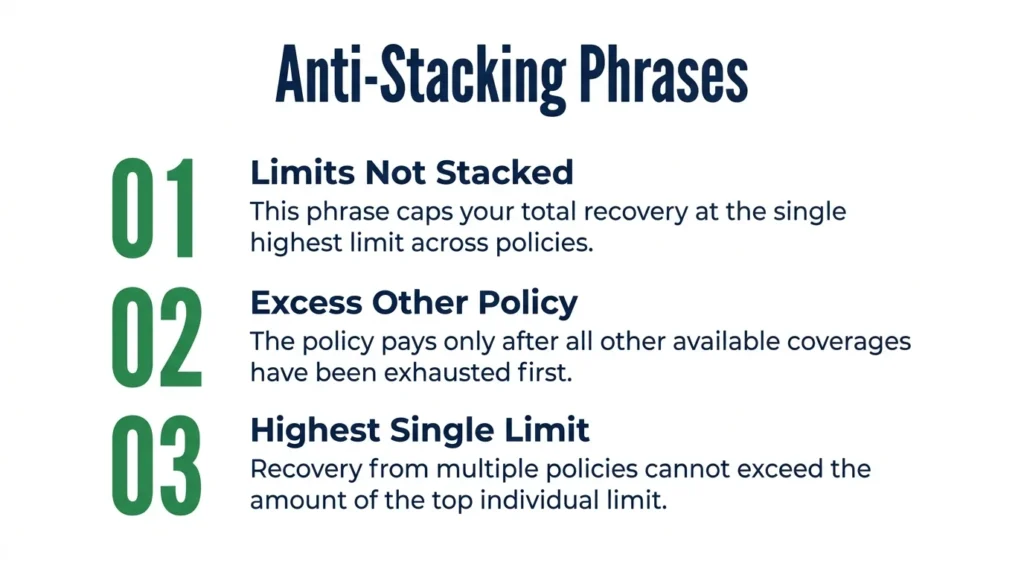

Anti-Stacking Clauses

An anti-stacking clause is policy language that limits the insurer’s obligation at the highest coverage amount available under one policy. It also excludes coverage if another policy is already covering the same loss.

Texas courts enforce these clauses, but only when the wording is clear. Vague or contradictory language may not stop someone from trying to stack coverage. For example, many policies hide an anti-stacking provision inside a clause that points to “other insurance.” This clause typically states that the policy only pays after “other insurance” is used first, or that your recovery cannot exceed the highest coverage amount available under one policy.

When you read your policy, look at the UM/UIM declarations page and watch out for phrases such as:

- “Limits shall not be stacked.”

- “This policy is excess over any other applicable policy.”

- “Maximum recovery shall not exceed the highest single limit available.”

The absence of clear anti-stacking language will strengthen your case for combining policies. The Texas Department of Insurance auto insurance guide clearly explains policyholder rights, including UM/UIM coverage basics.

An attorney can read the exact policy wording and tell you whether the anti-stacking language in your contract would survive a Texas court’s scrutiny. Our breakdown of UM/UIM and PIP coverage explains how these coverages interact in a typical claim.

