Commercial Insurance for Contractor Pickup Trucks

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

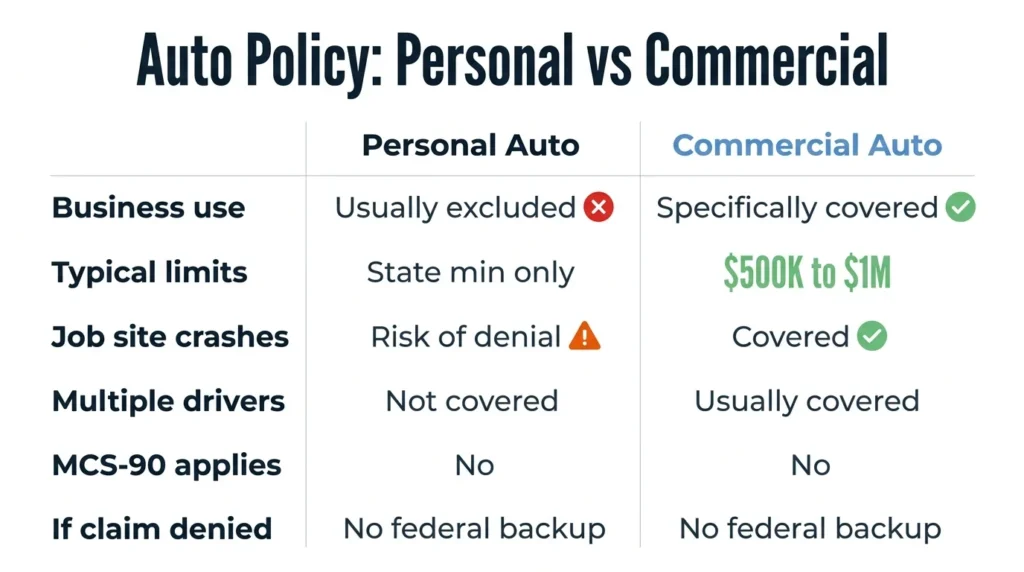

- Contractor pickup trucks are not regulated by FMCSA, so there is no federal backup that forces coverage when a personal auto insurer denies a claim because the truck was being used for business.

- A business use exclusion in a personal auto policy may deny coverage for crashes that occur while the contractor was driving to or from a job site, even if the driver is technically insured.

- The contractor's employer or hiring business may be liable through respondeat superior, or they may be directly liable if they employed negligent hiring practices or if the contractor performed inherently dangerous work.

Maybe a plumber’s truck ran a red light and hit your car. Or maybe a landscaper’s pickup merged into you on the freeway. Or perhaps an electrician’s van sideswiped you in a parking lot.

In these scenarios, the crash itself looks like any other vehicle accident, but the insurance is more complicated because the vehicle was being used for business at the time of the crash, and the driver may not carry commercial coverage.

Who pays depends on the policy that the contractor carries, what it covers, and whether the business that sent the driver to the job site shares responsibility.

Why Contractor Pickup Trucks Are Not the Same as Commercial Trucks

Contractor pickup trucks are not subject to federal regulations that apply to large commercial motor vehicles. The Federal Motor Carrier Safety Administration regulates vehicles that are over 10,001 lbs and are used for interstate commerce or for-hire freight transport. Most contractor pickup trucks weigh less than this, so there is no FMCSA oversight, commercial driver’s license requirement, or MCS-90 endorsement.

The MCS-90 is the federal safety requirement attached to large carrier policies that forces an insurer to pay a final judgment against the motor carrier, regardless of policy exclusions. Contractor pickup trucks are not subject to this. If a personal auto insurer denies coverage for a contractor truck crash, there is no federal rule that can force the insurer to pay.

A contractor truck crash is handled entirely by Texas state law and the specific policy that the driver purchased, whether that is personal or commercial auto coverage. Understanding how truck crashes are legally different from car accidents puts these differences into perspective.

The Personal Auto Policy Gap and Business Use Exclusions

The most common coverage problem in contractor truck crashes is straightforward: the contractor was driving a personal pickup truck and purchased a personal auto policy that excludes business use.

Nearly every personal auto policy includes a business use exclusion that denies coverage for accidents that occurred while the vehicle was being used for commercial or business purposes. Driving to a job site with tools in the truck, transporting materials, and hauling equipment all typically qualify as “business use” by the policy’s own definition. If an insurer discovers the driver was on the way to a job or returning from one, it may cite this exclusion to deny the claim.

The contractor may meet Texas’s minimum financial responsibility requirements under Texas Transportation Code § 601.072, which are $30,000 per person, $60,000 per accident for bodily injuries, and $25,000 for property damage. However, meeting these minimums does not prevent the insurer from denying a claim if the accident happened during business use.

However, a coverage denial under the business use exclusion is the starting point of the claim, not the end. Other defendants and policies may still apply.

