Does Comprehensive Insurance Cover Hail, Flood, & Storm Damage in Texas?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Comprehensive coverage in Texas typically pays for hail, flood, wind, and other weather-related vehicle damage (minus your deductible).

- Texas insurers must acknowledge claims within 15 days, and after receiving all information, they must make a decision on your claim within 15 business days.

- If your claim is delayed, denied, or underpaid, Texas Insurance Code Chapters 541 and 542A provide consumer protections and legal remedies.

Imagine this: A severe thunderstorm just rolled through San Antonio, leaving golf-ball-sized hail dents across your car’s hood and roof. Or maybe flash flooding along Loop 410 caught you off guard, and now your engine won’t start. Either way, you’re looking at serious damage and wondering whether your auto insurance will actually pay for it.

The good news? If you have comprehensive coverage on your Texas auto policy, most weather-related damage is covered. The challenge is understanding exactly how your policy works, what deadlines apply, and what to do if your insurer delays or underpays your claim.

What Comprehensive Coverage Covers in Texas

Comprehensive coverage (sometimes called “other-than-collision” coverage) protects your vehicle against damage that doesn’t involve a crash with another car or object. According to the Texas Department of Insurance Auto Insurance Guide, comprehensive coverage typically covers:

- Hail damage (such as dents, cracked windshields, and broken mirrors)

- Flood and water damage (including flash floods and rising water)

- Wind damage (such as flying debris and fallen tree limbs)

- Lightning strikes

- Theft and vandalism

- Fire damage

- Animal collisions (such as hitting a deer on US-281 near Stone Oak)

Texas doesn’t require comprehensive coverage by law. However, if you’re financing or leasing your vehicle, your lender will almost certainly require it.

Even if you own your car outright, comprehensive coverage is often worth having, given how frequently Texas experiences severe weather.

What Comprehensive Coverage Does Not Cover

Understanding the limits of your policy can prevent unpleasant surprises during the claims process. That’s why it’s important to know what comprehensive coverage does not pay for:

- Collision damage (you’ll need separate collision coverage if you hit another vehicle or object)

- Mechanical breakdowns (unrelated to a covered event)

- Normal wear and tear

- Damage from poor maintenance

- Personal belongings inside your vehicle (your homeowners or renters policy may cover these)

One common point of confusion is that Texas auto policies don’t typically have “named storm” deductibles, like some homeowners policies do. Your standard comprehensive deductible applies to hail, wind, and flood damage the same way it applies to theft or vandalism.

How Deductibles & Payouts Work

Your comprehensive deductible is the amount you pay out of pocket before insurance kicks in. If you chose a $500 deductible, and your hail damage repair costs $3,000, then you’ll pay $500, and your insurer will pay $2,500.

Repair vs Total Loss

When you file a claim, your insurer will assess whether to repair your vehicle or declare it a total loss. The decision depends on comparing repair costs to your car’s actual cash value (ACV). ACV represents what your vehicle was worth immediately before the damage occurred (accounting for depreciation).

If repair costs are reasonable: Your insurer will pay for your repairs (minus your deductible). You can typically choose your own repair shop, though using an insurer-preferred shop may speed up the process.

If your vehicle is totaled: Texas insurers generally total a vehicle when repair costs exceed a certain percentage of ACV (often 70-80%, though this varies by company). In this case, you’ll receive the ACV (minus your deductible). If you owe more on your loan than the car is worth, gap coverage can help bridge the difference.

Negotiating Your Payout

The ACV offered by your insurer isn’t always final. If you believe their valuation is too low, you can do the following:

- Gather comparable vehicle listings from your area showing higher values.

- Document any recent upgrades or maintenance that increased your car’s worth.

- Request a detailed explanation of how they calculated the ACV.

- Ask about your policy’s appraisal clause, which allows a neutral third party to resolve valuation disputes.

