What Happens When Insurance Claims Require Arbitration?

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

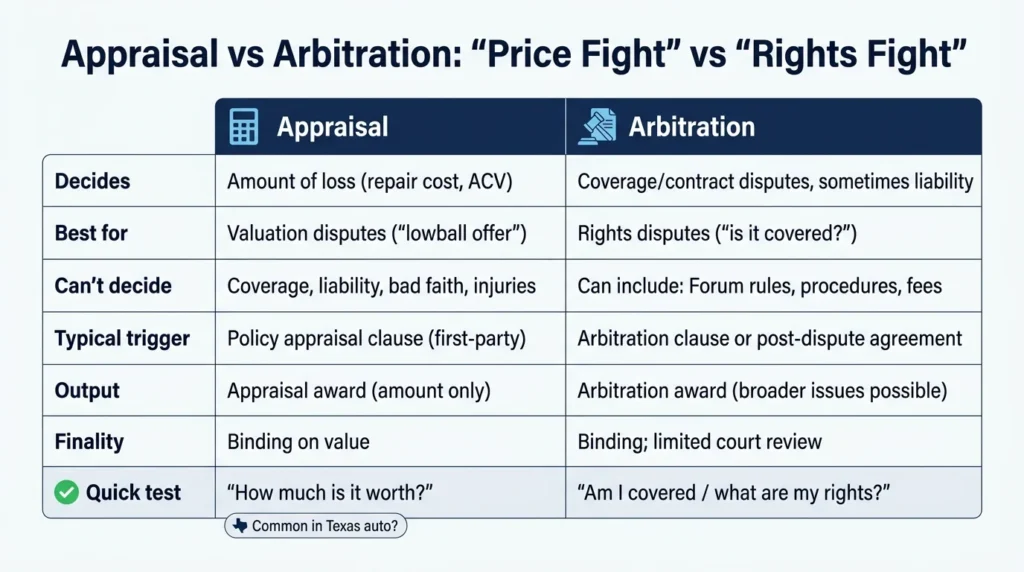

- Appraisal decides the dollar amount of vehicle damage or total loss value, while arbitration handles broader coverage and contract disputes.

- Both appraisal and arbitration awards are generally binding in Texas with very limited grounds for court review under state or federal law.

- Claimants should request the exact policy clause, document everything, and consider legal counsel before agreeing to ADR scope or signing any releases.

You were rear-ended in rush hour traffic on I-30 near Lower Greenville last week. The adjuster already sent a valuation for your totaled vehicle, but the number is thousands less than what you owe on your loan.

Now the insurance company is mentioning “appraisal” or “arbitration” as the next step. These terms sound similar, but they work very differently. Understanding which process applies to your situation can determine whether you recover fair compensation or get locked into a lowball number.

Why Insurers Claims Into Arbitration

Insurance companies have business reasons for steering disputes toward “alternative dispute resolution,” or “ADR.” ADR processes like appraisal and arbitration let insurers narrow the issues, control costs, and avoid the uncertainty of a jury trial. For claimants, recognizing these tactics early is important.

Appraisal resolves disagreements about the dollar amount of vehicle damage or total loss value. For example, if your insurer claims your vehicle is only worth $15,000 when vehicle valuation tools say it should be in excess of $15,000, appraisal can help bridge this gap.

Arbitration handles broader disputes, often involving coverage questions or contract interpretation. Inter-company arbitration is a separate system where insurers settle allocation disputes among themselves. You might hear “your claim is going to arbitration” when the process doesn’t actually involve you at all.

The practical reason insurers invoke ADR is straightforward: speed, cost control, and finality. Once a binding decision is issued, challenging it becomes extremely difficult. Before agreeing to any ADR procedure, confirm exactly what issue is being decided and whether the outcome will affect your ability to pursue additional damages.

According to the Texas Department of Insurance, most Texas auto “valuation fights” use appraisal rather than arbitration. If your dispute is about how much your vehicle is worth, appraisal is likely the relevant process. Understanding how insurance handles car accident claims can help you anticipate what comes next.

Arbitration vs Appraisal in a Texas Auto Insurance Claim

The simplest way to tell the difference: ask whether this is a “price fight” or a “rights fight.”

