How UM/UIM Handles Crashes Involving Company-Owned Trucks

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- UM/UIM on your personal auto policy can pay the gap when a company truck is underinsured.

- Notify your own insurer in writing before settling with the employer to protect UIM rights.

- Commercial fleet policies in Texas rarely include UM/UIM coverage for third parties they hit.

You were heading east on I-30 near downtown Fort Worth when a delivery truck drifted into your lane and clipped your front bumper. The driver handed you a card with a company name you didn’t recognize. Now the employer’s insurer is dragging its feet, and the medical bills are stacking up faster than the offers are coming in.

Who Pays When a Company Truck Hits You

When a company-owned truck causes a crash, the employer’s commercial auto policy is usually the first source of payment. Under a Texas legal doctrine called respondeat superior, employers are responsible for crashes their employees cause while working. Because of commercial truck insurance requirements, that policy often carries higher limits than personal auto insurance, but it can still fall short or get disputed.

The first fight is often whether the driver was actually on the job. Insurers and employers regularly argue that the driver was off duty, running a personal errand, or otherwise outside the scope of employment. If that argument sticks, the employer’s policy may not cover you at all.

Even when liability is clear, the commercial policy may have a self-insured retention layer that delays payment. Layered policies and disputed coverage create gaps in what you can actually collect.

Federal & Texas Coverage Requirements for Company Trucks

Commercial trucks must meet specific insurance floors, but those floors vary widely.

- Federal rules apply to interstate trucks above certain weight thresholds.

- Texas rules apply to intrastate trucks operating only within the state.

Knowing which set applies tells you what coverage the at-fault truck was required to carry.

Interstate carriers must meet FMCSA financial responsibility requirements, which range from $750,000 to $5 million depending on cargo and route. Intrastate trucks follow Texas financial responsibility rules instead, and those floors are often lower.

Under Texas Transportation Code § 601.051, every motor vehicle that operates in Texas must carry financial responsibility. For intrastate commercial carriers specifically, Texas Transportation Code Chapter 643 and 43 Texas Administrative Code Chapter 218 set out the more direct regulatory framework. Large trucking companies sometimes use layered policies or self-insured retention arrangements that reduce what is practically available to a claimant.

When a commercial truck carries only minimum coverage and your damages exceed those limits, you are dealing with an underinsured driver.

When UM/UIM Coverage Applies in a Company Truck Crash

Uninsured motorist and underinsured motorist (UM/UIM) coverage on your own personal auto policy can step in when the at-fault company truck’s coverage is missing or not enough. Texas Insurance Code Chapter 1952 requires this protection in every automobile liability policy by default — you have it unless you rejected it in writing when you bought the policy.

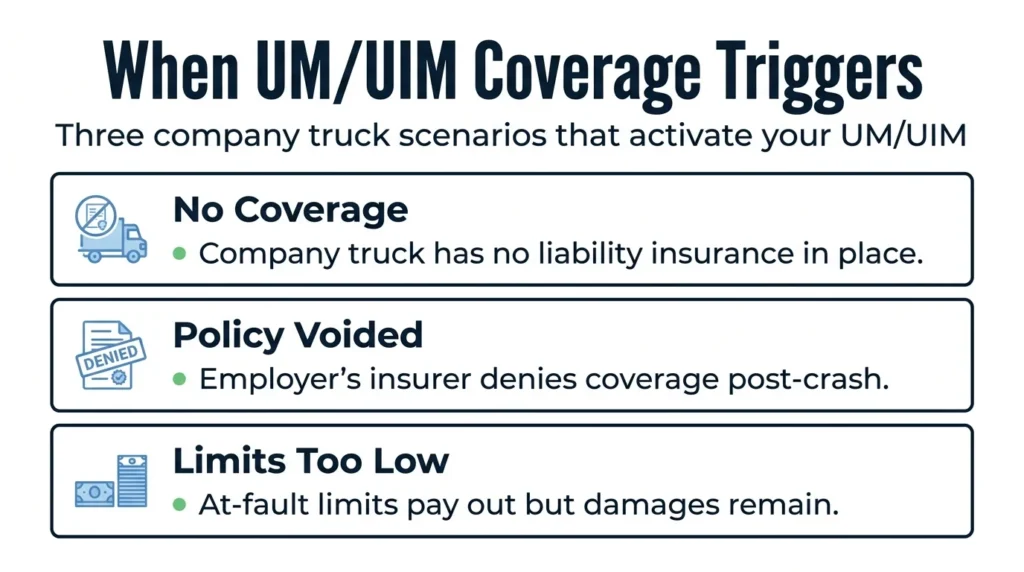

Uninsured Motor Vehicle Trigger

A company truck counts as uninsured when it carries no liability coverage, the policy is voided or denied by the employer’s insurer, or the employer’s insurer becomes insolvent.

A hit-and-run by an identifiable company truck may also trigger UM coverage. Policy language requiring physical contact can complicate these claims, so the specific wording is important.

Underinsured Motor Vehicle Trigger

A commercial truck is underinsured when the employer’s policy limits are smaller than your total damages. This is common in serious crashes, where medical bills and lost wages quickly outrun standard fleet limits.