What Commercial Auto Insurance Covers for Contractor Trucks

When a contractor carries a commercial auto policy, the coverage looks very different. Commercial auto policies are designed for vehicles that are used in business operations, and they typically provide substantially higher liability limits (commonly $500,000 to $1,000,000 per accident), as compared to the state minimum personal auto limits.

Commercial policies also extend to business-use driving in ways that personal policies do not. They cover multiple drivers (including employees), protect physical damage to the vehicle during business operations, and include coverage for accidents that occur during business activities.

Some commercial policies include hired and non-owned auto coverage, which extends the policy to vehicles the business hired, borrowed, or gave to employees to use for business purposes. This even extends to vehicles that the employees own personally.

For example, if the contractor was driving their own truck on the employer’s behalf, and the employer’s commercial policy included hired and non-owned auto coverage, then the employer’s policy may cover the crash.

Understanding what commercial truck insurance actually covers can help you and your attorney identify which coverage sources are worth pursuing.

When the Contractor’s Employer or Hiring Business Is Liable

Even if the contractor’s own policy denies a claim, the business that dispatched them may carry commercial insurance that applies, and they may face direct liability for the crash.

Texas law holds employers responsible for employee negligence committed while working. This is a rule called “respondeat superior.” If the contractor was an employee of the business, and they were driving for company business at the time of the crash, the employer’s commercial liability policy covers the claim either alongside or instead of the contractor’s own coverage.

The central issue is the distinction between employee and independent contractor. Texas courts look at how much control the business had over how, when, and where the contractor worked. The more control the company has, the more likely the contractor will be treated as an employee for liability purposes.

There are two situations in which a company can still be held liable, even if the contractor is a true independent contractor:

- If the business assigned work that was inherently dangerous, the company may still be held liable. The company cannot avoid responsibility by hiring someone else to do the work.

- If the company used negligent hiring practices (such as selecting a contractor with a known poor safety record, giving unsafe instructions, or failing to provide a safe work site), it can be held directly liable.

Texas truck accident claims that go beyond the individual driver’s policy require you to identify who controlled the work and who sent the driver to the site.

How to Protect Your Claim After a Contractor Truck Crash

Several steps must be taken immediately after the crash to make a significant difference in which coverage sources remain available.

Identify who employed the contractor, and why they were driving at the time of the crash. At the scene, ask the driver for their employer’s name, the job site address, and who dispatched them. Company logos on the truck, tools or materials visible in the vehicle, and job site paperwork are all evidence of the driver’s work purpose.

Establish whether the driver carries personal or commercial auto insurance. When the driver provides their insurance information at the scene, note the insurer and policy type. If the driver only lists a personal auto policy, inform your attorney immediately, so they can investigate whether the business use exclusion applies before the insurer processes the claim.

If the contractor was dispatched on company business, file a claim with the employer’s commercial insurance and the driver’s own insurer. Do not wait to see whether one insurer denies your claim before pursuing another.

If the contractor’s personal policy and the employer’s insurance both deny coverage or do not provide enough coverage, your own uninsured or underinsured motorist coverage may cover the remaining losses.

Working with an Attorney on Contractor Truck Crashes

Contractor truck crashes involve complicated insurance issues, including personal policy exclusions, disputed employment status of the driver, and multiple liable parties. Most insurance adjusters do not resolve these issues in the victim’s favor.

Angel Reyes & Associates can help. Our firm has handled Texas vehicle accident claims for over 30 years, and we work on contingency, which means you pay no fee unless we win. Contact us for a free consultation.

Contractor Truck Crash FAQs

What if the contractor says they were just driving to the job site? Is that considered business use?

In most cases, yes. Driving to and from a job site in a vehicle used for business purposes constitutes business use under personal auto policy definitions. A contractor transporting tools, materials, or even just themselves to a work location generally equates to operating the vehicle for business purposes. This triggers the business use exclusion in a personal auto policy.

Can I get the general contractor's insurance to pay if a subcontractor hit me?

It depends on the facts of the crash. If the subcontractor was performing inherently dangerous work that was delegated to them by the general contractor, then the general contractor may be held liable under the non-delegable duty doctrine. Likewise, if the general contractor had substantial control over the subcontractor’s work, then the court may treat the subcontractor as an employee for liability purposes.

What if the contractor drove their own truck, but the company paid for gas and maintenance?

These facts are important when deciding whether the driver was an employee or an independent contractor. A business that reimburses vehicle expenses, requires a specific truck, or controls when and where the vehicle is used may treat the driver as an employee, rather than an independent contractor. The more control the business had over how the truck was used, the stronger the argument that the company’s insurance should cover the crash.

What is the minimum insurance that a contractor driving in Texas must carry?

Under Texas Transportation Code § 601.072, every vehicle operating on Texas public roads must meet the minimum financial responsibility of $30,000 per person, $60,000 per accident for bodily injury, and $25,000 per accident for property damage. These minimums apply to contractor pickup trucks the same way they apply to any personal vehicle. They are the minimum required by law, but they do not guarantee that coverage will apply to a crash that happened during business use under the contractor’s personal policy, and they are usually not enough to cover serious injuries.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...