What to Do When the Other Driver Hands You a Fake Insurance Card in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- A fake insurance card does not create coverage -- the driver is legally treated as uninsured for purposes of your claim.

- Presenting a fraudulent insurance document is a crime in Texas under Penal Code § 37.10 and related fraud statutes.

- UM coverage (not UIM) applies in a fake-insurance scenario because the at-fault driver has zero valid coverage.

You’re in a crash happens on Congress Avenue or the I-35 corridor in Austin, and the other driver hands you an insurance card to photograph. You call the insurer listed days later and you are told that the policy number does not exist. The discovery is disorienting. What you thought was a routine claim has now become something else entirely.

This guide explains what a fake insurance card means for your legal options and what steps to take next.

What a Fake Insurance Card Means for Your Claim

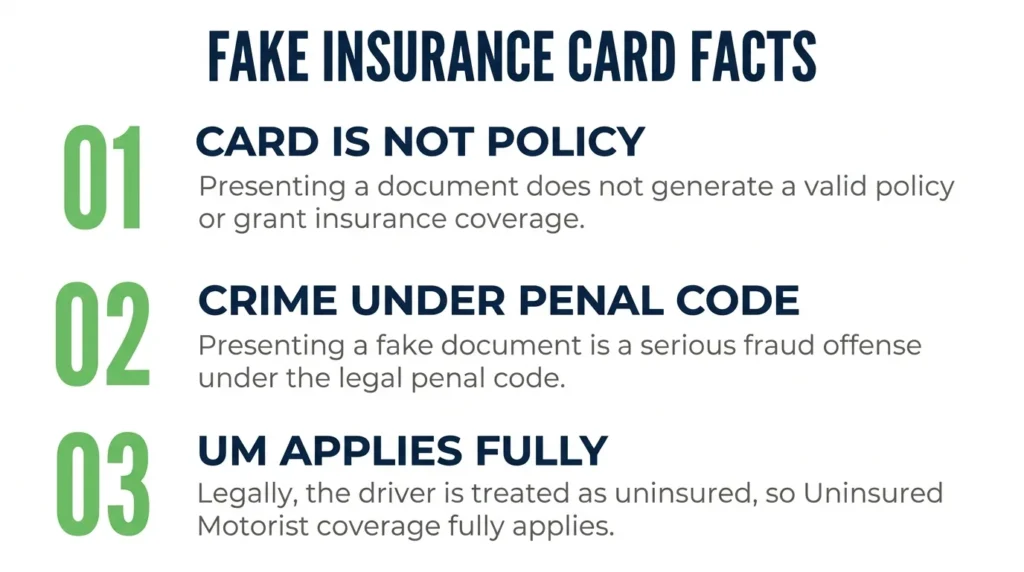

An insurance card is not a policy. It is a document that represents the existence of a policy. If the policy listed on the card does not exist, was never issued to that driver or vehicle, or has been cancelled, there is no coverage regardless of what the card says.

Presenting a fraudulent insurance document is a crime in Texas. Texas Penal Code § 37.01(2)(D) prohibits tampering with governmental records, and a fake insurance document falls within related fraud statutes. The driver who handed you that card may face criminal liability separate from any civil claim you bring.

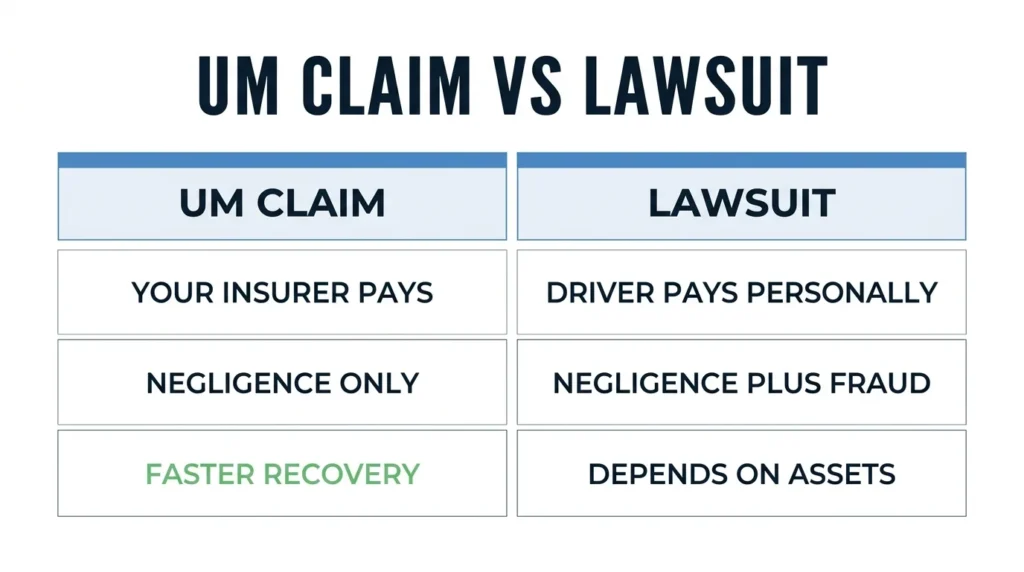

From a coverage standpoint, the legal result is straightforward: a driver whose insurance card is fake occupies the same position as a driver with no insurance at all. Your claim against the other driver’s insurer ends the moment you confirm the policy does not exist. Your recovery path shifts entirely.