Appraisal answers: How much is the damage worth? What is the actual cash value of my totaled vehicle?

Arbitration answers: Does the policy cover this loss? Who is liable? What are my contractual rights?

The TDI complaint pathway confirms that appraisal typically cannot decide coverage or liability questions. If the insurer is denying your claim entirely or disputing who caused the accident, appraisal will not resolve those issues.

Both processes produce outcomes that are difficult to undo. Preparation before you agree to procedures, scope, or stipulations is critical. Once you are locked into a binding process, your leverage shrinks significantly. Our clients often tell us they wish they had understood these distinctions earlier.

What “Inter-Company Arbitration” Is

Sometimes adjusters mention arbitration when referring to insurer-to-insurer systems. These forums handle allocation and apportionment between carriers. The injured person typically does not participate directly.

This process does not automatically waive your injury claim or prevent you from pursuing damages from the at-fault driver’s insurer. If you are told arbitration is happening, ask for the coverage position letter, valuation basis, and payment breakdown in writing. Truck accident claims often involve multiple insurers, making this distinction especially important.

When a Texas Auto Insurance Appraisal Clause Can Be Invoked

Appraisal clauses appear in most Texas auto policies. Common triggers include disagreement over repair cost estimates, total loss actual cash value, or the scope of covered damage.

Appraisal is not appropriate for coverage denials, policy exclusions, liability disputes, or injury-related damages like medical bills and lost wages. If you are dealing with the other driver’s insurance, the appraisal clause in your own policy may not apply at all.

The evidence package you assemble before appraisal begins can determine the outcome. Repair estimates, dated photos, comparable vehicle listings, and condition documentation are all important. The party with better documentation typically has leverage.

Appraisal in First-Party vs Third-Party Claims

First-party claims (your own collision or comprehensive coverage) typically contain the appraisal clause. You and your insurer are both bound by the policy terms.

Third-party claims (against the at-fault driver’s insurer) work differently. You do not have a contract with that company, so their policy’s appraisal clause may not apply to you. Before spending money on an appraiser, confirm in writing which policy provision the adjuster is citing and what issue the appraisal will decide.

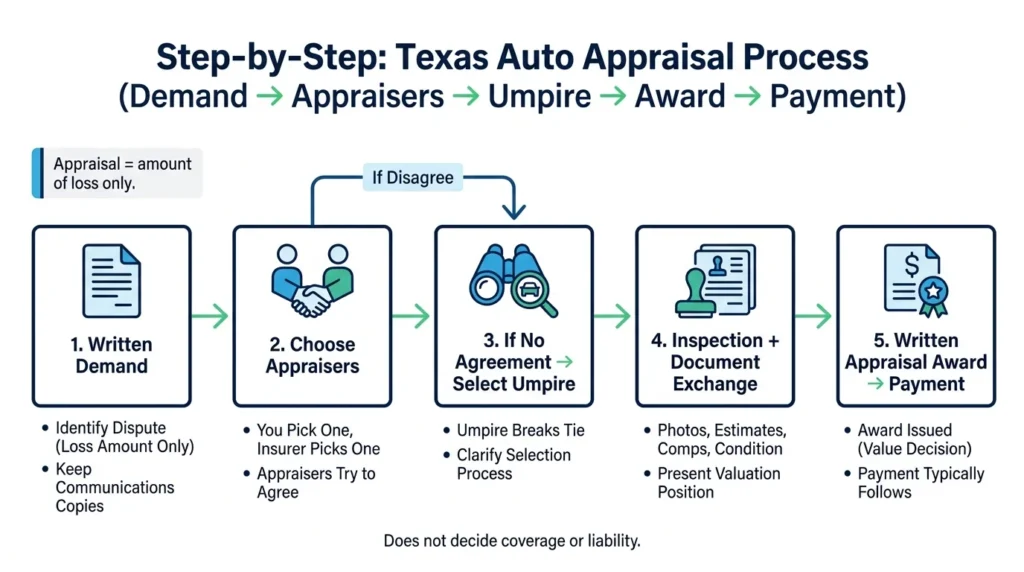

Step-by-Step: The Texas Auto Appraisal Process

Once appraisal is invoked, the process follows a predictable pattern:

- Step 1: One party sends a written demand for appraisal identifying the dispute (amount of loss only). Keep copies of everything.