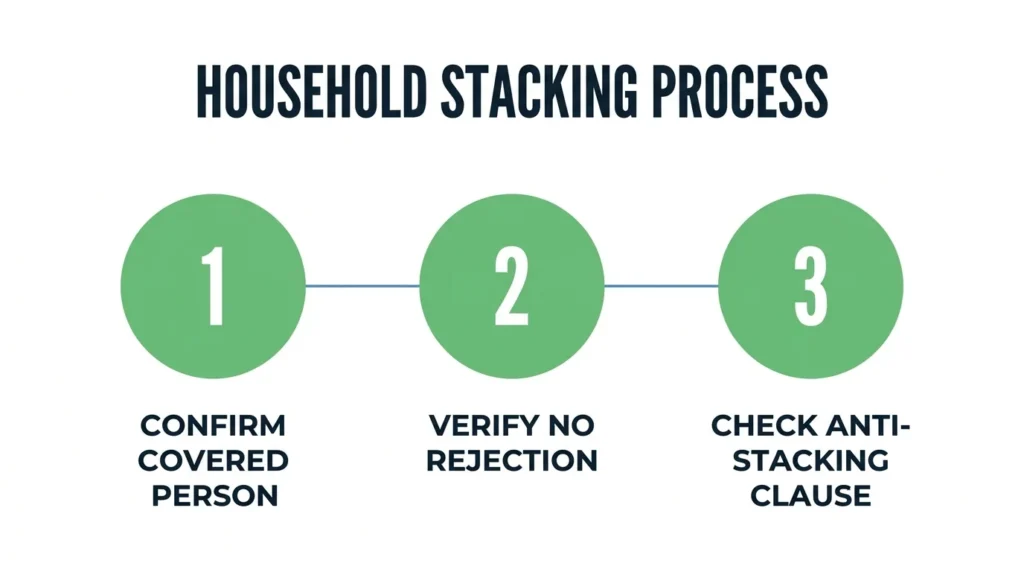

Household Policies

Many Texas drivers qualify for UM/UIM coverage under more than one policy. Your own auto policy may cover you, and a spouse’s or resident relative’s auto policy may extend coverage to you, as well. When both policies apply to the same crash, stacking those limits may cover the difference.

Start by working through the household coverage issue in three steps:

- Confirm that you qualify as a covered person under the household member’s policy.

- Confirm that UM/UIM coverage was not rejected in writing when their policy was issued.

- Check whether their policy contains enforceable anti-stacking language.

Remember, the definition of “covered person” varies by policy. Most policies extend coverage to relatives and household members who live with you, but the declarations page and the definitions section will confirm who actually qualifies. You do not need to file a lawsuit to stack household policies if the language is clear. Send a demand letter to each insurer separately along with the same medical records, wage documentation, and crash evidence.

Texas Insurance Code § 1952.106 explains that any amount you recover from the at-fault driver’s insurer is deducted from your UM/UIM payout. When you stack multiple policies, each policy may apply its own deduction rules, which can change your net recovery amount. Our article on going above the minimums with UM/UIM and PIP explains why it’s important to have higher coverage before a crash ever happens.

Talk to an Attorney About Stacking UM/UIM Policies in Texas

Stacking claims depend entirely on policy wording. Spotting every applicable policy, reading the anti-stacking and “other insurance” clauses correctly, and pursuing claims against multiple insurers at once is hard work. Angel Reyes & Associates has over 30 years of experience handling Texas UM/UIM claims, with more than $1 billion recovered for clients.

You can review our case results to see how we approach complex coverage questions. Consultations are free, and we work on contingency, so there is no fee unless we win. Contact us today to discuss whether stacking applies to your claim.

Past results do not guarantee future outcomes.

Frequently Asked Questions

Can I stack UM/UIM coverage from a commercial or rideshare policy with my personal auto policy in Texas?

Sometimes. It depends on whether you qualify as a covered person under both policies, and whether either policy contains clear anti-stacking language. Rideshare and commercial auto policies often define covered persons more strictly than personal policies, so eligibility varies according to the contract terms.

Does Texas require insurers to notify me if my policy has an anti-stacking clause?

No, Texas law does not require a separate notice specifically for anti-stacking provisions. The clause is typically buried in the UM/UIM endorsement or the “other insurance” section, so you will have to read those portions of your policy to know whether the clause exists.

Does a written rejection of UM/UIM coverage by one household member affect another household member's ability to stack that policy?

Yes. If the named insured on a policy rejected UM/UIM coverage in writing, then that coverage is not available for anyone under that policy, including other household members who might otherwise qualify as covered persons.

How does the two-year statute of limitations in Texas apply when stacking claims against multiple insurers?

Texas generally gives you two years from the date of the crash to file a UM/UIM lawsuit, and that deadline applies to each insurer separately. Filing a claim with one insurer does not pause the clock on a stacking claim against a second insurer.

Can a minor child injured in a household vehicle stack UM/UIM coverage from both parents' separate policies?

Most likely. A minor child who qualifies as a resident relative under both parents’ policies may be eligible to pursue claims under each, as long as neither policy contains enforceable anti-stacking language that restricts this combination.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...