Illegal Insurance Denial in Texas: How to Spot Bad Faith & Protect Your Claim

Every article on this site is researched by our internal team, reviewed for legal accuracy against current Texas law, and held to State Bar of Texas advertising standards before publication. We do not publish content that overstates outcomes or makes promises about results.

Learn more about our

editorial standards .

Key Takeaways

- You can often strengthen a denied or lowballed claim by demanding a clear written explanation and responding with a focused evidence packet.

- Red flags like shifting denial reasons, weak investigation, and long unexplained delays should be documented in a timeline and communication log.

- Early action matters, especially in commercial and truck cases where time-sensitive evidence may disappear without preservation steps.

Illegal Insurance Denial in Texas: How to Spot Bad Faith and Protect Your Claim

You reported the wreck. You shared your side of the story truthfully. You sent records and bills supporting your testimony. Then the letter comes: the insurance company denied your claim or offered far less than your documented losses.

A denial letter is not always the end of the road. A denial or low offer may cross the line when the company ignores evidence, misstates policy terms, or drags out the claim without a real reason. The good news is you have options when it comes to fighting back.

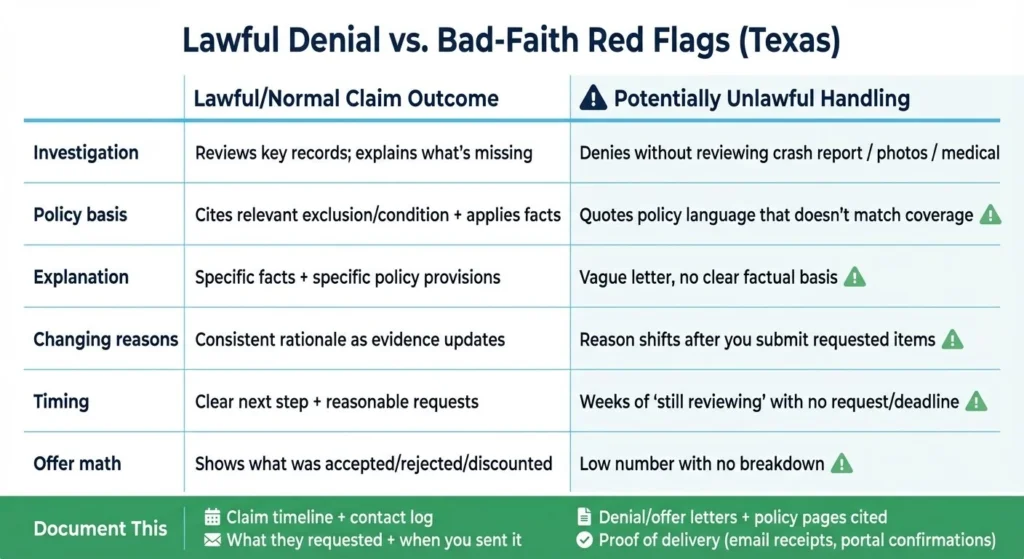

Lawful Denials vs. Potentially Unlawful Denials in Texas

Not every denial is wrongdoing. Insurers can deny claims for valid reasons, including exclusions that actually apply, missing documentation, or a failure to comply with a policy requirement.

The concern is how the insurer reached the decision.

Texas Insurance Code § 541.060 prohibits certain unfair settlement practices, including denying a claim without conducting a reasonable investigation and failing to provide a reasonable explanation tied to the policy and the facts. Illegal insurance claim denial could leave them liable for penalties.

Some lawful reasons insurers deny claims include:

- A clear exclusion applies to the loss

- The insurer lacks proof of causation or damages (medical records, bills, wage loss proof)

- A policy requirement was missed (notice, cooperation, examinations, or documentation)

Even with a valid issue, an insurer generally still needs to review relevant information and explain the decision in writing.

That being said, sometimes denials are not given after a thorough review or investigation. Some red flags that suggest the process was not fair can include:

- The adjuster denies the claim without reviewing key records (medical records, photos, or the crash report)

- The insurer cites policy language that does not match coverage

- The denial letter is vague and does not explain what facts or documents drove the decision

- The denial reason changes after you submit the exact items the insurer asked for

In Dallas and across Texas, these disputes often show up after “minor impact” arguments, liability disputes, or treatment gap narratives. Truck and commercial claims can add more friction because there may be multiple carriers and multiple layers of coverage.

First-Party vs. Third-Party Claims

Before you respond to a denial, identify what type of claim you are dealing with. First-party claims are when you are using your own policy, such as PIP, MedPay, UM/UIM, collision, or comprehensive. Third-party claims are when you pursue the at-fault driver’s liability insurance.

