How Motorcycle Accident Settlements Work in Texas

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- Texas riders have two years from the crash date to file a motorcycle injury lawsuit.

- Riders found 51 percent or more at fault recover nothing under Texas comparative fault rules.

- Settlement value tracks injury severity, policy limits, fault allocation, and documented losses.

After being clipped by a driver on Loop 410, you’re now facing hospital bills while an adjuster calls with questions that feel like traps. The first offer in your inbox doesn’t come close to covering what you’ve lost, and the pressure is mounting. So, how is a fair settlement actually calculated?

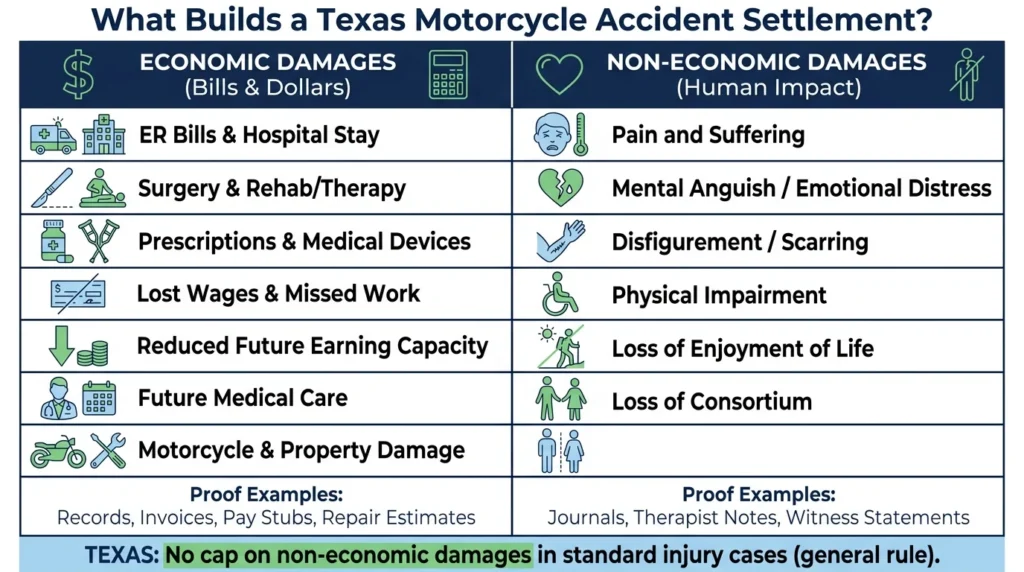

What Goes Into a Motorcycle Accident Settlement Amount

A Texas motorcycle settlement is built from two damage categories:

- Economic damages cover measurable losses like medical bills, lost wages, future treatment, and motorcycle repair.

- Non-economic damages cover pain, emotional distress, and loss of enjoyment of life.

Texas does not cap non-economic damages in standard injury cases, so severe crashes can produce significant awards beyond out-of-pocket costs.

Economic damages are the easier numbers to prove. Hospital records, surgery invoices, physical therapy bills, and pay stubs build the foundation. Future costs matter too, especially when injuries require ongoing care or limit your ability to work.

Non-economic damages are harder to quantify but are often larger. A serious crash changes how you sleep, work, ride, and spend time with family. Those losses are real, and Texas law allows recovery for them.

Insurers know this and still open low, with the first offer rarely reflecting a rider’s full damages picture. Reviewing your full inventory of losses before responding can mean the difference between covering bills and leaving money behind. NHTSA motorcycle safety data shows that motorcyclists face significantly higher injury risks than passenger vehicle occupants, which is why documenting every common injury sustained in motorcycle crashes matters so much in settlement talks.

