Dealing with Insurance After a Motorcycle Accident

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Insurer bias against riders is real: adjusters inflate fault to cut payouts under Texas proportionate responsibility law.

- You are not required to give a recorded statement to the other driver's insurance company.

- Texas gives you two years from the crash date to file a personal injury lawsuit under CPRC § 16.003.

You were heading home on the Katy Freeway when a driver changed lanes without signaling and clipped your front wheel. You went down, your bike is totaled, and your shoulder hasn’t felt right since. Now the at-fault driver’s insurance company is already calling.

What you say next, and what you agree to, can shape how much compensation you recover.

Why Motorcycle Claims Trigger More Insurer Pushback

Motorcycle accident claims are harder to resolve than car accident claims, and the reason isn’t the law. It is the bias adjusters bring to the process.

Insurance adjusters often assume motorcycle riders contributed to crashes. They reach for common stereotypes: speeding, weaving, riding aggressively. That assumption influences how adjusters evaluate claims from the first phone call, and it shapes what they offer.

Texas uses a fault-sharing system called proportionate responsibility. Under Texas Civil Practice and Remedies Code (CPRC) Chapter 33, if you are found more than 50% at fault for the crash, you recover nothing. Insurers know this rule. Pushing your fault percentage above 50% is a direct path to paying you zero, and anti-rider bias is the tool they use to get there.

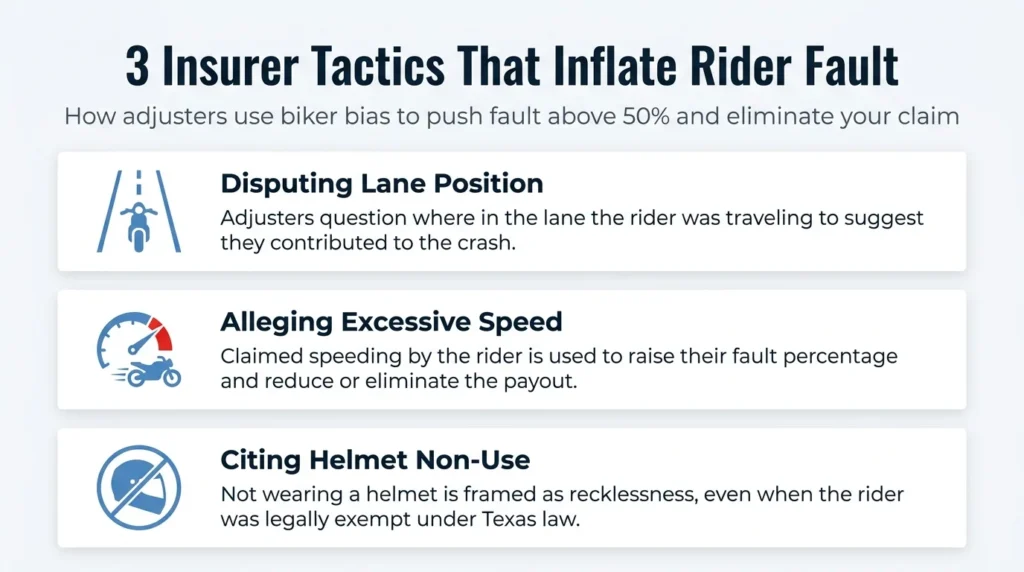

Common tactics include:

- Disputing your lane position

- Arguing you were speeding

- Raising helmet use as evidence of recklessness

None of these arguments automatically reduce your claim, but they create enough uncertainty to justify a lower offer or a denial. Knowing this going in is the first step toward protecting yourself. Understanding how Texas motorcycle accident cases develop and what coverage issues you could face helps you prepare.