The tools and timelines can differ. Prompt payment rules often come up in first-party claims more than third-party disputes, and some coverage disputes hinge on policy wording.

Common issues with your own insurer can include:

- UM/UIM disputes over fault, causation, and the value of injuries

- PIP or MedPay reductions based on “reasonable and necessary” treatment arguments

- “Independent” reviews used to cut bills or limit care

If an insurer relies on a medical review, request the report in writing and document when you asked and when you received it.

The other driver’s insurer is not your advocate. When filing a third-party claim, expect pushback on liability, treatment, and damages. Be careful with recorded statements and broad medical authorizations. Those requests can be used to shape the claim narrative.

If you need a practical walkthrough, read: Should I Talk to the Other Driver’s Insurance?

Bad-Faith Warning Signs to Document Early

You do not need to guess what the insurer is doing. You can track it. Watch for patterns like these:

- Shifting reasons: The denial basis changes each time you address the last issue

- Thin investigation: No witness outreach, no meaningful review of records, no clear evaluation path

- Policy misstatements: The adjuster describes limits or exclusions that do not match your declarations or policy wording

- Unexplained delays: Weeks of “still reviewing” with no specific request, deadline, or next step

- Low offers without math: The number appears with no explanation of what was accepted, rejected, or discounted

Poor Communication

Poor communication can leave an insurance company with wiggle room they can exploit to deny your claim. In fact, poor communication tactics are a method they might use against you. Here are a few of them to watch for:

- Pressure for a recorded statement early, before you have records and a timeline

- Requests for blanket medical authorizations rather than specific records

- “Phone only” adjusting that leaves no paper trail

Whenever possible, follow up by email and confirm what was said, what was requested, and the expected next step.

Document Loops

If the insurer keeps requesting items you already sent, treat it as a process issue. Send the items again with a short cover note listing what is attached, the dates previously provided, and confirmation receipts. Keep records of everything you send, including dates and times you send them. This can help you prove bad faith should you need to escalate your claim to a lawsuit.

Texas Claim-Handling Rules That Often Apply

Two areas come up often in denial and delay disputes.

- Unfair settlement practices: Texas Insurance Code § 541.060

- Prompt payment timelines: Texas Insurance Code Chapter 542, often called the Prompt Payment of Claims Act

Prompt payment rules focus on acknowledgment, requests for items, decision timing, and payment timing. These rules can be coverage-specific and fact-specific, so it is important to track your dates and documents.

Key provisions include:

- Acknowledgment and investigation (§ 542.055)

- Accept or deny after receiving requested items (§ 542.056)

- Pay after acceptance (§ 542.057)

- Potential liability for violations (often discussed as statutory interest plus attorney’s fees in certain cases): (§ 542.060)

Even if you are not sure which provisions apply, tracking the timeline helps you spot unreasonable gaps and forces clearer communication.

What to Do Right After a Denial, Delay, or Low Offer

Your first steps should build leverage and reduce confusion.

- Read the letter closely. Highlight the stated reason, any cited policy language, and any response deadlines.

- Ask what was reviewed. Request, in writing, the documents the insurer relied on and what specific items would change the decision.

- Move everything into writing. Confirm phone calls with short follow-up emails.

- Build a simple claim timeline. Include crash date, treatment start, major diagnosis dates, document submissions, and adjuster contacts.

- Keep treating if you are still injured. Gaps in care often get used against causation and severity.

Some injuries take time to show up, including certain back, neck, and head symptoms. In limited situations where an injury was not reasonably discoverable right away, courts may apply a “discovery rule” analysis that can affect when a deadline starts. This is highly fact-specific, so do not assume extra time applies. Act early and document when symptoms began and when you first sought care.

