Prompt Payment Rules Texas Insurers Must Follow

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas Insurance Code Chapter 542 can impose an 18% annual penalty when insurers miss claim-handling deadlines.

- Chapter 542A applies to certain property-damage lawsuits and requires pre-suit notice before filing.

- Documenting every insurer communication, deadline, and payment creates the foundation for any bad-faith or prompt-payment claim.

Your insurance company approved your claim three weeks ago. The adjuster said the check was “in process.” You’ve called twice, left messages, and still have no payment. Meanwhile, your car sits at the shop in Fort Worth, and the rental bill keeps climbing.

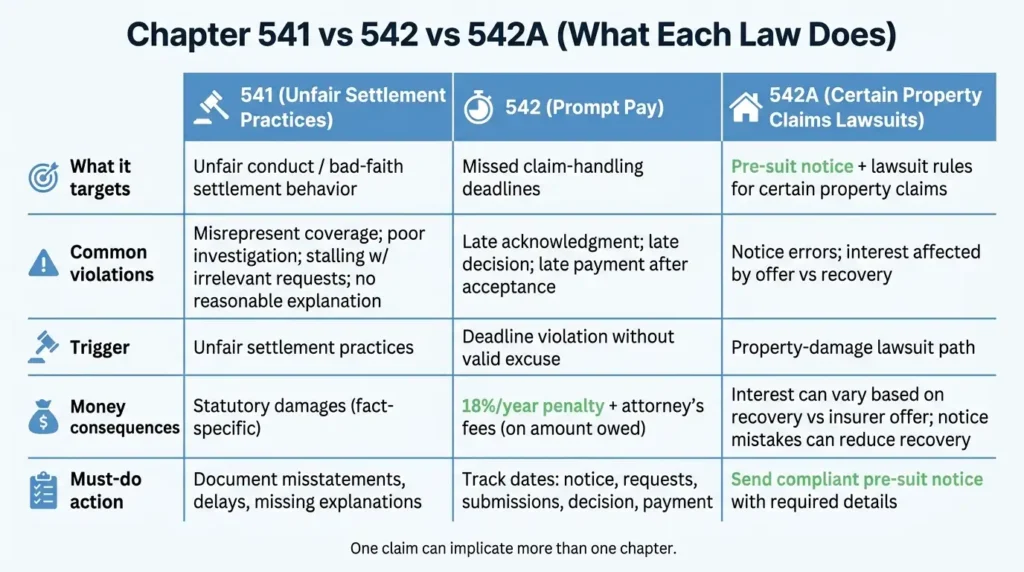

Texas law doesn’t leave you empty-handed when your insurer drags its feet or lowballs a legitimate claim. Two main statutory frameworks can turn delay and unfair conduct into real, recoverable damages: the prompt-payment rules under Texas Insurance Code Chapter 542 and the unfair settlement practices provisions under Chapter 541. For certain property-damage claims, Chapter 542A adds another layer with its own notice requirements and interest calculations.

Knowing how these statutes work together helps you spot when an insurer’s behavior has crossed a legal line, and what you need to document to protect yourself.

What “Bad Faith” and “Prompt Pay” Mean in Texas Law

An insurer cannot refuse to pay out a claim that they are responsible for. It’s one thing to do their due diligence and investigate a claim, but Texas law sets standards for how this should proceed. Failing to abide by this law could be a sign of “insurance bad faith,” which is illegal.

Insurance bad faith is a phrase that gets thrown around a lot, but in Texas, it ties to specific statutory violations. Texas Insurance Code § 541.060 sets out the unfair settlement practices insurers are prohibited from using. These include:

- Misrepresenting what a policy covers

- Failing to push toward a fair settlement when liability is reasonably clear

- Refusing to give a reasonable explanation for denying or delaying a claim

- Skipping a proper investigation altogether

- Stalling by demanding paperwork that has no real bearing on the claim

Chapter 542, the Texas Prompt Payment of Claims Act, takes a more mechanical approach. It lays out specific deadlines insurers must hit when processing a claim. Miss those deadlines without a valid reason, and the statute can tack on an 18% per-year penalty on the amount owed, plus reasonable attorney’s fees.

One claim can trigger both statutes at the same time. An insurer that strings a claimant along for months while offering nothing but vague updates may be violating the prompt-payment timeline under Chapter 542 and engaging in unfair settlement practices under Chapter 541. Attorneys reviewing delayed or denied claims typically look at both angles.

