How to File a Motorcycle Property Damage Claim in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Property damage and injury claims are handled by separate adjusters on different timelines in Texas.

- When a total-loss offer is too low, Texas law gives you the right to demand a binding appraisal.

- Damaged helmets and riding gear are recoverable personal property and belong in your claim.

Your bike is sitting in a tow yard somewhere in San Antonio, and the other driver’s insurance company has already called twice. You know you need to file a claim, but nobody has explained how this actually works. The property damage side of a motorcycle crash claim follows its own rules, its own timeline, and its own adjuster.

Most riders never learn that until they are already behind.

Property Damage Runs on a Separate Track

The insurer assigns two different adjusters to your case after a motorcycle accident. One handles bodily injury. The other handles property damage. These are separate departments with separate files, and the property damage adjuster can close your bike’s file long before your injury claim reaches any kind of resolution.

This separation works in your favor if you understand it. You do not need to wait for your injuries to heal before pursuing compensation for your motorcycle. The two claims operate at the same time.

Texas law sets specific timelines for how insurers must handle property damage claims. Under Texas Insurance Code Chapter 542, an insurer must acknowledge your claim within 15 business days of receiving written notice and then accept or reject it within 15 business days of receiving all required documentation.

If the claim is accepted, payment must follow within 5 business days. Missing those deadlines triggers an 18% annual interest penalty on the unpaid amount, plus the right to recover attorney fees.

The filing deadline for property damage follows the same two-year window as a personal injury claim under the Texas Civil Practice and Remedies Code (CPRC) § 16.003. File the property damage claim immediately. Do not let it sit while you focus on your medical care.

Step 1: File the property damage claim right away. Contact the at-fault driver’s insurer and open a claim. Ask for the claim number and the name and direct contact for the property damage adjuster assigned to your file.

Step 2: Document the damage thoroughly. Photograph your motorcycle from every angle, including close-ups of every bit of damage. Take pictures of road conditions, skid marks, and the crash scene while you can.

Step 3: Preserve your helmet and riding gear. Do not discard, repair, or clean any gear worn during the crash. Your helmet and jacket are property damage, and you will need them as evidence.

Step 4: Obtain your accident report. Request a copy from the police department that responded to the scene. This establishes fault on the record and becomes a foundation document for both your property damage and injury claims.

How Insurers Value a Totaled Motorcycle

Under Texas Transportation Code § 501.091, a vehicle is a total loss when the cost of repairs plus its salvage value equals or exceeds its actual cash value (ACV) Texas sets that threshold at 100 percent of ACV, unlike states that trigger a total-loss review at 70 or 75 percent.

In practice, insurers will often begin evaluating for total loss when repair estimates reach 70 to 80 percent of your motorcycle’s ACV, well before the statutory ceiling.

How ACV Is Calculated

The insurer does not determine your bike’s value internally. They commission a report from a third-party valuation company, most often CCC ONE or Audatex. These platforms pull data from recent comparable vehicle listings in your area and apply a series of adjustments for mileage, condition, and market factors.

The system produces a number. That number is presented to you as the offer. What the system does not tell you is how it got there, which comparable vehicles it used, what condition grade it assigned, or what adjustments pulled the final figure down.

You are entitled to the full valuation report, not just the conclusion. Request it in writing.

Why Motorcycles Are Frequently Undervalued

The comparable-vehicle problem hits motorcycles harder than cars. Automated valuation systems work best when there are dozens of similar vehicles recently sold in the same market, but motorcycles aren’t always so lucky.

The system may source comparables from weaker motorcycle markets, lower trim models, or higher-mileage units when there is not enough local data. That skews the valuation downward before anyone reviews your claim.