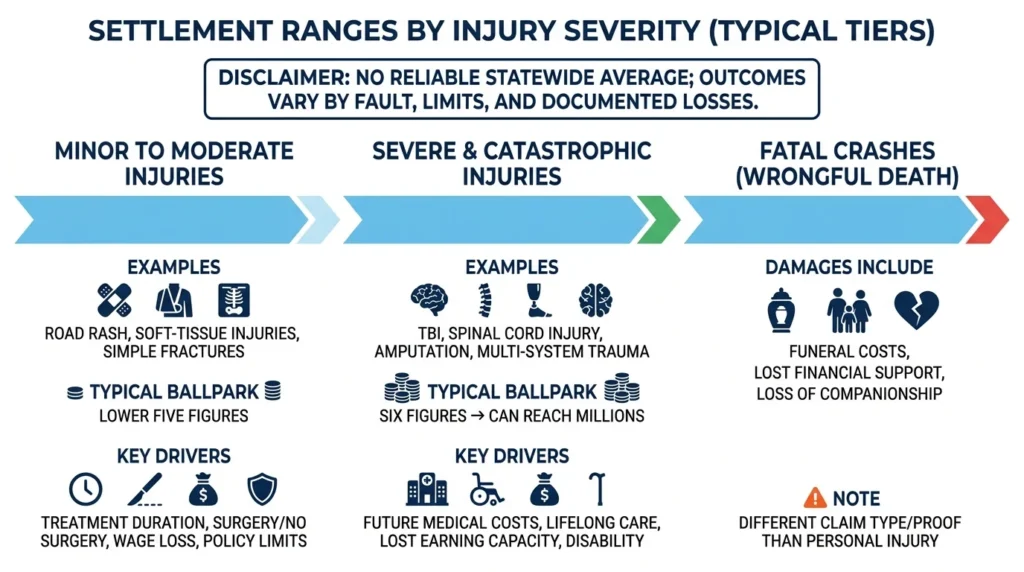

Average Motorcycle Accident Settlements by Injury Severity

Settlement values track injury severity more than any other single factor. While Texas does not publish a reliable statewide average, because outcomes depend on fault, insurance limits, and documented losses, what we can describe is how cases tend to cluster by injury tier, so you can locate your situation on the map.

Minor to Moderate Injuries

These cases usually involve road rash, simple fractures, or soft-tissue injuries that resolve within months. Settlements typically land in the lower five figures. Treatment duration, whether surgery was needed, and the at-fault driver’s policy limits drive the final settlement number.

Wage loss during recovery also matters. A two-week absence from work looks very different from a six-month layoff. State data on injury patterns from TxDOT crash statistics helps confirm how riders are typically hurt and where evidence gaps appear.

Severe & Catastrophic Injuries

Traumatic brain injuries, spinal cord damage, amputations, and multi-system trauma sit in this tier. Settlements commonly reach six figures and can climb into the millions when future medical costs and lost earning capacity are fully documented. Permanent disability changes the math because the rider’s losses extend across a lifetime.

Fatal crashes shift into Texas wrongful death claims. Surviving family members can recover funeral costs, lost financial support, and loss of companionship. These cases require different proof and different statutory grounding than personal injury claims.

Factors That Raise or Lower Your Settlement

Several variables push settlement values up or down. Clear liability on the other driver, well-documented injuries, high policy limits, and evidence of gross negligence all increase value, while shared fault, treatment gaps, low policy limits, and pre-existing conditions all decrease it. Knowing where your case stands on each factor lets you evaluate any offer with open eyes.

Gross negligence, fraud, or malice opens the door to exemplary damages under Texas Civil Practice and Remedies Code (CPRC) § 41.003. Drunk driving and street racing are common triggers in motorcycle crashes. To recover exemplary amounts above actual losses, a rider must prove by clear and convincing evidence that the at-fault driver acted with malice, fraud, or gross negligence—a higher burden than ordinary negligence.

Texas Transportation Code § 661.003 requires helmets for riders under 21; riders over 21 may be exempt if they meet training or insurance conditions. Even when riding helmetless is legal, insurers argue that a helmetless rider assumed extra risk for head and facial injuries. That argument can resurface during legal proceedings as a comparative fault claim intended to reduce the total settlement.

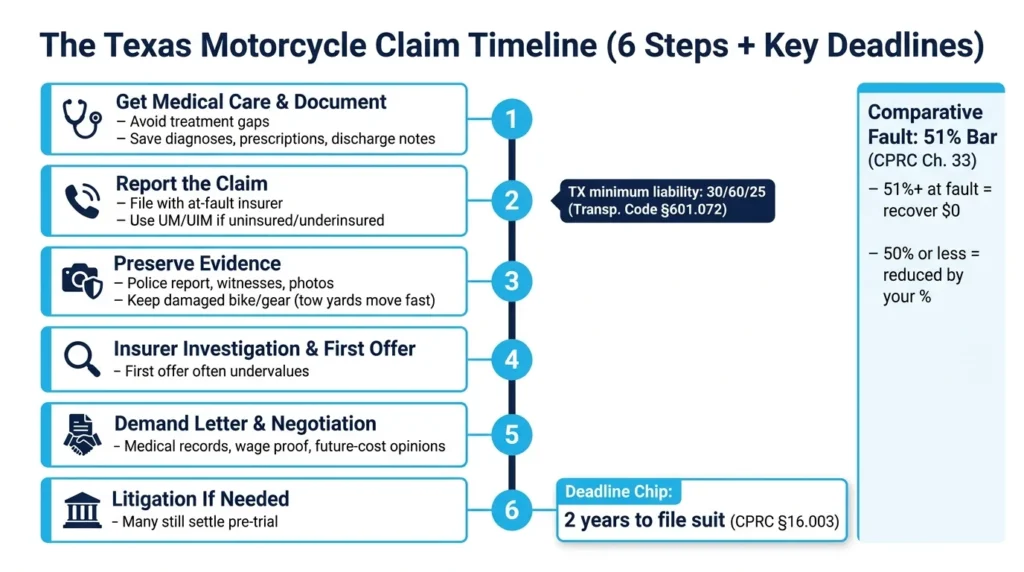

Under Texas’s modified comparative fault rule (CPRC Chapter 33), you cannot recover any damages if you are found 51 percent or more at fault for the accident. If your fault is 50 percent or less, your settlement is reduced by the specific percentage of your responsibility. The 51 percent comparative negligence rule is the single biggest reason fault allocation matters so much in motorcycle cases.