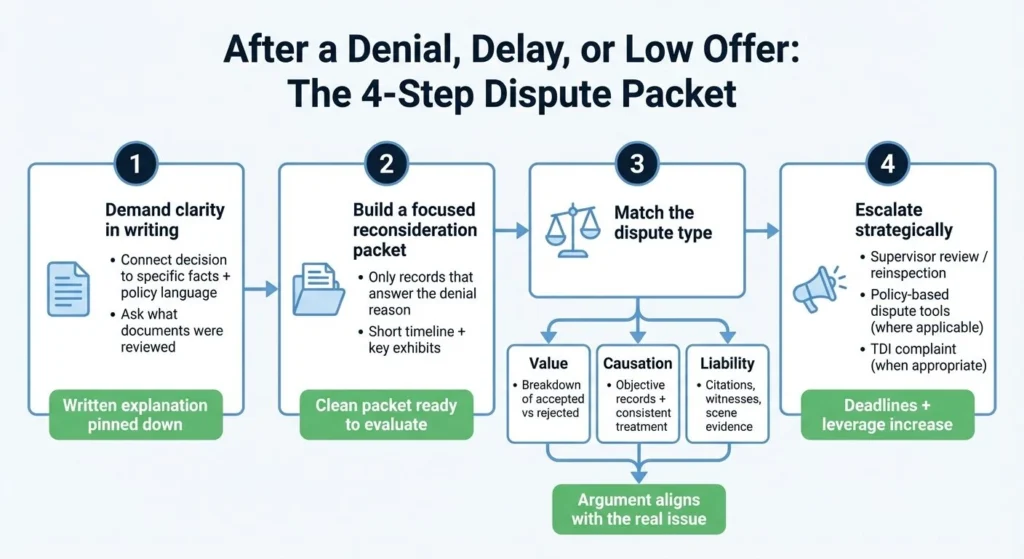

How to Challenge the Decision Without Losing Leverage

A structured dispute package is usually more effective than repeated calls.

Step 1: Demand a clear written explanation. Ask the insurer to connect the decision to specific facts and specific policy language.

Step 2: Send a focused reconsideration packet. Include only the key records that address the denial reason:

- ER and follow-up records

- Imaging reports and diagnoses

- Itemized bills and payment ledger

- Wage loss proof and work restrictions

- Photos, crash report, witness information, and a short timeline

Step 3: Address the right dispute type.

- If the fight is about value, request a written breakdown of what the insurer accepted and what it rejected.

- If the fight is about causation, send objective records and consistent treatment documentation.

- If the fight is about liability, send facts that support fault, including citations, witness statements, and scene evidence.

Step 4: Consider escalation tools. Depending on the claim, escalation may include supervisor review, reinspection requests, a policy-based dispute process (such as appraisal in certain property disputes), and a complaint to the Texas Department of Insurance.

If you are seeing patterns of delay or denial tactics, this may help: How to Protect Yourself Against Big, Bad Faith Insurance

Get Help from an Attorney

Insurance denials and low offers often change when you force the insurer to commit to clear reasons, clear deadlines, and a documented record. If you were hurt in a crash in Texas and your claim was denied, delayed, or undervalued, the next step is usually organization plus escalation, not silence.

If you want help reviewing the denial basis, building a clean evidence packet, and protecting your claim strategy, request a free consultation with Angel Reyes & Associates. Free initial consultations are available, and there is no fee unless we win.

Insurance Denial & Bad Faith FAQs

What is a “reservation of rights” letter, and should I worry?

It often means the insurer is investigating while reserving the ability to deny coverage later. Ask what specific policy provisions are at issue and what documents the insurer needs to finish the decision.

Should I sign a broad medical authorization for the insurer?

No. Often you can provide specific records instead of a blanket release. If you sign anything, limit the scope and dates when possible, and keep a copy of exactly what you signed.

Can I ask for a reinspection or a second review after a denial?

Yes, many insurers will reconsider with new records, a clearer timeline, or corrected facts. Request a supervisor review in writing and attach documents that address the stated denial reason.

What is “depreciation” and a “holdback” in property-related claims?

Some policies pay actual cash value first and hold back depreciation until repairs are completed. Ask the adjuster to confirm whether your policy uses replacement cost and what proof is required to recover the holdback.

Will a quick settlement release block future treatment bills?

It can. Releases often cover known and unknown injuries, so signing too early may shift future costs to you. Consider waiting until your doctor has a clearer prognosis and treatment plan.

About the Authors

Angel Reyes

Writer

Angel L. Reyes, III is the Founder and Managing Partner of Angel Reyes & Associates. A nationally recognized trial attorney and business leader, Angel has helped over 70,000 injury victims recover more than $1 billion since founding the firm in 1993. Named to the Texas Super Lawyers list annually since 2008, Angel brings Wall Street experience, Ivy League education, and a deep commitment to client advocacy. He is a frequent legal commentator and published author with extensive contributions to legal scholarship, trial strategy, and consumer protection.

Kyle Nicolas

Editor

Kyle Nicolas is the Web Content & SEO Manager at Angel Reyes & Associates. He has more than 10 years of experience as a marketing co...

Spencer Browne

Reviewer

Spencer Browne is a partner at Angel Reyes & Associates and a Board Certified personal injury trial lawyer with nearly 100 jury trials a...