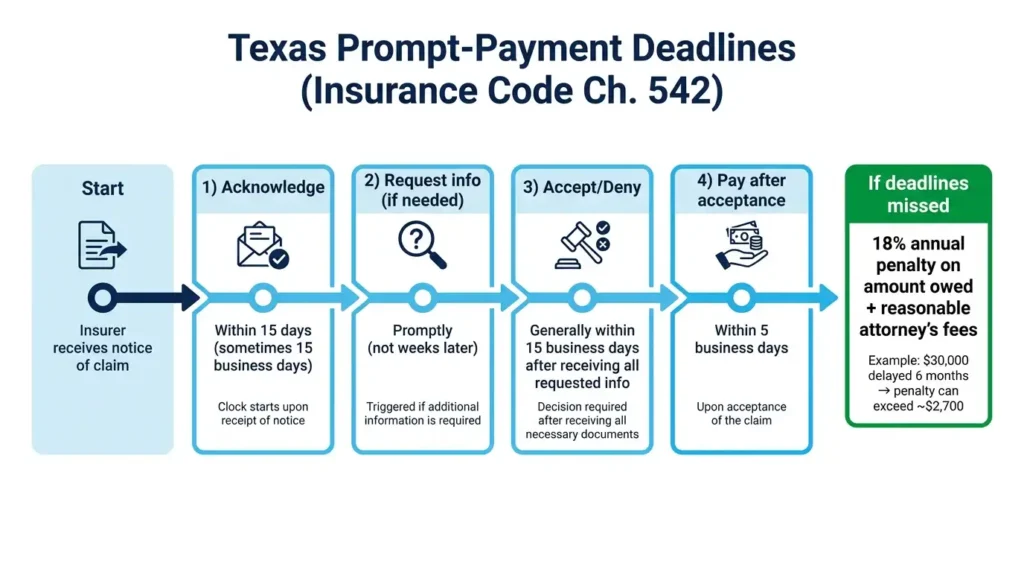

The Prompt-Payment Timeline in Chapter 542

Texas law gives insurers a specific sequence they must follow after receiving notice of a claim. The Texas Department of Insurance outlines these requirements for consumers:

- Acknowledgment: The insurer must confirm receipt of the claim within 15 days (or 15 business days for certain claims).

- Request for Information: If additional documentation is needed, the insurer must ask for it promptly, not weeks later.

- Decision: After receiving all requested information, the insurer generally has 15 business days to accept or deny the claim.

- Payment: Once the insurer accepts liability, the check must go out within 5 business days.

That start date matters more than most people realize. So do the dates you submitted any requested documents. Keep copies of everything you send.

When an insurer misses these deadlines without a legitimate excuse, Chapter 542 can layer the 18% annual penalty on top of whatever they should have paid. On a $30,000 claim delayed six months, that penalty alone can push past $2,700.

Chapter 542A: Rules for Property Claims

If your dispute involves property damage and you’re thinking about filing a lawsuit, Chapter 542A may come into play. This statute creates its own separate framework with requirements you can’t skip.

The most important difference is the pre-suit notice requirement. Before filing certain property-damage lawsuits, you generally have to send the insurer a written notice that includes specific details about your claim and the damages you’re seeking. That notice gives the insurer a window to inspect the property and potentially work out the dispute before you ever walk into a courthouse.

Chapter 542A also has its own way of calculating interest. Rather than the flat 18% penalty under Chapter 542, the interest calculation under 542A can shift depending on how much you ultimately recover compared to what the insurer originally offered.

Getting the pre-suit notice wrong, or skipping it entirely, can cost you money on the back end. That’s one reason talking to an attorney before sending demand letters on a property claim is worth the conversation.

A proper 542A notice package typically covers:

- Policyholder information and claim number

- Property address and date of loss

- A timeline of inspections and adjuster contacts

- Photos, repair estimates, and contractor reports

- A breakdown of what you’re claiming versus what the insurer paid

- Documentation of any additional living expenses

What Delay & Underpayment Looks Like

Insurance companies exist to make money, which means settling claims for as little as possible. That’s not illegal on its own. But some tactics go too far.

Frequently Rotating Adjusters

Your car accident claim gets handed off to a new adjuster every few weeks. Each one needs time to “review the file.” Months go by. No decision. This pattern can trigger both prompt-payment violations and unfair settlement practice claims.

Never-Ending Document Requests

You’ve already sent medical records, repair estimates, and photos. Now the insurer wants the same documents again, or starts asking for things that don’t exist. Requesting unnecessary paperwork to buy more time violates § 541.060.

Lowball Payments

After a truck accident on I-35W near downtown Fort Worth, the insurer’s estimate leaves out half the damage your mechanic documented. They sent a check, but it’s thousands short of the actual repair costs. A partial payment with no real explanation can still create prompt-pay and unfair-practice exposure for the insurer.

The Silent Treatment

Your claim just sits there. Calls go to voicemail. Emails get form responses. The Texas Department of Insurance has specifically flagged failure to respond to communications as problematic conduct.