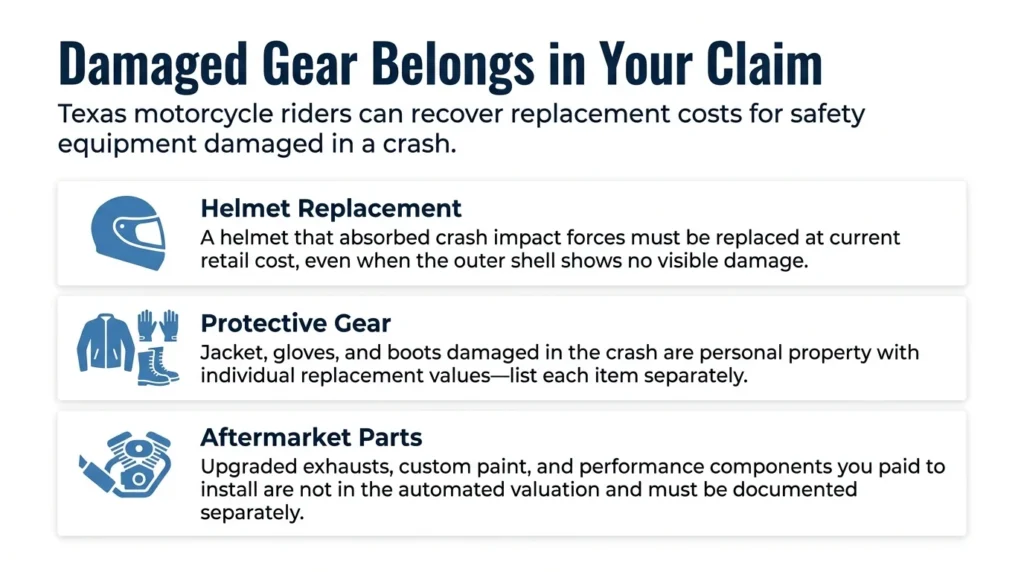

Aftermarket parts and custom modifications create a second problem. A stock valuation for your year and model does not account for the upgraded exhaust, custom paint, premium tires, or performance components you paid to install. Those upgrades may be worth thousands of dollars, and the automated report will not acknowledge them unless you force the issue.

You can learn more about how motorcycle accident settlements work in Texas, including how property damage fits into an overall recovery strategy.

How to Counter a Low Total-Loss Offer

You are not required to accept the insurer’s first number. Pushing back on a total-loss valuation is a formal process, and it works when you approach it with documentation rather than emotion.

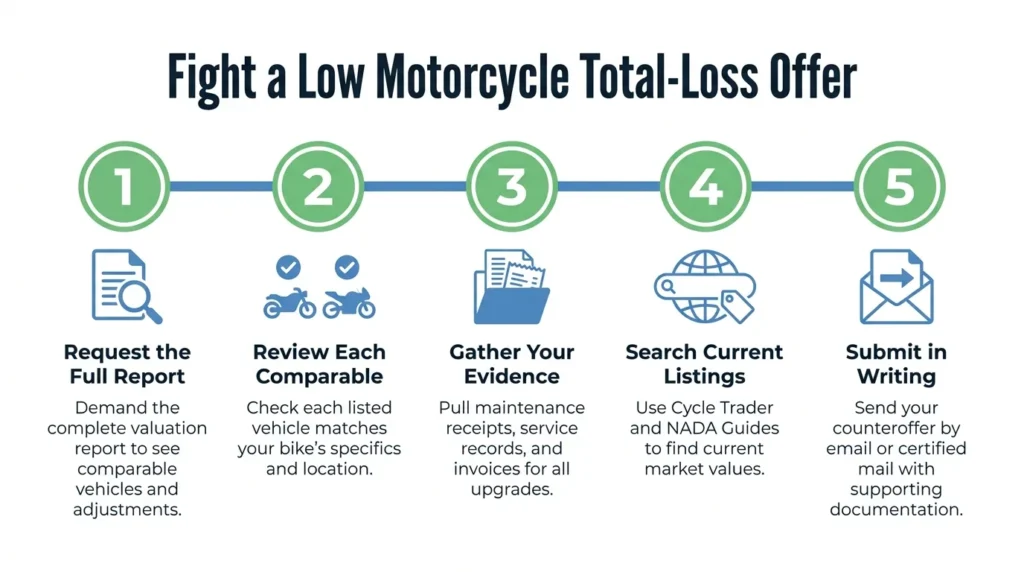

Request the complete valuation report in writing. That document shows the comparable vehicles the system used, the condition grades assigned, and every adjustment that reduced the final figure.