For a broader overview of what happens when the at-fault driver has no valid coverage, see the Texas Uninsured Motorist Accident Guide.

Steps to Take When You Discover the Insurance Was Fake

The discovery usually comes when you or your attorney calls the insurer listed on the card and the representative has no record of the policy.

Document what you have. The photograph of the card, the police report, the driver’s name, license number, and plate. These form the evidentiary record of what occurred. Preserve all of it immediately.

Contact your own insurer. Report that the other driver appears to be uninsured. Do not wait for formal confirmation from the listed insurer. Your own policy’s uninsured motorist coverage is now your primary tool, and notifying your insurer promptly protects your claim.

File a police report if you have not already. Some victims discover the fake insurance days or weeks after the crash. You can still report the fraudulent document to the police department that handled the original accident report, and you can file a new report if you initially thought the other driver was insured.

Report the fraud to the Texas Department of Insurance. The TDI investigates insurance fraud and can refer cases for criminal prosecution. A TDI report does not directly compensate you, that comes through your civil options, but it creates a formal record and may result in action against the driver.

For specific guidance, see our blog on initial steps after learning the at-fault driver has no coverage.

How Your UM/UIM Coverage Applies

Texas Insurance Code Chapter 1952 requires every auto insurer to offer uninsured/underinsured motorist coverage with every policy. The coverage can only be declined in writing. If you did not sign a written rejection of UM/UIM coverage, you almost certainly have it.

In a fake insurance scenario, the at-fault driver has zero valid coverage. That means your uninsured motorist (UM) coverage applies, not your underinsured motorist (UIM) coverage. UIM applies when the other driver has some coverage but not enough. Here, there is none.

UM coverage pays for your bodily injury damages: medical bills, lost wages, pain and suffering, and other compensable losses, up to your policy limit. Some policies also include UM property damage coverage.

One important feature of Texas UM law: no physical contact requirement. Some states require that the uninsured vehicle actually made contact with yours before UM coverage applies. Texas does not impose that requirement, which is reassuring in a scenario where the contact clearly occurred and is documented.

For a detailed breakdown, see our blog of how UM, UIM, and PIP coverage each work.

What About the At-Fault Driver Personally?

UM coverage is faster and more reliable than suing an individual, but a personal lawsuit against the driver remains available and can be pursued at the same time.

A personal lawsuit can include two separate claims. First, the negligence claim for the crash itself, the same claim you would bring against any at-fault driver. Second, a fraud claim arising from the fake insurance card. The driver who presented a document they knew was false may have committed fraud against you when you relied on that card in deciding how to handle the claim.

Recovery from a personal lawsuit depends entirely on what the defendant can pay. A judgment is a legal right to collect, not cash in hand. If the driver has no meaningful assets, the judgment may be difficult to enforce. That is why UM coverage, where you are dealing with your own insurer under a policy you paid for, is typically the more practical recovery path.

Texas Civil Practice and Remedies Code Chapter 33 governs the proportionate responsibility framework for the negligence claim. Separate fraud theories apply to the insurance fraud component.

Talk to a Texas Car Accident Lawyer

When the other driver’s insurance turns out to be fake, you are not out of options. Your own UM coverage, a personal lawsuit against the driver, and fraud reporting to TDI are all available tools — and they are not mutually exclusive.

Angel Reyes & Associates has handled uninsured motorist and car accident cases across Texas for over 30 years, with more than $1 billion recovered for clients. If you have discovered that the other driver’s insurance was fraudulent, the firm can evaluate your UM coverage, advise on the personal lawsuit option, and take the steps needed to protect your claim from the start.

We offer free consultations for car accident victims, and take no fee unless we win. Contact our firm to move your claim forward.

Frequently Asked Questions

How can I tell if an insurance card is fake at the scene of an accident?

You usually cannot tell just by looking. The most reliable approach is to call the insurer listed on the card while still at the scene and ask to verify that the policy number shown is active and covers the vehicle described. Most major insurers have 24-hour verification lines. Getting a police report also documents exactly what the driver presented, which protects you if the card later turns out to be fraudulent.

Does my UM coverage apply if I discover the insurance was fake days after the accident?

Yes. The timing of your discovery does not affect your eligibility. What matters for UM coverage purposes is that the at-fault driver was uninsured at the time of the crash. When you contact your own insurer, explain that you believed the other driver was insured based on the card they provided and that you have since learned the policy does not exist.

Can I file a UM claim if the at-fault driver left before the police arrived?

Yes, if you have identifying information. Texas UM coverage does not require physical contact with the uninsured vehicle. If you have the license plate number, the driver’s name, or other identifying details, your insurer can investigate. Without any identifying information, the claim becomes more difficult, but reporting the incident to police immediately after it happens preserves your options.

Will filing a UM claim raise my insurance rates?

Texas law generally prohibits insurers from surcharging a policyholder for filing a UM/UIM claim after a crash that was not the policyholder’s fault. However, policy terms and insurer practices vary. Review your policy and ask your insurer directly before filing if rate impact is a concern.

What should I do if the police report lists the fake insurance as the other driver's valid coverage?

Contact the police department that took the report and explain that the insurance listed has been verified as fraudulent or nonexistent. Request that the officer who wrote the report amend it to reflect the accurate status. A corrected report strengthens your UM claim and supports any fraud complaint you file with the Texas Department of Insurance.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...