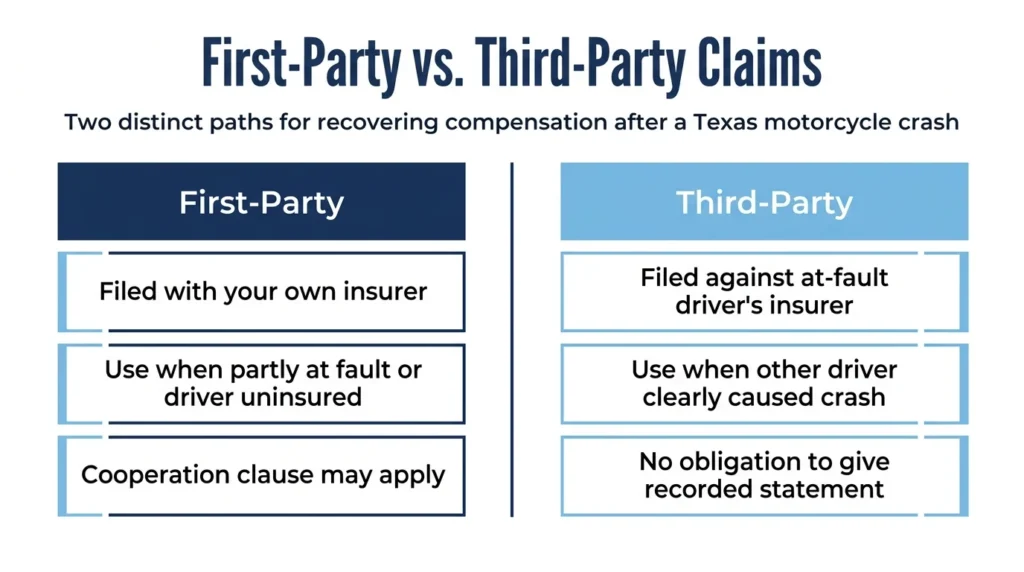

First-Party vs. Third-Party Claims Explained

The first decision after a crash is which insurer to call. You might not realize that there are two separate paths, and choosing the wrong one can slow down your recovery.

First-Party Claims

A first-party claim is filed with your own insurance company using the coverage in your own policy. This is the right path when you bear some fault for the crash, when the other driver has no insurance, or when their policy limits aren’t enough to cover your injuries.

Your own policy may include collision coverage for bike damage, MedPay for immediate medical bills regardless of fault, and UM/UIM coverage for crashes with uninsured or underinsured drivers. UM/UIM coverage is not required under Texas law, but insurers must offer it when you buy a policy. If you turned it down, you may not have it.

One thing to understand about first-party claims: your insurance contract can require you to cooperate. That may include providing a recorded statement to your own insurer. This is different from what a third-party adjuster can ask of you. Texas Insurance Code Chapter 542 requires your own insurer to acknowledge your claim within 15 days and to pay or deny it within defined deadlines after receiving the required information.

Third-Party Claims

A third-party claim is filed directly against the at-fault driver’s liability insurance. If the other driver clearly caused the crash, this is usually the primary path to compensation for your injuries and bike damage.

Texas requires drivers to carry a minimum of $30,000 per person for bodily injury under Texas Transportation Code § 601.072. That limit isn’t always high enough in a serious motorcycle crash. If the at-fault driver’s policy isn’t enough to cover your medical bills, lost wages, and bike damage, your own UM/UIM coverage can bridge the gap.

When filing a third-party claim, get the police report, the at-fault driver’s insurance information, and photos of the scene and your injuries. The adjuster handling that claim works for the at-fault driver’s insurer. They are not on your side.

The Recorded Statement Request

One of the first things a third-party adjuster will ask for is a recorded statement. They will frame it as routine, as just confirming the details. Do not agree without understanding what you’re agreeing to.

A recorded statement is a phone call the adjuster records and transcribes. It becomes part of your claim file. You have no legal obligation to give one to a third-party insurer. No Texas statute requires it.

Adjusters use recorded statements to find inconsistencies. If your account differs in any way from the police report, a witness statement, or your medical records, they will use that gap to dispute your version of events. Statements made early, before you know the full extent of your injuries, can lock in descriptions of pain and symptoms that don’t match a later diagnosis.

If you have already been approached, you can decline and tell the adjuster your attorney will be in contact. If you haven’t spoken to one yet, do that before agreeing to anything. When you contact an attorney, they are on your side. Your attorney can help you understand when it makes sense to accept an insurance settlement offer, and when it doesn’t.

