Insurance Issues with Unauthorized Truck Drivers

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- "Unauthorized" covers multiple scenarios, including no CDL, wrong CDL class, disqualified status, named policy exclusion, or no carrier permission. Each has different coverage and liability implications.

- The MCS-90 endorsement requires a motor carrier's insurer to pay any final judgment against the carrier, even when the driver was excluded from coverage under the policy's own terms.

- The motor carrier faces direct liability through negligent entrustment and respondeat superior regardless of the driver's license status or the insurer's coverage position.

When a crash victim learns a truck driver was unlicensed, had the wrong credentials, or was explicitly excluded from the carrier’s insurance policy, they often assume coverage is off the table. That assumption is often wrong.

The driver’s authorization status creates insurance complexity, but it doesn’t eliminate the carrier’s own liability. In many cases, a federal rule overrides the policy exclusion entirely.

What “Unauthorized” Means for a Commercial Truck Driver

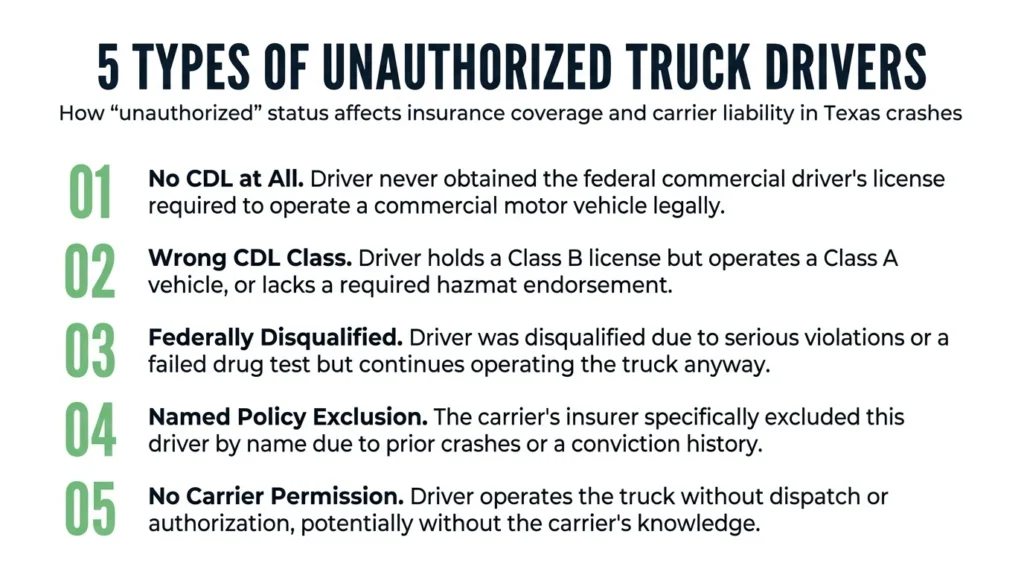

“Unauthorized” covers several distinct situations in the commercial trucking context, and each one has different legal consequences.

The clearest case is a driver with no commercial driver’s license, meaning someone who never obtained the federal CDL required to operate a commercial motor vehicle. A related but different scenario involves a CDL class mismatch: a driver holds a Class B license but operates a Class A vehicle, or drives a truck carrying hazardous materials without the required hazmat endorsement.

Both are violations of federal qualification requirements, but they arise in different factual contexts.

A third scenario involves a federally disqualified driver. This is someone who was disqualified from operating commercial motor vehicles due to serious traffic violations, an out-of-service order, or a failed drug or alcohol test, but who continues to operate anyway.

A disqualified driver is distinct from an unlicensed driver; the disqualified driver may still hold a CDL that has not yet been physically revoked.

The fourth and most insurance-specific scenario is a named excluded driver. The carrier’s insurer specifically identified this driver by name as excluded from coverage under the policy, usually because of a prior crash or conviction that made the driver uninsurable. Some crashes involve a driver who had no authorization from the carrier, but was operating the truck without dispatch, permission, and potentially the carrier’s knowledge.