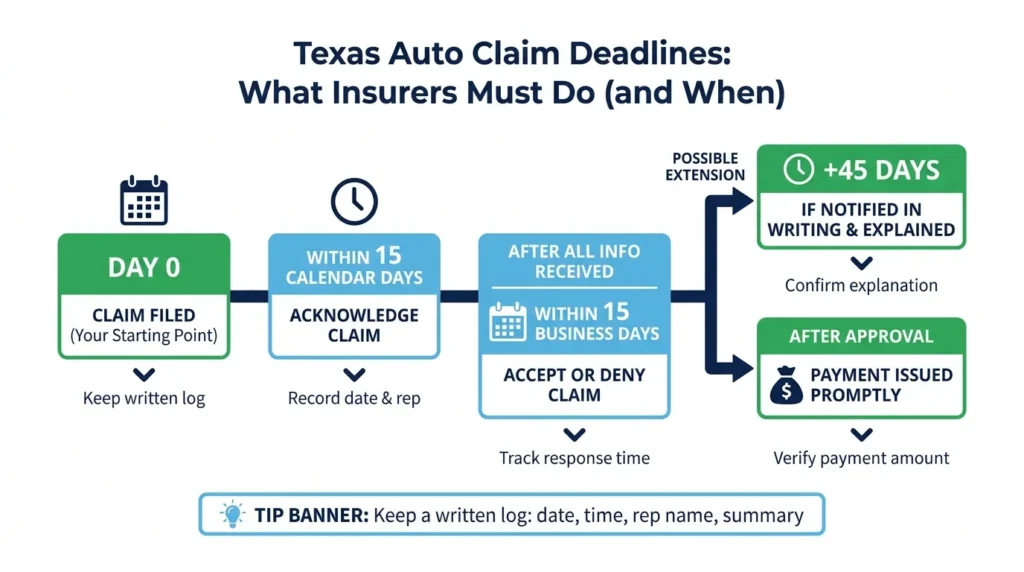

Texas Claim Deadlines & Your Rights

Texas law establishes specific timelines that insurers must follow while handling your claim. The TDI claims process guide outlines the following requirements:

- Acknowledgment: Your insurer must acknowledge your claim within 15 calendar days.

- Decision deadline: After receiving all the requested information, your insurer has 15 business days to accept or deny your claim.

- Possible extension: Insurers may take an additional 45 days if they notify you in writing and explain why more time is needed.

- Payment: Once a claim is approved, payment must be issued promptly.

Keep a written log of every interaction with your insurer. Note the date, the time, the representative’s name, and what was discussed. This documentation is critical if disputes arise later.

What to Do When Your Claim Is Delayed, Denied, or Underpaid

Insurance companies are businesses. Their goal is to resolve claims efficiently, which sometimes means offering less than your damages are worth. If you believe your claim isn’t being handled fairly, Texas law provides several protections.

Warning Signs of Unfair Claim Handling

Watch for these red flags that may indicate bad faith insurance practices:

- You are experiencing unreasonable delays without explanation.

- You have been sent requests for the same documentation multiple times.

- You have been given denials that don’t cite specific policy language.

- You are being pressured to accept a lowball offer quickly.

- The insurer is not returning calls or responding to written inquiries.

Your Legal Protections Under Texas Law

Texas Insurance Code Chapter 541 prohibits unfair or deceptive acts by insurers. This includes misrepresenting policy terms, failing to acknowledge claims promptly, and refusing to pay claims without conducting a reasonable investigation.

For weather-related property damage claims, Texas Insurance Code Chapter 542A establishes specific procedures for pursuing legal action. This chapter requires you to provide written notice to your insurer at least 60 days before filing a lawsuit, which will give them an opportunity to inspect the damage and make a settlement offer.

Steps to Escalate a Disputed Claim

If your insurer isn’t responding appropriately, consider these escalation steps:

- Submit a written complaint to your insurer’s claims supervisor, citing specific policy provisions and Texas deadlines.

- File a complaint with TDI through their online portal or by calling their consumer helpline.

- Request the appraisal process if your dispute focuses on the damage amount, rather than coverage.

- Consult with an attorney if you suspect bad faith or significant money is at stake.

An illegal insurance claim denial doesn’t have to be the end of the road. Texas consumers have real options for holding insurers accountable.