Review each comparable listing. Verify it is actually available for sale, matches your bike’s actual trim level and configuration, and comes from a comparable market. A system that built your valuation around listings from out-of-state markets with weaker demand is not giving you an accurate local value.

Gather competing evidence. Pull maintenance records, service receipts, and receipts for any aftermarket parts or upgrades you added.

Search current listings on Cycle Trader and similar platforms for bikes matching your year, make, model, trim, and mileage. Cross-reference with current NADA Guides values. Those listings and guides form the basis of your counteroffer.

Submit a written counteroffer with all documentation attached. A phone call is not a formal dispute.

Send your counteroffer by email or certified mail, identifying each specific error in the insurer’s report, stating the bike value you believe is accurate, and including your supporting evidence.

An attorney who handles motorcycle accident claims can review the insurer’s valuation report and identify the specific errors that support a higher offer, often before you send any written response.

If the insurer will not move after your written dispute, Texas law gives you a formal escalation path. Texas Insurance Code Chapter 1813 requires every personal auto policy issued or renewed in Texas on or after January 1, 2026, to include a binding appraisal provision.

Either you or the insurer can demand an appraisal. Each side has an independent appraiser, and if the two cannot agree, a neutral umpire comes in to resolve the dispute. The award is binding, with narrow exceptions for fraud or material mistake.

An independent appraisal costs money upfront, but if your bike’s true value is significantly higher than the insurer’s offer, the process often pays for itself.

Claiming Your Helmet & Gear as Property Damage

Your helmet, jacket, gloves, boots, and any other riding gear damaged in the crash are recoverable as personal property. They belong in your property damage claim, not as an afterthought.

A helmet that absorbed impact forces during a crash must be replaced even if the outer shell shows no cracks or visible damage. The internal foam is designed to compress on impact and cannot be reliably reused after a significant collision. Replacement cost is the standard, not depreciated value for an item that can no longer be used safely.

Photograph every item of damaged gear before you do anything else with it. Get replacement cost quotes directly from the retailer or the manufacturer’s website.

A quality helmet can cost several hundred dollars. A full gear set including jacket, gloves, and boots can easily exceed a thousand dollars. List each item separately, document the current replacement cost, and attach that documentation to your property damage claim.

Do not accept an offer that lumps your gear into the overall settlement without addressing it line by line. Each item has a replacement value, and each belongs in the claim.

Work with an Attorney on Your Property Damage Claim

Property damage claims after a motorcycle crash seem straightforward until you are facing a valuation report that underprices your bike by thousands of dollars, a slow adjuster, or an insurer that will not acknowledge your written dispute.

Angel Reyes & Associates has spent over 30 years helping injured Texans recover what they are owed after motorcycle accidents. If the insurer declares your bike a total loss and the offer does not reflect what your motorcycle was actually worth, or if the adjuster has gone quiet and the timeline has slipped, we can review your claim and your options at no upfront cost.

We work on contingency, which means you pay nothing unless we recover compensation for you. Contact us today for a free consultation.

Past results do not guarantee future outcomes.

Motorcycle Property Damage FAQs

Can I claim a rental vehicle while my motorcycle is being repaired or replaced?

Yes, loss of use is a recoverable element of your property damage claim in Texas. The at-fault driver’s insurer is responsible for your transportation costs while your motorcycle is being repaired or replaced, though the insurer may try to limit the daily rate or the total duration.

What if the at-fault driver's insurance does not cover the full value of my motorcycle?

If the at-fault driver’s policy limits are lower than your loss, you may be able to recover the remaining amount through your own underinsured motorist property damage coverage, if you carry it. Texas does not require this coverage, so check your own policy to know what is available.

Can I still claim diminished value if my motorcycle was repaired and not totaled?

Yes. Under Texas law, you can pursue a diminished value claim against the at-fault driver’s insurer even after repairs are complete. Diminished value compensates you for the reduction in your motorcycle’s market value because it now carries an accident history, even after being fully repaired.

What should I do if the insurance adjuster stops returning my calls or responding to my messages?

Document every unanswered attempt to contact the adjuster in writing, then send a formal written notice to the insurer referencing the Texas Insurance Code Chapter 542 deadlines. If the insurer continues to delay without a valid reason, you may have a claim for bad-faith handling in addition to your property damage claim.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 55,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...