Understanding the legal issues that arise when someone uses a vehicle they shouldn’t be using provides context for why these scenarios create coverage disputes.

What Federal Law Requires Before a Driver Can Operate a Commercial Truck

Before any driver gets behind the wheel of a commercial motor vehicle, the motor carrier has federal obligations it must meet. Those obligations are codified in 49 CFR Part 391, which governs driver qualifications.

Every motor carrier must maintain a Driver Qualification File for each driver. The file must include:

- Verification of the driver’s commercial driver’s license

- A motor vehicle record obtained from each licensing authority in each state where the driver has held a license

- A current medical examiner’s certificate confirming the driver meets physical qualification standards

- A signed employment application

- Documentation of the driver’s road test or equivalent.

Carriers must also conduct annual MVR checks every year the driver is employed. When a carrier fails to build and maintain this file, or fails to conduct the required annual checks, the carrier is legally deemed to have failed to discover what was in the record.

A carrier that would have found a license suspension, a pattern of serious violations, or a failed drug test had they looked faces the same negligent hiring exposure as a carrier that found those facts and ignored them.

Federal regulations are direct on disqualified drivers: a driver who is disqualified under FMCSA regulations must not drive a commercial motor vehicle for any reason. A carrier that dispatches a disqualified driver has violated federal safety requirements, and that violation is evidence of negligence.

Understanding what commercial truck insurance requires, and the federal safety framework behind those requirements, puts the DQF obligations in context.

How an Excluded Driver Endorsement Affects Insurance Coverage

Commercial liability policies can include an excluded driver endorsement that names specific drivers who aren’t covered under the policy. When a named excluded driver causes a crash, the insurer may deny coverage for that driver’s acts under the policy’s own terms.

Insurers issue these exclusions when a driver’s history makes them too risky to insure, such as a recent DUI, pattern of at-fault crashes, or license suspension. The exclusion exists because the insurer assessed the risk and refused to accept it. When a carrier accepts that endorsement and continues to employ or dispatch the excluded driver anyway, that decision is not just a business judgment, but evidence the carrier entrusted its vehicle to someone it knew was uninsurable.

In this scenario, a coverage denial from the insurer is a claim position. It’s the insurer’s statement about what its policy covers, not a statement about whether the motor carrier itself is liable. The carrier’s direct liability for putting an excluded driver on the road is a separate legal theory that the insurer’s denial doesn’t address.