Adjusters and juries sometimes assume riders take on extra risk just by being on a bike, and they push fault percentages higher than evidence supports. Strong documentation and witness statements push back against that bias. Reviewing strategies for maximizing a Texas injury settlement can help riders see how the same principles apply to motorcycle claims.

The Motorcycle Claim Settlement Process in Texas

Most Texas motorcycle settlements follow a predictable path from crash to resolution. Understanding each step helps you spot moments where claim value is won or lost. The lifecycle below is what we see in the majority of cases handled across the state.

Step 1: Get medical care and document everything. Treatment gaps are the first thing insurers attack. Every visit, diagnosis, and prescription becomes evidence.

Step 2: Report the claim. File with the at-fault driver’s insurer. When that driver is uninsured or underinsured, file with your own carrier under Uninsured Motorist (UM)/Underinsured Motorist (UIM) coverage. Texas minimum liability limits are 30/60/25 under Texas Transportation Code § 601.072, which often falls short of what severe motorcycle injuries cost.

Step 3: Preserve evidence. Gather and save the police report, witness contacts, scene photos, injury photos, and the damaged bike itself. Tow yards crush motorcycles fast, so move quickly.

Step 4: The insurer investigates and makes a first offer. First offers almost always undervalue the claim. Treat them as a starting point, not a conclusion.

Step 5: Demand letter and negotiation. A demand letter backed by full medical records, wage documentation, and expert opinions on future costs usually produces a higher counter-offer. This is where preparation pays off.

Step 6: Litigation if negotiation stalls. Most cases still settle before trial, but filing suit often changes insurer behavior. Texas riders have two years from the crash date to file suit under CPRC § 16.003. Miss that deadline and the claim is gone.

If you have already received a first offer, comparing it against your documented losses is the single most useful thing you can do before responding. An attorney handling motorcycle accident cases can run that analysis at no upfront cost. Riders comparing crash claim valuation often find it useful to see how Texas car accident settlements average out for context on insurer behavior.

Speak With an Attorney Today!

With over 30 years of experience and $1 billion recovered, Angel Reyes & Associates features a team of more than 600 dedicated professionals available 24/7 across more than 20 offices statewide to handle motorcycle cases in both English and Spanish.

Our trial-ready Texas attorneys can review your settlement offer at no cost to you. We work on contingency, meaning no fee unless we win, and because our Texas case results reflect the kinds of outcomes our team pursues for riders across the state, you should contact us today to talk through your claim.

Past results do not guarantee future outcomes.

Motorcycle Accident Settlement FAQs

How long do I have to accept or reject a motorcycle accident settlement offer in Texas?

There is no fixed legal deadline for accepting a settlement offer, but the two-year statute of limitations controls how long you can wait before losing the right to file suit. If negotiations stall and you let that window close without filing, you forfeit your claim regardless of the offer on the table.

What happens to my settlement if the at-fault driver has no insurance and I have no UM/UIM coverage?

Without uninsured motorist coverage, you would need to pursue the at-fault driver directly through a lawsuit and attempt to collect any judgment from their personal assets. In practice, uninsured drivers often have few collectible assets, which makes recovery difficult even when liability is clear.

Can my medical bills be paid before my motorcycle accident settlement is finalized?

Medical providers may agree to a lien against your future settlement instead of requiring immediate payment, which allows treatment to continue while the claim is still open. Some health insurance plans will also cover crash-related treatment, though the insurer may seek reimbursement from your settlement proceeds once the case resolves.

Does Texas allow me to recover damages for damage to my riding gear, not just my motorcycle?

Personal property damaged in a crash, including helmets, jackets, and other gear, is recoverable as part of your economic damages claim. You would need to document the replacement cost or repair cost for each item, just as you would for the motorcycle itself.

What does "maximum medical improvement" mean, and why does it affect my settlement timing?

Maximum medical improvement, often called MMI, is the point at which your doctor determines your condition has stabilized and further recovery is unlikely. Settling before reaching MMI is risky because future medical costs and any permanent impairment may not yet be fully known, which can lead to accepting less than your injuries will ultimately cost.

About the Authors

Alex Ivanov

Writer

Alex Ivanov is a personal injury attorney at Angel Reyes & Associates, focused on car, truck, and motorcycle accident cases. Licensed in Texas and multiple federal districts, Alex brings international legal experience and a global education to his practice. He earned his LL.M. from Texas A&M University School of Law after graduating from Belarussian State University in 2016. Alex is fluent in Russian, English, Ukrainian, and Belarussian, and is recognized by multiple national trial lawyer associations for his results and leadership under 40.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Angel Reyes

Reviewer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business...