- Step 2: Each side selects an appraiser. The two appraisers attempt to agree on the value. If they cannot, they select an umpire.

- Step 3: Inspection, document exchange, and valuation positions are presented. The appraisers (or umpire) issue a written appraisal award.

- Step 4: Payment typically follows the award. If the insurer delays or reduces payment after a valid award, escalation options exist.

What Appraisal Typically Costs in Texas

Cost allocation follows a standard pattern: you pay your appraiser, and the umpire fee is usually split between you and the insurer. Total costs vary based on complexity.

Cost drivers include total loss valuation research, multiple reinspections, specialized damage issues, and expert support. Before hiring an appraiser, ask for fee structures in writing. Clarify whether travel, inspection, and administrative costs are included or billed separately.

Building a Strong Appraisal Evidence Package

For vehicle damage disputes, gather dated photos, repair facility line-item estimates, supplements, and parts/paint documentation.

For total loss valuations, compile comparable vehicle listings with matching trim and options, mileage and condition records, pre-loss photos, and maintenance documentation. Websites listing similar vehicles for sale in the Dallas-Fort Worth area can support your position on actual cash value.

Keep all adjuster communications in writing. Save texts, emails, and estimate revisions. Avoid inconsistent statements that could undermine your position.

When Binding Arbitration Shows Up in Texas Accident-Related Insurance Disputes

Arbitration is less common than appraisal for vehicle value disputes, but it appears in certain coverage disagreements and contractual ADR provisions. Some policies include arbitration clauses for specific dispute types.

Arbitration can be triggered by a policy clause, a separate ADR agreement, or a post-dispute stipulation. Identify the controlling document before agreeing to arbitrate. Ask for a copy of the exact clause.

When a clause names the American Arbitration Association, AAA consumer due-process standards apply. These include screening of consumer clauses and rules about fee responsibility. Understanding the forum rules is crucial.

Texas Arbitration Act vs Federal Arbitration Act

The law governing your arbitration affects procedures and, most importantly, how limited court review will be.

The Texas Arbitration Act (Texas Civil Practice and Remedies Code Chapter 171) provides the Texas framework for arbitration procedure and post-award court motions. The Federal Arbitration Act (9 U.S.C. Section 10) establishes narrow grounds for vacating awards when federal law governs.

Regardless of which law applies, courts generally do not re-try the case. Your best opportunity to affect the outcome is before and during arbitration. Maintain a complete record, organize exhibits, and make timely objections. Consider consulting with experienced attorneys before the hearing date is set.

How Final Is an Appraisal or Arbitration Decision in Texas?

Most readers want the same answer: “Is this really final?”

Appraisal awards are generally binding on the amount of loss when properly invoked. They do not decide coverage questions. If the insurer accepts the appraisal number but still will not pay, you may have additional options.

Arbitration awards are binding with very limited judicial review. Courts do not revisit the merits simply because one party disagrees with the outcome.

Both Texas law and federal law provide narrow statutory grounds to vacate or modify awards. These include arbitrator misconduct, evident partiality, or the arbitrator exceeding their authority. Deadlines for challenging awards are strict. If you are considering a challenge, talk to a lawyer immediately.