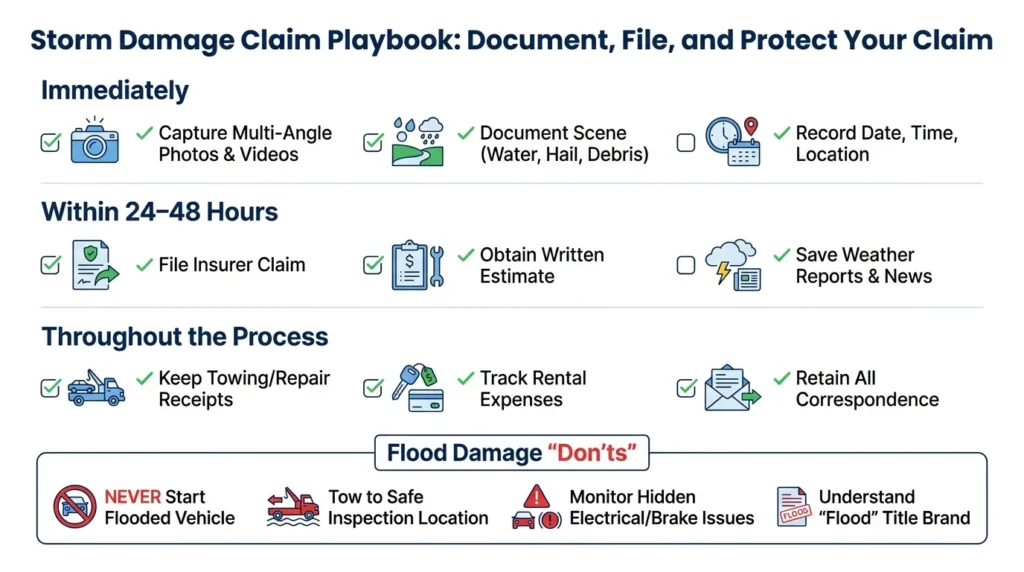

Documenting Your Damage Correctly

Strong documentation is your best protection against underpayment. Be sure to take the following steps after any weather event damages your vehicle.

Immediately:

- Take photos and videos from multiple angles, including close-ups of specific damage.

- Photograph the surrounding area to show weather conditions (such as standing water, fallen hail, or debris).

- Note the date, time, and location of the damage.

Within 24-48 hours:

- File a claim with your insurer.

- Get a written repair estimate from at least one independent mechanic.

- Save any weather reports or news coverage of the storm.

Throughout the process:

- Keep all receipts for temporary repairs or towing.

- Document rental car expenses (if this coverage is included in your policy).

- Save copies of every document you send to or receive from your insurer.

You may wonder whether you need to file a police report for insurance claims in Texas. While not always required for weather damage, a police report can help establish when and where the damage occurred.

Special Considerations for Flood Damage

Flood damage deserves extra attention because water can cause hidden problems that aren’t immediately visible. In case of a flood, the TDI flooded car guide makes the following recommendations:

- Don’t try to start a flooded vehicle. This can cause additional engine damage that may complicate your claim.

- Have the vehicle towed to a safe location for inspection.

- Be cautious about repairs. Water damage can affect electrical systems, brakes, and other safety components in ways that aren’t immediately obvious.

- Check the title. If your vehicle is totaled due to flood damage, Texas law requires a “flood” brand on the title to warn future buyers.

If you’re buying a used car after a major flood event, always run a title history check. Unscrupulous sellers sometimes move flood-damaged vehicles to other states to avoid disclosure requirements.

When to Contact an Attorney

Most straightforward weather damage claims are resolved without legal help. However, certain situations warrant professional guidance, especially if:

- Your claim involves significant dollar amounts (such as major repairs or total loss).

- Your insurer has denied coverage, and you believe the denial is wrong.

- You’ve experienced unreasonable delays that violate Texas deadlines.

- You suspect bad faith practices (such as misrepresentation or refusal to investigate).

- The damage occurred alongside a car accident or another incident involving another party’s liability.

How Angel Reyes & Associates Can Help

Dealing with insurance companies after storm damage can feel overwhelming, especially when you’re also managing repairs, rental cars, and daily life. At Angel Reyes & Associates, we’ve spent over 30 years helping Texans protect their rights when insurance companies don’t play fair.

We offer free initial consultations to evaluate your situation, and you pay no fee unless we win your case. Our team has recovered more than $1 billion for clients across Texas, and we’re available 24/7 to answer your questions. With more than 20 locations statewide, we can handle the majority of your case remotely, while giving you the personal attention you deserve.

If your weather damage claim has been delayed, denied, or underpaid, contact us today to discuss your options. You can also read what past clients have said about working with our firm on our client reviews page.

Comprehensive Coverage FAQs

Will filing a comprehensive claim for hail or flood damage raise my insurance rates in Texas?

Sometimes, but not always. Rate changes depend on your insurer, your claims history, and other rating factors. A single weather claim does not automatically mean your premium will increase.

Does comprehensive coverage pay for a rental car while my storm-damaged vehicle is being repaired?

Only if you bought rental reimbursement coverage as an add-on to your policy. Comprehensive coverage pays for covered vehicle damage, but rental costs are often handled under a separate coverage.

Can I choose my own body shop for hail or flood repairs in Texas?

Yes, in most cases, you can use whichever auto repair shop you prefer. An insurer may suggest a preferred shop, but that does not usually mean you have to use it.

What should I do if my car was flooded, and I already tried to start it?

Tell the insurer and the repair shop exactly what happened as soon as possible. Starting a flooded vehicle can worsen the damage, and being upfront will help you avoid disputes about what damages were caused by the flood.

Can I still make a weather-damage claim if I did not report the damage on the same day as the weather event?

In most cases, yes, but you should report it as soon as you discover the damage. Waiting too long can make it harder to prove what caused the damage, especially after hail, wind, or standing water events.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...