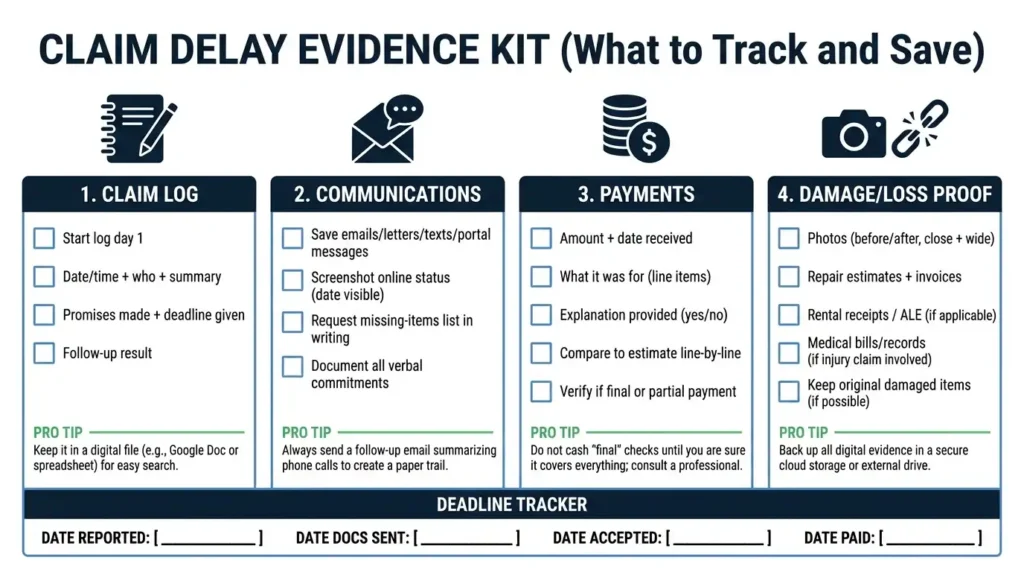

Building Your Evidence: What to Track and Save

Delay and underpayment cases are won or lost on documentation. Start a claim log the day you report your loss.

Record every contact. Date, time, who you spoke with, what they said, and what they promised. Note any callback commitments, and whether they were actually kept.

Save all written communications. Emails, letters, texts, portal messages. Screenshot your online claim status with the date visible.

Track every payment. What was paid, when it hit your account, and what explanation (if any) came with it. Compare each payment to your estimates line by line.

Preserve your evidence. Photos of damage, repair invoices, rental receipts, and medical bills. If the insurer’s estimate excludes items that are clearly documented, note exactly what they skipped or undervalued.

This paper trail does more than one thing. It helps you pinpoint why your insurer is stalling. It lets you confirm whether statutory deadlines were actually met. And it forms the backbone of any future legal claim.

When It’s Time to Call an Attorney

Not every slow claim needs a lawyer. But some situations make it worth picking up the phone sooner rather than later.

Repeated delays with no clear explanation. If the insurer keeps saying they’re “still investigating” without telling you what they’re waiting on, that’s a red flag.

Payment that ignores your documentation. When an insurer’s estimate ignores damage that’s clearly documented, you may need legal pressure to get them to reconsider.

Pressure to sign releases fast. Insurers sometimes push for quick settlements before you know the full extent of your losses. Have an attorney look at any release before you sign it.

Property claims needing a 542A notice. Because a defective notice can reduce what you recover, getting it right the first time matters. An attorney helps you avoid procedural mistakes that cost money later.

Claims tied to serious accidents. If your insurance dispute comes out of a motorcycle accident or another collision with significant injuries, the stakes are too high to navigate alone. An attorney can coordinate the insurance side with any injury claims.

How Angel Reyes & Associates Can Help

Dealing with an insurer that won’t pay what it owes is exhausting. You shouldn’t have to become an expert in insurance code provisions just to get treated fairly.

Angel Reyes & Associates has spent over 30 years helping Texans hold insurance companies accountable. We know how Chapters 541, 542, and 542A work together, what documentation builds a strong case, and which deadlines matter most.

We offer free consultations and work on contingency—you pay nothing unless we recover money for you. We serve clients across Texas from our more than 20 offices statewide, and handle most cases remotely.

If your claim has stalled, been underpaid, or denied without a real reason, reach out to us to talk through your options. The sooner you act, the stronger your position.

Insurance Bad Faith FAQs

Does filing a complaint with the Texas Department of Insurance make the insurer pay my claim?

A TDI complaint can sometimes prompt a response or create a paper record of the delay, but it doesn’t guarantee payment or decide a lawsuit. It’s best used as one tool alongside solid claim documentation.

Can a partial payment still lead to a prompt-payment dispute in Texas?

Yes. If an insurer pays part of a claim but unreasonably delays or shortchanges the rest, the unpaid balance may still raise prompt-payment or unfair-settlement issues depending on the facts.

What if the insurance company says it's still waiting on documents from me?

Ask the insurer to put in writing exactly what’s missing and when it was first requested. That helps you confirm whether the delay is legitimate or whether they’re moving the goalposts.

Do Texas prompt-payment rules apply to every type of insurance claim?

Not always in the same way. The type of policy and claim can affect which statutes apply and how deadlines are measured. Property-damage lawsuits may also involve Chapter 542A rules that change the analysis.

Should I sign a release if the insurer sends a check, but I think the claim was underpaid?

Proceed carefully. Cashing a check or signing certain documents can limit your ability to pursue more money later. Read the language closely before agreeing to anything, or have an attorney review it first.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...