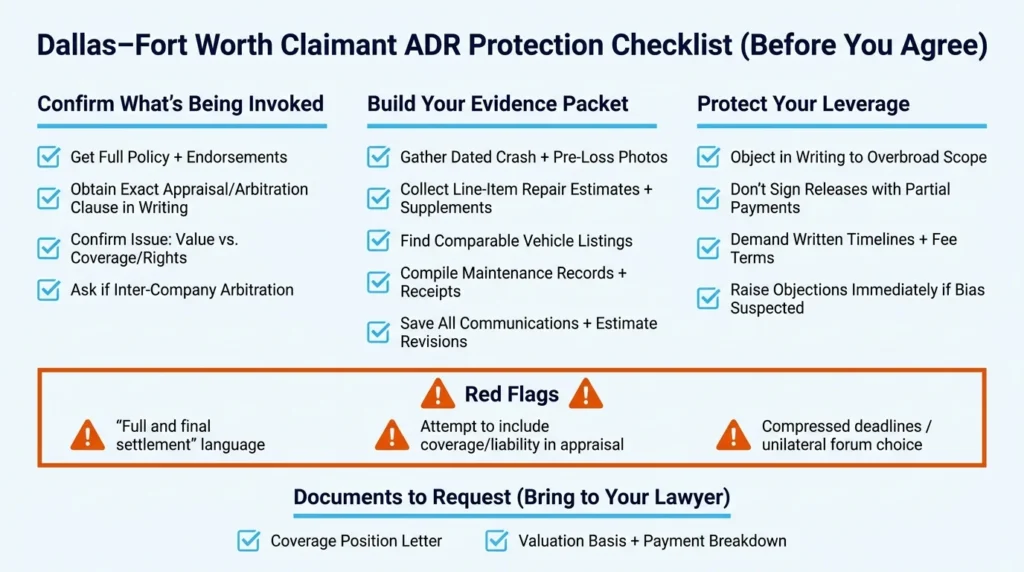

Red Flags Before Agreeing to ADR

Many “lost rights” problems start with paperwork, not the hearing itself.

Watch for overbroad scope language attempting to fold coverage, liability, or extra-contractual issues into what should be a simple appraisal. Watch for releases and “full and final settlement” language tied to partial payments. Have any release reviewed before signing. Watch for compressed timelines and unilateral forum selection that does not match the policy clause.

Dallas-Fort Worth Claimant Playbook: Protecting Your Rights

If an insurer invokes ADR on your claim, take these steps:

Get the policy and the exact clause. Request the appraisal or arbitration wording, endorsements, and any ADR rules referenced.

Lock down your timeline and evidence. Gather repair estimates, photos, towing and storage receipts, rental records, and all claim communications.

Know your escalation options. If valuation or payment stays low, you can negotiate, request appraisal (for amount disputes), or file a complaint with the Texas Department of Insurance.

Recognize when you need legal help. Injury components, truck crash complexity, coverage denials, suspected bad-faith tactics, or ADR being used to limit legitimate damages all warrant professional guidance. A demand letter may be an appropriate next step.

Talk to a Texas Car Accident Attorney About Your Claim

Insurance companies use ADR processes strategically. Understanding whether you are facing appraisal or arbitration, what each process can decide, and how binding the outcome will be puts you in a stronger position.

Angel Reyes & Associates has spent over 30 years helping Texas accident victims navigate insurance disputes. We offer free initial consultations and work on contingency, meaning no fee unless we win. Our team has recovered more than $1 billion for clients across the state. We have more than 20 locations throughout Texas and can handle most of your case remotely.

If an insurer is pressuring you toward ADR or offering less than your claim is worth, contact us to discuss your options.

Past results do not guarantee future outcomes.

Claim Arbitration FAQs

Can you still use your own repair shop during an appraisal dispute in Texas?

Usually yes, but the insurer may only agree to pay what it determines is the covered amount of loss under the policy. If repairs have already started, keep the damaged parts, photos, and all invoices so the condition and scope of damage can still be evaluated.

What if the insurance company says some of the damage was pre-existing?

That kind of dispute can complicate appraisal because the parties may disagree about what damage came from the crash versus earlier wear or prior accidents. Photos taken right after the wreck, prior service records, and a detailed body-shop estimate can help separate old damage from new damage.

Does a lienholder or leased vehicle change how a total-loss dispute works?

It can affect who gets paid and how the payment is issued, because the lender or leasing company may have rights under the policy or vehicle contract. Even if the valuation is resolved, you may still owe money if your loan balance is higher than the vehicle’s actual cash value.

Can an appraiser or arbitrator make the insurer pay for a rental car or storage fees too?

Not automatically. Those items usually depend on the coverage you bought, the policy limits, and whether the charges are part of the dispute being submitted, so it is important to check the policy language carefully.

What should you do if the insurer names an appraiser or umpire you think is biased?

Raise the concern in writing right away and ask for the basis of that person’s selection and any known relationships that could affect neutrality. Waiting too long to object can make it harder to challenge the process later.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...