How the MCS-90 Endorsement Protects Victims Despite Policy Exclusions

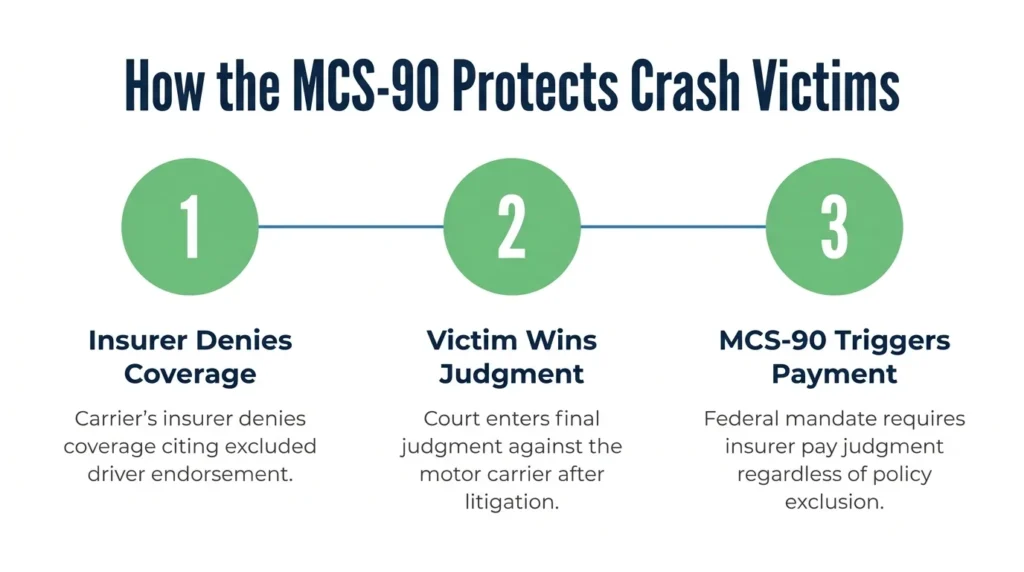

For crash victims, the most important protection against an excluded driver coverage denial comes from a federal rule the carrier’s insurer cannot avoid: the MCS-90 endorsement.

The MCS-90 endorsement is attached to every interstate motor carrier’s liability policy by federal requirement under 49 CFR Part 387. It obligates the insurer to pay any final judgment obtained against the motor carrier for public liability, even when the carrier’s own policy language would deny coverage.

The excluded driver endorsement is a policy provision. The MCS-90 is a federal mandate that supersedes policy provisions in the context of a final judgment against the carrier.

The mechanism works like this: the insurer denies coverage during the claims process. The victim pursues the motor carrier through litigation. The court enters a judgment against the carrier. The insurer must pay that judgment under the MCS-90, up to the minimum policy limits, regardless of the excluded driver endorsement. The insurer then has a right of reimbursement against the motor carrier, but that dispute is between the insurer and carrier. The victim’s judgment is paid.

The practical result is an insurer’s pre-trial coverage denial in an unauthorized driver case is not the same as no existing coverage. For truck accident claims involving interstate carriers, the MCS-90 changes what an initial denial actually means for a victim’s ultimate recovery.

The Motor Carrier’s Direct Liability for Putting an Unauthorized Driver on the Road

Regardless of how insurance responds, the motor carrier faces direct liability for the decision to put an unauthorized driver on the road. Two doctrines independently support this liability.

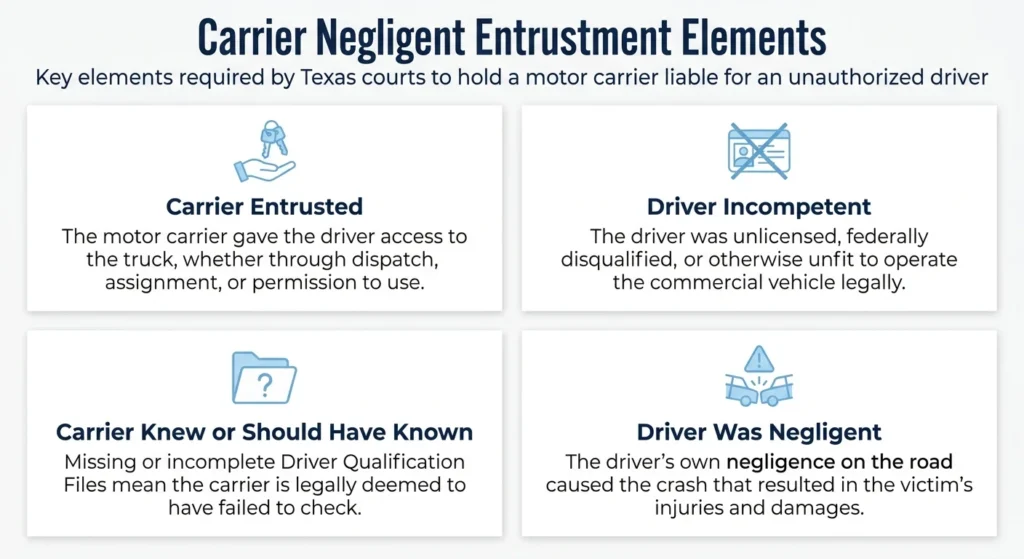

Texas courts recognize negligent entrustment as a direct theory against the vehicle owner. To establish it, a plaintiff must show:

- The carrier entrusted the truck to the driver

- The driver was unlicensed, disqualified, or otherwise incompetent

- The carrier knew or should have known as such

- The driver was negligent on the occasion

- This negligence caused the plaintiff’s injuries

In commercial crashes, the DQF answers “should have known”: if the required file was missing or incomplete, the carrier is deemed to have failed to find what was needed.