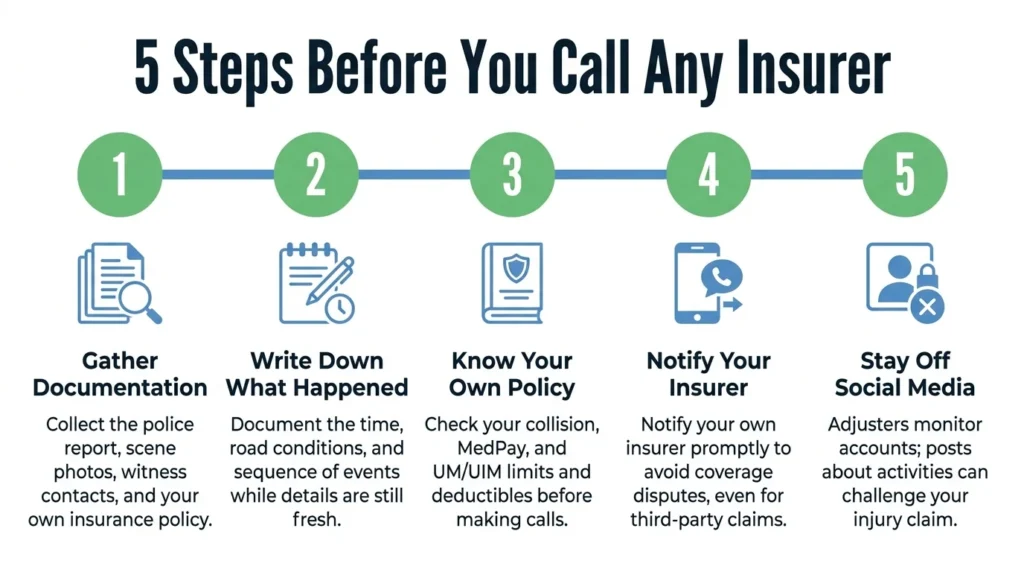

Steps to Take Before You Call Any Insurer

Before speaking with any insurance representative, take time to prepare. The goal is to avoid giving information that is incomplete, premature, or that can be used against you later.

Step 1: Gather Your Documentation.

Collect the police report, photos of the scene and bike damage, contact information for any witnesses, and a copy of your own insurance policy. Know your coverage limits before calling anyone.

Step 2: Write Down What Happened

Do this while the details are fresh. Include the time, road conditions, what the other driver did, estimated speeds, and the sequence of events. This becomes your reference point for any future conversations.

Step 3: Know Your Own Policy

Check your collision, MedPay, and UM/UIM limits before calling your own insurer. Know your deductibles. Understand what your policy requires of you so you aren’t surprised.

Step 4: Notify Your Insurer Promptly.

Even if you plan to file a third-party claim first, notify your own insurance company of the crash. Late notice can create policy complications, including coverage disputes.

Step 5: Stay Off Social Media

Adjusters monitor social media accounts during active claims. Posts about your activities, your recovery, or the accident itself can be used to challenge your injuries or fault position.

When To Call a Motorcycle Accident Attorney

If you have serious injuries, a disputed fault finding, or a recorded statement request you haven’t answered, talking to an attorney before responding to the insurer is the right call.

Angel Reyes & Associates has helped injured Texans through the process of dealing with insurers after motorcycle accidents for over 30 years. We understand how insurer bias works in motorcycle claims, and we know how to document the crash and build the record that changes those negotiations. You pay nothing unless we recover compensation for you. Consultations are free, and we’re available 24/7 to help you.

For more context on how our team approaches personal injury cases, you can learn about us and our case results.

The two-year filing deadline under CPRC § 16.003 starts on the date of your crash. In serious injury cases, that window can close before you realize you need to act. Reach out for a free consultation and understand your options before the process moves further along.

Past results do not guarantee future outcomes.

Motorcycle Accident Insurance FAQs

Can not wearing a helmet hurt my motorcycle insurance claim in Texas?

Texas allows riders 21 and older to ride without a helmet if they have completed a safety course or carry qualifying health insurance that covers motorcycle accident injuries, but this legal exemption doesn’t stop an insurer from raising helmet use as a comparative fault argument. If an insurer successfully ties your lack of a helmet to the severity of your head or neck injuries, it could reduce your recovery by your assigned fault percentage.

What happens if the at-fault driver has no insurance and I don't have UM coverage?

Without UM/UIM coverage on your own policy, your options narrow significantly: you can file suit directly against the at-fault driver personally, but collecting on a judgment against someone with no insurance is often difficult. If an insurer claims you rejected UM coverage, Texas law requires it to produce your signed written rejection. If the insurer can’t produce it, you may still be deemed covered.

Does Texas law require the other driver's insurer to resolve my claim within a set timeframe?

No. Texas’s prompt payment rules under Insurance Code Chapter 542 apply to first-party claims with your own insurer, not to third-party claims against the at-fault driver’s carrier. Third-party claims can drag on for months or longer, especially when liability is disputed or injuries require ongoing treatment.

I already gave the insurance company a recorded statement. What now?

A recorded statement doesn’t automatically kill your claim, but it can complicate negotiations if your account differed from the police report or later medical records. An attorney can review what was said, help you document any inconsistencies with context, and manage all communications with the insurer going forward.

Can I still recover damages if I was partly at fault for the motorcycle crash?

Yes, as long as your share of fault does not exceed 50%. Texas proportionate responsibility law reduces your recovery by your fault percentage, so if you were 30% at fault and your damages total $100,000, you recover $70,000. At 51% or more fault, you recover nothing.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...