Your UIM claim pays the gap. If the employer’s policy paid $200,000 and your damages are $400,000, your UIM coverage may pay up to its limit toward the remaining $200,000, offset by what you already received.

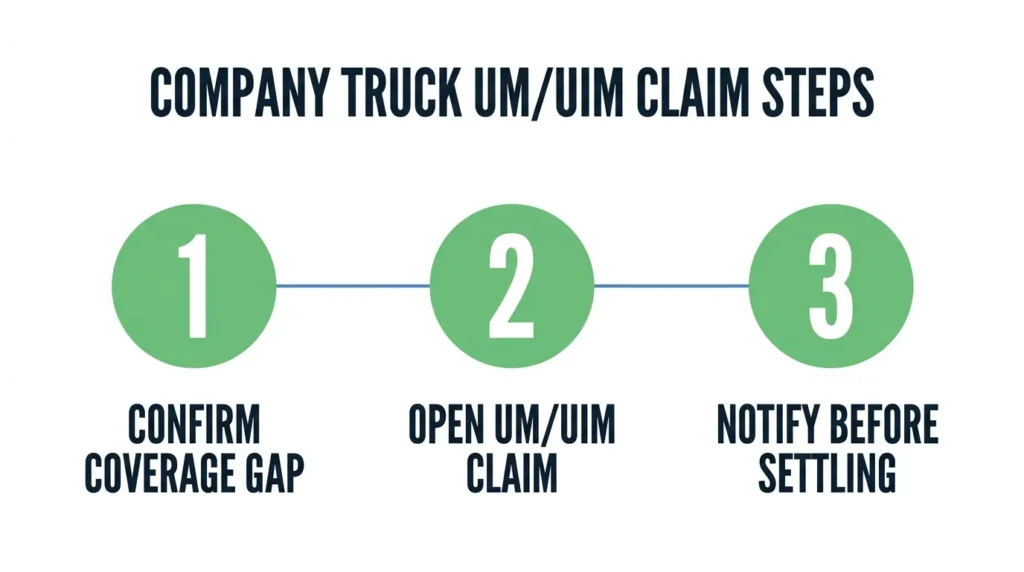

Before you settle with the employer’s insurer, notify your own carrier in writing. Settling without that notice can wipe out your UIM claim entirely. Many delivery truck crashes fall into this scenario, which is why understanding the steps to take in a Texas uninsured motorist claim early can protect your recovery.

Does a Commercial Fleet Policy Include UM/UIM?

Usually no, at least not for you. Texas law does not require commercial auto policies to include uninsured motorist coverage. When fleet policies do carry it, the benefits typically protect the company’s own employees rather than the people the truck hits. As a third party, you generally cannot reach into the employer’s fleet policy for UM/UIM money.

That leaves your own personal policy as the secondary recovery layer, so it’s important to understand how UM/UIM and PIP coverage in Texas fit together.

When the employer’s commercial policy does include UM/UIM coverage and they somehow apply, the coverage may interact with your own policy through Texas offset rules. The practical effect is rarely a windfall.

If the commercial fleet policy on the at-fault truck cannot fully cover your losses, your own UM/UIM coverage is usually the next stop.

Talk to a Texas Truck Accident Attorney

Company truck crash claims involve overlapping coverage layers, scope-of-employment disputes, and notice requirements that can quietly cost you money if missed. An attorney can identify which policies apply, evaluate employer liability, and send the UIM preservation notice before you sign anything.

Angel Reyes & Associates has over 30 years of experience handling Texas motor vehicle and truck accident claims, with more than $1 billion recovered for our clients. We offer free consultations, work on contingency with no fee unless we win, and can handle most of your case remotely.

Our case results show how we approach commercial vehicle claims. Contact us today to talk through your situation with a free consultation.

Past results do not guarantee future outcomes.

Company Truck Accident FAQs

Can I use my UM/UIM coverage if the company truck driver was an independent contractor rather than an employee?

It depends on how the driver was classified and whether the hiring company controlled their work. If the employer’s insurer denies liability by arguing the driver was an independent contractor, the at-fault truck may qualify as uninsured under your own policy, which could trigger your UM coverage.

Does Texas law set a deadline for filing a UM/UIM claim after a commercial truck crash?

In Texas, the statute of limitations for a personal injury claim is generally two years from the date of the crash. Your UM/UIM contract may also include its own notice and filing deadlines, which can be shorter, so reading your policy terms early matters.

Will my personal UM/UIM rates go up if I file a claim after a company truck hits me?

Texas law prohibits insurers from surcharging or canceling your policy solely because you filed a UM/UIM claim when you were not at fault. However, each insurer’s practices can differ, so reviewing your policy language or asking your insurer directly is a good idea.

Can I stack UM/UIM coverage from multiple personal policies after a commercial truck crash?

Texas allows stacking only if your policies or the insurer’s practices permit it. Most standard personal auto policies include anti-stacking language that limits recovery to the single highest applicable limit, so the answer turns on your specific policy terms.

What if the company truck was a rental vehicle rather than owned by the employer?

A rental truck can complicate the coverage picture because both the rental company’s liability coverage and the employer’s non-owned auto coverage may apply before your personal UM/UIM is reached. The order in which those policies respond depends on the rental agreement and the employer’s commercial policy language.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Alex Ivanov

Reviewer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in...