Respondeat superior operates separately. A motor carrier is vicariously liable for a driver’s negligence when the driver was acting within the scope of employment at the time of the crash. The test for respondeat superior is scope of employment, not license status. An employee driver does not need to hold a valid CDL for the carrier to face vicarious liability for that driver’s negligence while under dispatch.

Both theories directly run against the carrier. A denial by the carrier’s insurer addresses the policy. It does not address the carrier’s own liability, and it does not address the carrier’s obligations under the MCS-90.

Understanding the timeline of a Texas truck accident claim helps victims anticipate when coverage disputes surface and what they mean for the overall claim.

Reach Out to an Injury Attorney Today

When a truck driver was unauthorized, excluded from coverage, or operating without proper credentials, the insurer’s initial denial is only the beginning of the coverage analysis. The carrier’s direct liability often provides an independent path to recovery.

Angel Reyes & Associates has recovered more than $1 billion for clients from a wide range of both commercial and general vehicle accident claims for over 30 years. We work on contingency, so there’s no fee unless we win. Contact us for a free consultation.

Past results do not guarantee future outcomes.

Frequently Asked Questions

Can I still recover damages if the truck driver had no CDL?

Yes. The driver’s lack of a CDL supports negligent entrustment and negligent hiring claims against the motor carrier directly. A carrier that dispatched a driver without verifying CDL status failed its obligations under 49 CFR Part 391, and that failure is evidence of the carrier’s own negligence. The carrier’s liability runs independently of the driver’s licensing status. The MCS-90 endorsement also may obligate the carrier’s insurer to pay a final judgment, even if the driver wasn’t supposed to be driving.

What if the driver was excluded from the carrier's policy — does that mean no insurance?

An excluded driver endorsement means the insurer may deny coverage for that driver’s acts under the policy’s own terms, but it doesn’t eliminate the motor carrier’s direct liability. For interstate motor carriers, the MCS-90 endorsement requires the insurer to pay any final judgment against the carrier, regardless of the policy exclusion. The denial addresses what the policy covers, but it doesn’t address the carrier’s obligation as a liable defendant.

What is a Driver Qualification File, and why does it matter to my claim?

A Driver Qualification File is the set of documents a motor carrier must maintain under 49 CFR Part 391 for each driver: CDL verification, annual motor vehicle records, medical examiner certificates, and employment records. Gaps in the DQF — no CDL check, expired medical certificates, missing annual MVR reviews — are evidence the carrier failed to screen the driver properly. That failure supports negligent hiring and negligent entrustment claims against the carrier, independent of the driver’s own insurance.

What does the wrong CDL class mean for the carrier's liability?

A CDL class mismatch is a disqualifying condition under 49 CFR Part 391. An example is a driver with a Class B license operating a Class A vehicle. The carrier that allowed a driver to operate with the wrong class violated its federal qualification obligations. This failure supports a direct negligent hiring or negligent entrustment claim against the carrier, separate from whatever the driver’s own policy covers.

Is the trucking company responsible if the driver used the truck without permission?

It depends whether the driver was acting within the scope of employment at the time of the crash. If the driver was dispatched by the carrier or using the truck second to their job duties, respondeat superior may apply regardless of permission. If the driver took the truck entirely for personal purposes with no connection to employment, the analysis changes. However, the carrier may still face liability for failing to secure the vehicle or for negligent entrustment if the driver’s prior conduct put the carrier on notice.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...